Market Action

Most global equity benchmarks closed modestly firmer on the week, while Asian equity benchmarks experienced a significant increase of several percentage points on the week. The yield on the US 10-year Treasury note was unchanged versus a week ago at 2.66% while the price of a barrel of WTI crude oil rose roughly $2.50 to $57.75. Volatility, as measured by the CBOE Volatility Index (VIX), declined to 14 from 15.6 last Friday.

As another round of talks between officials from the US and China unfolded throughout the week, news emerged that the negotiators have made progress on a number of the most contentious structural issues, suggesting an agreement may be within reach. Memorandums of understanding are being drafted covering issues such as forced technology transfer and cyber theft, intellectual property rights, services, currency, agriculture and non-tariff barriers to trade. Additionally, the two sides are discussing enforcement mechanisms to ensure compliance with any deal, a major concern for the US. President Donald Trump said that the March 1 deadline to reach an agreement is “not a magical date,” suggesting any hike in US tariffs on Chinese goods is unlikely so long as the two sides continue to make progress toward an agreement.

The EU threatened to react in a “swift and adequate manner” if the US imposes additional tariffs on European car imports. The US Commerce Department recently submitted a document to President Trump that reportedly recommends levying duties on European cars on the grounds that damage to America’s car industry is a threat to national security. The president has 90 days to decide whether to act.

With just over a month before the UK is scheduled to leave the EU, British prime minister Theresa May traveled to Brussels for another round of negotiations with European Commission president Jean-Claude Juncker. The EU has long vowed not to reopen talks on the withdrawal treaty, but reports circulated late in the week that the EU is open to adding a legally binding codicil to the agreement allowing the UK to exit the Irish backstop – which guarantees that the Irish border will stay open – with 12-months’ written notice. Given May’s recent difficulties in parliament, it is thought that the EU wants to see if that option can pass the House of Commons before proceeding any further. Talk circulated late in the week that May could seek a three-month extension of the negotiating period.

Flash purchasing managers’ indices for February released on Thursday show that the global manufacturing sector continues to struggle. Manufacturing PMIs in Europe and Japan both fell below 50, signifying a contraction, with US data showing that while activity continues to expand, it is doing so at a slower pace. The global service sector appears to be in much better shape, though manufacturing has historically tended to be a better leading indicator of where the economy is headed next.

The minutes of the January meeting of the US Federal Reserve’s Federal Open Market Committee meeting confirmed that almost all the participants thought it desirable to announce before too long a plan to stop reducing the Fed’s asset holdings later this year. They stressed that they favored a patient approach to monetary policy that allows them to observe the effects of past rate hikes, saying soft inflation data allow the committee to be patient.

Click here for this week’s updated market returns table.

What could affect markets in the days ahead?

The question for the ECB before its March 7 meeting is: will “flash” inflation numbers due Thursday and Friday reinforce the picture of a sluggish economy and below-target inflation? An advance peek into February’s eurozone PMI surveys indicates factories across the bloc shunted into reverse for the first time in six years.

UK Prime Minister Theresa May has promised to make a statement to parliament on February 26 regarding her progress on a Brexit divorce deal, and then to allow lawmakers to debate the issue on February 27. Any sort of defeat for May – who many argue really has nothing very new to present to parliament – will raise risks of a no-deal Brexit, dealing a blow to the pound and hurting vulnerable sectors, such as housing.

The March 1 deadline that ends the 90-day US-China trade truce arrives soon and hopes are high that some kind of trade deal is reached by then. If not, markets hope the deadline will be postponed. The alternative? A significant trade war escalation, with Washington slapping 25% tariffs on $200 billion worth of Chinese goods – more than double current levels.

After a week’s delay, Nigerians are headed to the polls on Saturday to pick a new president after a shock last-minute one-week delay to the vote. Africa’s top oil producer has suffered from violence surrounding its elections in the past, leaving the population in turmoil and rattling its financial markets. Elsewhere in the region, voters in Senegal on Sunday will have their say at the ballot box with President Macky Sall the strong favorite to win.

This Week from BlackSummit

Projected Q1 Earnings Contraction: Valuations, Momentum, and Resistance Levels

John E. Charalambakis

Listen on the go! Subscribe to the podcast Market Commentary with BlackSummit on iTunes, Android, Google Play, Stitcher, Spotify or TuneIn.

Recommended Reads

The Failure of the French Elite – WSJ

The Nord Stream 2 gas pipeline is a Russian trap – Putin’s pipeline

Africa’s debt crises not the fault of creditors alone | DW

Munich Security Report 2019 – Munich Security Conference

China’s Property Market, Once a Lifeline, Now Carries Economic Risks – WSJ

Video of the Week

DW Freedom of Speech Award 2019 for Anabel Hernández

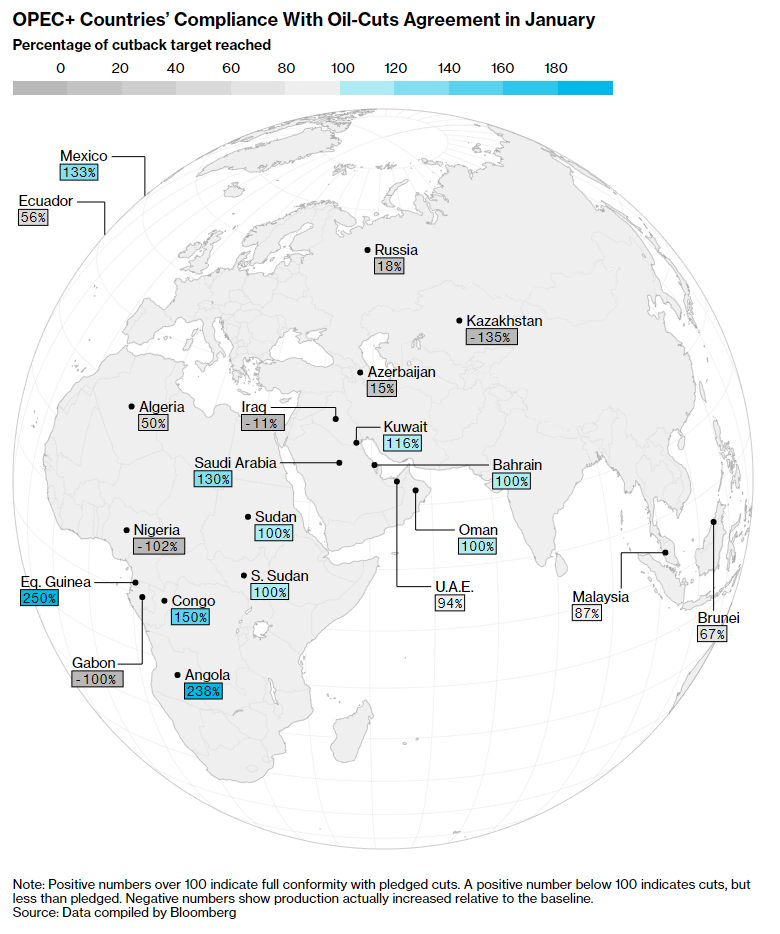

Image of the Week