The Wooden Nickel is a collection of roughly a handful of recent topics that have caught our attention. Here you’ll find current, open-ended thoughts. We wish to use this piece as a way to think out loud in public rather than make formal proclamations or projections.

1. The Consumer Brake

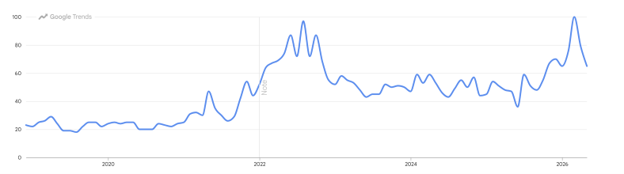

Inflation has been a persistent talking point among consumers and markets alike, despite their climb down from COVID highs. Even in their (temporary) nadir, Google Trend searches for inflation surpassed pre-COVID levels, speaking to the constant presence in people’s minds.

Figure 1: Google Searches for “Inflation”

The recent elevated interest was sparked by none other than the war in the Persian Gulf. The ubiquity of crude oil and its derivatives in daily life justifies this elevated concern. And it’s not just top of mind for consumers as bankers at the Federal Reserve have voiced an outlook for higher prices as a result of the conflict. It’s been quite the wrench in policy maker’s expectations given that coming into 2026 the open hope was for multiple rate cuts by end of the year. Instead, today, current market pricing expects a hike in interest rates by end of the year.

Figure 2: Monetary Policy Expectations At Year Start (Left) and Last Week (Right)

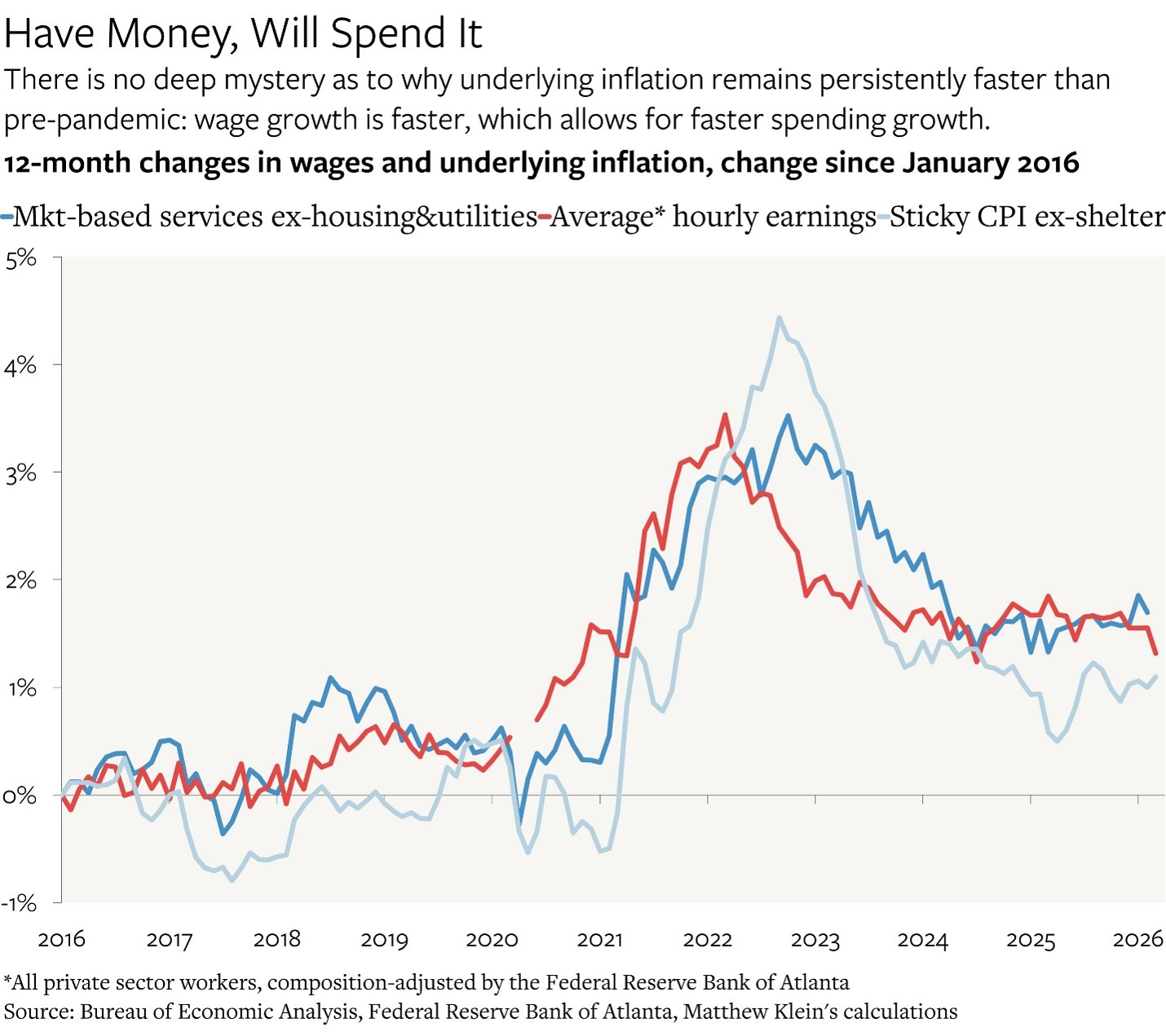

But while the supply side dynamic has consumed so much of the oxygen I don’t think enough attention has been paid to other catalysts. Whereas higher prices driven by supply forces can act as a natural governor it’s the more chronic “demand-push” type of inflation that should be front of mind for policy makers. Here, Matthew Klein, formerly of the Financial Times and Barron’s, has been the best voice and illustrator chronicling the concern. In short, if we aim to return to a 2% world (ie the environment before COVID) then we should see some evidence of that in the subcomponents making up our various price indices. So far, not so good.

Figures 3 & 4: Neither Wages nor Service Pricing Align with a 2% World, Source: Matthew Klein

Currently, what represented levels of “peak” wage growth and services pricing in the pre-COVID world has served as a floor even with the dramatic disinflation post 2022. The Fed cannot do anything to open the Strait of Hormuz much like it couldn’t untangle the knots in supply chains during the COVID stimulus. The same cannot be said for any demand-push type forces and the latter constitutes the majority of economic activity in the US (over 70%). Elevated services demand (and a shrinking pool of labor) will keep those wages robust.

And as long as those wage gains are there they will be spent. From recent quarterly commentary:

Visa CEO: “There’s certainly a lot of things happening around the world that people are looking at in the future and wondering what’s going to happen. But if you actually look at the facts and you look at the data, especially as it relates to our network, there’s an enormous amount of resiliency in consumer spending, and that continues today.”

Home Depot’s CEO: “…our consumer has been remarkably resilient….quite remarkable, as I said, how the consumer has been pretty darn resilient to all of that.”

Decker’s Outdoor CFO: “I think as we look at the environment, consumers, even with everything going on, are still operating from a healthy position.”

Dollar Tree CFO: “when we look at Dollar Tree, when I take apart the data from this past quarter and we look at our store base by income demographic, all of our cohorts are comping positive in this past quarter”

Spending has been so strong that the personal savings rate hit 2.6% in April, continuing its decline the past year. The only times the rate was lower was 1) after the dramatic influx of savings transferred via the Government sector thanks to fiscal stimulus during COVID and 2) as credit lines got filled up leading up to the GFC.

Figure 5: The Personal Savings Rate

One way or another this will have to get resolved. Either through higher levels of wages, which feed back into the loop between wages and spending that have accelerated the economy already and pose a policy conundrum, or through dramatically lower expenditures. Keep in mind, that the rigidity of wages and spending (and thus prices) existed even before the Persian Gulf energy constraints. In other words, I’m not sure reduced energy prices will be enough.

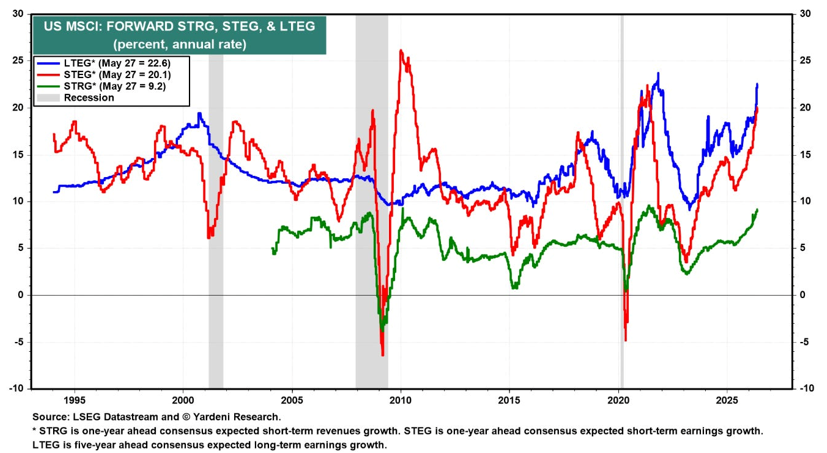

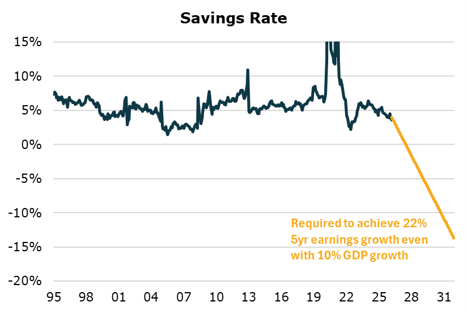

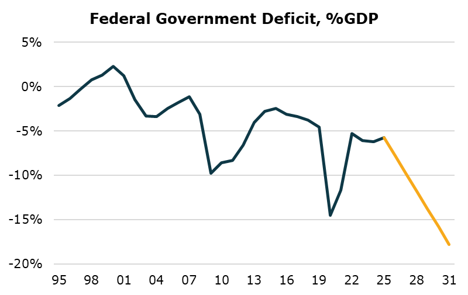

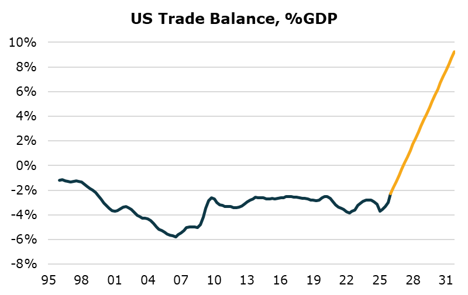

These (meager) level of savings do not last historically. And my concern is that (from a long-term perspective) the market has only priced in an extrapolation of a tight/robust spending environment long into the future. Five year earnings projections for the US stand at just over 22%, a rate completely unmoored from historic rates (past estimates of such high earnings rates did not materialize).

Figure 6: Extrapolating the Good Times Farther Out Into the Future, Source: Ed Yardeni

As computed by Bob Elliott, using the Kalecki-Levy framework of analysis near and dear to us, to bring these estimates into fruition for the corporate sector requires some other sector to supply the earnings power by drawing down on savings: households, the government, or the international sector or of course some combination. But through the lens of history, I think you can start to see why it feels improbable based on Elliott’s work:

Figures 7, 8, & 9: What Savings Are Left?, Source, Bob Elliott

2. Knowing What You Own

There’s a fable that Howard Marks recites in The Most Important Thing that I’ve long enjoyed.

“Day traders considered themselves successful if they bought a stock at $10 and sold at $11, bought it back the next week at $24 and sold at $25, and bought it a week later at $39 and sold at $40.

If you can’t see the flaw in this – that the trader made $3 in a stock that appreciated by $30 – you probably shouldn’t read the rest of this book.”

Upon joining a new investment firm several years ago, a friend of mine was taken out to lunch by the firm’s Chief Investment Officer. Asking for advice on starting out a career in investments the CIO urged my friend to develop “templates” for different situations in investing: value stocks, turn arounds, capital return stories, etc.” It was an interesting piece of advice. I’m not sure, to this day how much I agree, but it did crystallize to myself an important distinction that I think most people, even professional investors (which is maddening at times I will admit), fail to internalize and that’s understanding the difference between a trade and an investment.

There’s a place for both trades and investments, especially over the long run. We’re only given one opportunity set each day and we don’t get to pick the price, only whether we want in or not (the classic voting machine versus weighing machine analogy of Buffett comes to mind.) And as a result sometimes the best place to put capital to work isn’t buying a company whose fundamental business prospects will compound because price is prohibitive but rather what Peter Lynch called “stalwarts”, those businesses who may not have growth runway ahead of them but offered clear value to their customers and had been left behind; John Huber, a favorite investor, refers to the approach as “buying cheap and selling dear.” Here your returns on a security come not from the incremental capital deployed but rather simply from multiple expansion.

I’ve found that setting that first distinction on whether something fits into the “trade” or “investment” label sets off a chain reaction of follow up questions and considerations that are very different from each other. Time horizon, management evaluations, financial statement analysis, all vary to enormous degrees depending upon which of the two categories you’re really after.

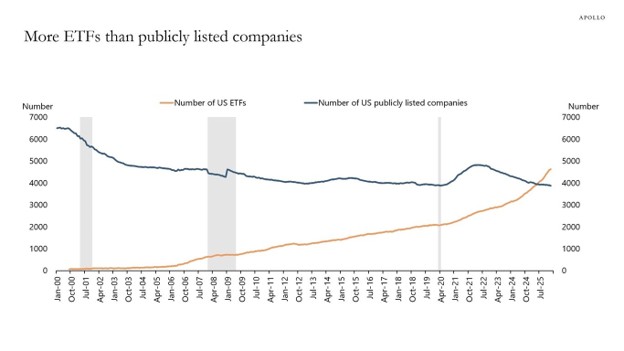

This all came to mind after seeing the below chart from Apollo this past week. It’s made the rounds in parts of the financial press as a sign of doom (it shouldn’t) but it does make me wonder if people realize that while you can chase on the bandwagon of someone else’s idea you cannot outsource conviction, emotional durability, and risk management.

Figure 10: More ETFs than Individual Companies, Source: Apollo Said another way, I think many investors would benefit from really thinking about how they expect to earn a return on a security before it is they buy it or thinking a bit more critically about what has driven pricing to date or flows to/away from certain stocks. Between passive forces, the quantization of everything, thematic shortcuts, leveraged ETFs, and a host of other factors knowing what you own, why you own it, and what makes it move is more crucial than ever. Are you buying earnings and cash flow? Or are you hoping that the next headline in the WSJ bodes well for your stock that’s six degrees of separation away?

Said another way, I think many investors would benefit from really thinking about how they expect to earn a return on a security before it is they buy it or thinking a bit more critically about what has driven pricing to date or flows to/away from certain stocks. Between passive forces, the quantization of everything, thematic shortcuts, leveraged ETFs, and a host of other factors knowing what you own, why you own it, and what makes it move is more crucial than ever. Are you buying earnings and cash flow? Or are you hoping that the next headline in the WSJ bodes well for your stock that’s six degrees of separation away?

3. Recommended Reads and Listens