Mickey came home in the early hours of Saturday. He told his folks that he had crashed the car they had just bought him. That same morning, his father wanted to demonstrate understanding, so they went and bought a brand-new car for Mickey. Three weeks later, Mickey crashed the car again. His daddy doubled down and bought him another brand-new car. Money, after all, was abundant. Two months later, the story repeated itself. It was obvious that Mickey’s parents suffered from a collective hallucination.

We are balancing on the ledge of multiple forces that could tip the economy and put the markets on an unpredictable trajectory. The pace of political change and actions in the US has caught the public unprepared. Similarly, the pace of the tech momentum could be reversed, as last Friday’s losses indicated, with some tech leaders losing more than 12% in a day. This is the nature of walking on the ledge of formations that can reverse at a moment’s notice. Let’s review some of those formations:

- Price/inflationary pressures

- Unsustainable debts

- Rising yields because of the above two points (and not only) make the debt even more unsustainable

- Questionable valuations sugarcoated as normal, simply because we have been raising forward earnings, and thus lowering the P/E ratio

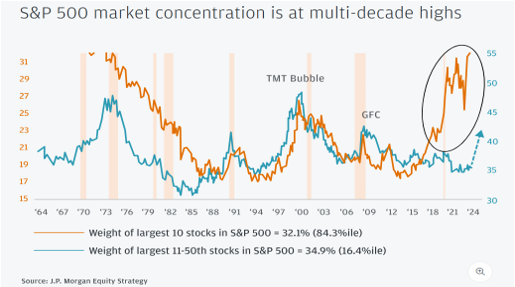

- Overconcentrated market, as shown below

- Cracks in the credit markets, as demonstrated by restricted withdrawals from well-known funds

- Geopolitical conflict that could start with a simple blockade of Taiwan

- A leaderless world where guardrails, rules, and alliances are disputed amid rising authoritarianism

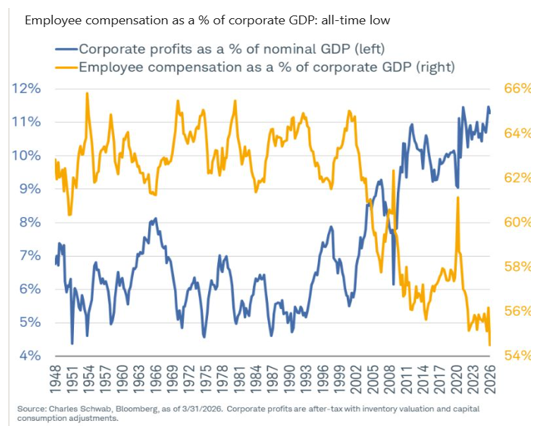

- Rising inequalities (not just economic), and stories of immense corruption that is brewing resentment (see graph below)

The markets’ discipline (temporary declines, rising long-term yields), or some moral suasion from officials, does not amount to a step back from the ledge. The key problem is the loose monetary policy which encompasses low rates in the face of inflationary pressures (it’s a quite a joke to have the federal funds rate hovering around 3.62% when wholesale inflation exceeds 6%), recycling maturing Treasuries (rather than reducing the Fed’s balance sheet), expanding open market operations, reinvesting maturing mortgage-backed securities into Treasuries, manipulating reserve requirements that lowers bank standards, and similar actions all of which amplify capital velocity and stimulate momentum and a market melt up. As we recently wrote: “The velocity of capital empowers the entire financial system to use its projects (e.g., data centers) and its ‘paper wealth’ (e.g., portfolios) to create more purchasing power.” The paper wealth just in the US represents a multiple of 6+ over the GDP, per recent Bank of America analysis.

Solid growth (economic, financial, social, etc.) requires capital infusions. There is evidence that points to a revival in activity in many parts of the world. All that activity requires capital, so we could argue that we are at the beginning of a new investment super-cycle, especially if we adopt the solid hypothesis that AI is a transformative technology that will bring in a revival in energy consumption (mostly from renewable sources), manufacturing, upgraded technologies, and human capital, which will transform the world like the agricultural and industrial revolutions.

However, such transformation demands the re-emergence of real assets relative to financial assets that have exploded in the last 40 years, as the following figure demonstrates.

Financial assets may need a pugnacious shellacking to bring balance into the economy. Any half-baked measures of a quarter of a percent rate increase won’t cut it. Such measures – especially if accompanied by accommodative language – will build atrophy into the economy. The markets need leadership that will bring discipline, lower yields, send a message of credibility, take excesses out, fertilize the ground for debt refinancing at lower rates, and nurture the trust in the pillars of programs and institutions that are the cornerstones of the global economy.

Mr. Warsh, it’s time to revisit the Paul Volcker days. Please raise the short-term interest rates decisively.