Welcome to our monthly newsletter which covers key developments in major non-US markets. With this newsletter, we highlight corporate, debt, and monetary policy news in European, Asian, and Latin American markets. We end this piece with a spotlight on commodities.

European Markets

Corporate and Business News

- Foreign bidders kept circling UK assets, pushing announced UK-target M&A to near-record levels and reinforcing the valuation-gap narrative for London-listed equities.

- AkzoNobel became a flashpoint for European industrial consolidation after rejecting a €12.5 billion approach from Nippon Paint and Sherwin-Williams, crystallising takeover optionality in the chemicals and coatings space.

- EasyJet re-entered the M&A spotlight as Castlelake pursued a takeover approach, reviving speculation around airline consolidation and lifting travel-sector sentiment.

- STMicroelectronics reignited the European AI trade after lifting its data-centre revenue targets, driving a sharp rally across semiconductor and technology names.

- Novo Nordisk advanced the European obesity-drug race as regulators backed and then the UK approved its oral Wegovy pill, giving healthcare investors a fresh growth catalyst.

- Partners Group’s decision to cap withdrawals from an $8.6 billion fund rattled confidence in evergreen private-market vehicles and spilled over into listed asset managers.

Debt and Monetary Policy News

- Euro-area inflation re-accelerated to 3.2%, driven by energy and services, hardening the case for tighter ECB policy and pushing European front-end rates higher.

- The ECB delivered a 25bps “insurance” hike to a 2.25% deposit rate, lifted its inflation projections and trimmed growth, reinforcing a higher-for-longer tone across euro sovereign curves.

- ECB officials leaned “measured but vigilant,” arguing the inflation shock had not yet de-anchored expectations but still justified keeping further tightening on the table.

- The BoE held Bank Rate at 3.75% in a hawkish 7–2 split, lifting short-dated gilt yields as markets focused on persistent inflation risk rather than near-term easing.

- Political and fiscal credibility stayed central to UK fixed income, with leadership uncertainty and scrutiny of the next finance minister keeping gilts sensitive even as the immediate market reaction remained contained.

Asian Markets

Corporate and Business News

- SK Hynix dethroned Samsung Electronics as South Korea’s most valuable listed company, underscoring how the AI-memory boom has become the single most powerful force in Asian equity leadership.

- Japan’s governance story stayed front and center as pressure around Toyota Industries’ buyout economics reinforced the market’s view that activist capital is reshaping valuation discipline across Japan Inc.

- Reliance Jio moved toward what could become India’s largest IPO, giving Reliance Industries a fresh re-rating catalyst and refocusing investors on telecom, AI, and digital-platform monetization.

- China’s primary market saw a notable reopening signal as China Resources New Energy prepared Shenzhen’s largest-ever IPO, reinforcing investor appetite for state-backed renewable infrastructure stories.

- U.S.-China tensions hit sentiment across Hong Kong and mainland tech after Alibaba, Baidu, BYD, NIO, and other major groups were added to Washington’s military-linked list.

- India’s corporate-manufacturing ambition gained a strategic boost as Tata Electronics partnered with ASML on the country’s first front-end semiconductor fab, strengthening the long-duration chip-capex theme in South Asia.

Debt and Monetary Policy News

- BOJ delivered a landmark tightening step, lifting rates to a 31-year high and signalling further hikes, while pausing the pace of bond-buying tapering beyond the current plan to steady the JGB market.

- Japan’s super-long bond volatility remained a regional anchor risk, with investors focused on whether policymakers would lean against renewed upward pressure at the long end of the curve.

- China kept benchmark lending rates unchanged and tightened its grip over short-term money-market rates, reinforcing a cautious, liquidity-management approach rather than outright monetary easing.

- India’s RBI held rates steady but raised inflation forecasts, cut growth projections, and rolled out measures to support the rupee, leaving bond investors to price a more defensive policy mix.

- Indonesia’s surprise off-cycle rate hike to defend the rupiah stood out as the sharpest EM Asia policy response, lifting local yields but helping restore foreign appetite for central-bank bills.

Latin American Markets

Corporate and Business News

- Brazil’s petrochemicals landscape was redrawn as IG4 and Petrobras became co-controllers of Braskem, putting governance, restructuring, and capital-allocation expectations back at the center of the sector.

- Cross-border energy consolidation moved up the agenda after Ecopetrol launched a tender offer to take control of Brazil’s Brava Energia, broadening its regional growth ambitions beyond Colombia.

- Vale faced a fresh governance flashpoint when top shareholder Previ pushed for a vote on replacing the chairman, reviving investor focus on board independence and strategic direction at the mining giant.

- America Movil reinforced its defensive-growth profile by outlining steady revenue and EBITDA expansion through 2028 while holding annual capex near $7 billion, supporting the broader Latin American telecom investment case.

- Brazil’s distressed-debt and restructuring theme intensified as IG4 moved on Raizen’s debt stack, signalling that one of the region’s largest corporate workouts could evolve into a control transaction.

- Latin American airlines swung with the energy tape: higher fuel costs forced capacity trims at LATAM Brasil, before easing oil prices triggered a relief rally across the region’s carriers.

Debt and Monetary Policy News

- The Middle East oil shock forced a broad repricing across Latin American rates, pushing local bond yields higher as investors dialed back expectations for faster regional easing.

- Brazil’s inflation outlook deteriorated materially, with the government lifting its 2026 forecast to the top of the target band and May inflation accelerating further above consensus.

- Brazil’s central bank still cut the Selic by 25bp to 14.25%, but the decision was read as dovish, steepening the curve as markets questioned how much easing remained credible.

- Mexico’s disinflation trend improved, but Banxico kept a cautious tone as sticky core pressures, weaker growth, and Moody’s downgrade to Baa3 kept sovereign risk in focus.

- Chile’s central bank cut its 2026 growth forecast and nudged inflation projections higher, reinforcing a more difficult duration backdrop for Chilean fixed income.

- Argentina gained some debt-market relief as the World Bank approved a guarantee-backed package to lower financing costs and support public debt management, extending the compression in sovereign stress indicators.

Commodities Spotlight

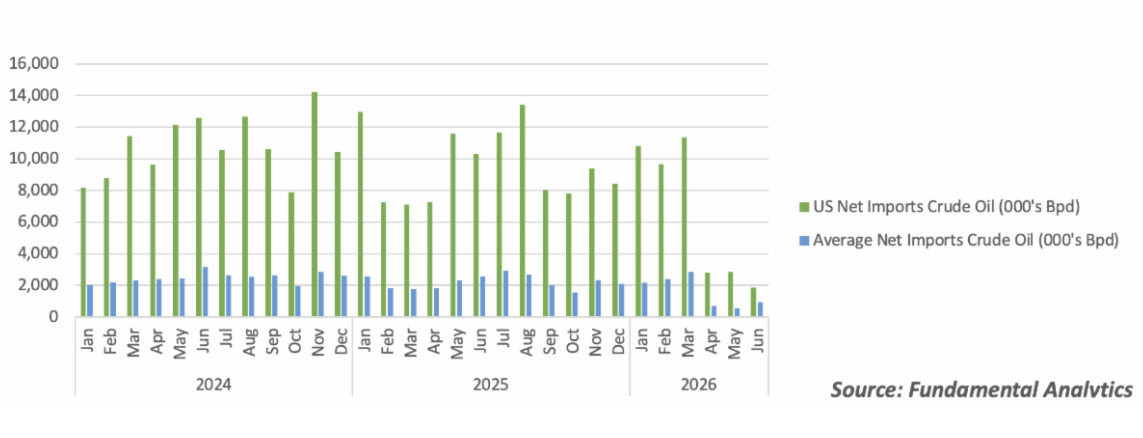

US-Iran Conflict Has Significantly Plummeted Net Imports. Supply Effects Are Visible in the Near Term

Source: Fundamental Analytics

NYMEX WTI front-month stayed highly volatile, initially trading near war-elevated highs as the Iran conflict threatened Hormuz flows, global inventories thinned, and U.S. crude exports surged to a record 5.6 mbpd as Asian and European refiners sought replacement barrels. U.S. crude stocks then drew sharply on strong refining runs and export demand, while gasoline and distillate inventories remained tight. Prices later retreated as ceasefire progress, Hormuz’s reopening, and a temporary U.S. licence for Iranian oil sales eased immediate supply fears and rebuilt expectations of looser balances.

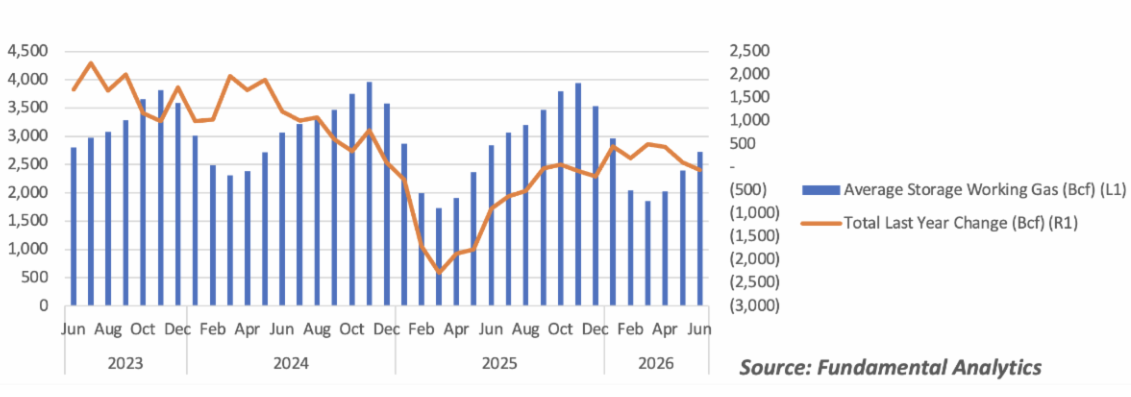

Hotter Than Expected Temperatures Lower Storage, Prices Follow

Source: Fundamental Analytics

NYMEX Natural Gas front-month moved higher overall, recovering from early weakness caused by lower LNG feedgas flows during export-plant maintenance. Strong Lower-48 production and comfortable storage, with working gas still above the five-year average, capped the rally. However, hotter weather lifted power demand, while rising LNG export capacity and geopolitical risks around Hormuz LNG flows and Qatar’s Ras Laffan complex added a risk premium. The result was a firmer but still supply-constrained market.