Welcome to our monthly newsletter which covers key developments in major non-US markets. With this newsletter, we highlight corporate, debt, and monetary policy news in European, Asian, and Latin American markets. We end this piece with a spotlight on commodities.

European Markets

Corporate and Business News

- BP delivered its strongest quarterly profit since 2023, with trading gains amplified by heightened geopolitical volatility. The result reinforced the view that Europe’s major energy groups remain key beneficiaries of disrupted commodity markets.

- Luxury sentiment weakened further as LVMH, Hermès, and Burberry came under pressure from softer demand and weaker travel flows. Conflict-related disruption added another headwind, weighing on one of Europe’s most influential equity sectors.

- European blue-chip earnings momentum improved materially, led primarily by energy and financials. That stronger profit backdrop helped support regional equities even as top-line revenue growth remained relatively subdued.

- Siemens reported strong second-quarter results, with orders rising double digits and profit reaching €3.0 billion, reinforcing confidence in industrial demand and the company’s positioning in AI-driven automation and infrastructure markets.

- UniCredit’s pursuit of Commerzbank turned openly hostile, reviving the cross-border banking consolidation theme in Europe. The situation also sharpened the political debate around financial integration and the limits of the EU single market in banking.

- Orange upgraded its 2026 outlook after a first-quarter earnings beat, supporting sentiment around the French telecom sector. At the same time, regulatory contacts around the proposed joint SFR bid reinforced expectations for further market consolidation.

- Vodafone guided to higher core earnings after recent market exits, helping investors focus on a cleaner and more disciplined portfolio story. The update also strengthened confidence in UK consolidation benefits and the longer-term recovery path in Germany.

Debt and Monetary Policy News

- The European Central Bank (ECB) kept rates unchanged but left the door open to further tightening, as policymakers acknowledge that the energy-driven inflation rebound is forcing markets to reprice the front end of the euro curve.

- Euro-area inflation accelerated back to 3.0%, led largely by higher energy costs, reviving the hawkish policy debate and pushing core sovereign yields higher across the region.

- The Bank of England (BoE) held the Bank Rate at 3.75% but warned that the inflation consequences of the Iran-related energy shock may still require a forceful policy response, keeping gilt volatility elevated.

- Long-end sovereign markets come under renewed pressure as Germany’s heavier borrowing plans and rising UK fiscal and political concerns lift term premia, sending Bund and gilt yields sharply higher.

Asian Markets

Corporate and Business News

- China has agreed to buy 200 Boeing jets, with a potential for the order to rise to as much as 750 planes, U.S. President Donald Trump told reporters, adding that the planes would have GE Aerospace engines.

- Stellantis and longtime Chinese partner Dongfeng have signed a $1.2 billion deal to produce Peugeot- and Jeep-branded vehicles in China, hinting at future expanded cooperation. The deal equates to a combined investment of more than 8 billion yuan, or about 1 billion euros ($1.2 billion), with Stellantis expected to contribute about 130 million euros.

- The U.S. has cleared around 10 Chinese firms to buy Nvidia’s second-most powerful AI chip, the H200, but not a single delivery has been made so far, leaving a major technology deal in limbo as CEO Jensen Huang seeks a breakthrough in China this week. Huang, who was not initially listed in a White House delegation to Beijing, joined the trip after an invitation from President Trump.

- China’s top contract chipmaker, Semiconductor Manufacturing International Corp, said orders from overseas clients are increasing as the global artificial intelligence boom tightens capacity at foreign foundries. “There are still quite a lot of semiconductor capacity expansion projects and companies in China,” co-CEO Zhao Haijun said during an earnings call. “These are among the few places with available production capacity, so we are seeing many overseas customers shift their orders to be manufactured in China.”

- China’s Alibaba said it would exceed its planned AI investment of up to 380 billion yuan ($55.96 billion) over the next three years, as early signs of returns from the technology push it to ramp up its cloud-computing capacity. The company missed market expectations for fourth-quarter profit, but its U.S.-listed shares jumped 7% after executives said Alibaba has a clear outlook for returns on AI spending over the next three to five years.

- Technology investor SoftBank Group reported that its net profit more than tripled to 1.83 trillion yen ($11.60 billion) in the January-March quarter, as it booked gains on the value of its investment in ChatGPT-maker OpenAI. It was SoftBank’s fifth consecutive quarterly profit, with the Vision Fund investing arm booking an OpenAI-driven gain of 3.1 trillion yen in the quarter.

- Japan’s Eneos Holdings has agreed to acquire Chevron’s Southeast Asia fuel business for about $2.17 billion, as it seeks to expand its regional footprint and tap growth in Asian and Australian energy markets.

- Samsung Electronics faces potential production disruptions as labor tensions escalate, with unions threatening strike action after wage negotiations stalled, raising concerns that any prolonged industrial action could hit chip output and disrupt global semiconductor supply chains.

Debt and Monetary Policy News

- Japan may have spent as much as 5.01 trillion yen ($32.06 billion) in its latest efforts to bolster its embattled currency, central bank data indicated, signalling repeated bouts of intervention in markets. The Bank of Japan’s projection for money market conditions for the following day indicated a 4.51 trillion yen net outflow of funds, compared with brokerage forecasts of between zero and an increase of 500 billion yen.

- The United States and Japan believe that excess volatility in the currency market is undesirable, U.S. Treasury Secretary Scott Bessent said. His comments are seen as offering some support to Tokyo’s recent round of intervention to prop up the yen. Speaking after his meeting with Prime Minister Sanae Takaichi, Bessent also said he was confident Bank of Japan Governor Kazuo Ueda would successfully guide monetary policy to avoid being behind the curve in addressing too-high inflation.

- The Bank of Japan is expected to raise its key rate to 1.0% in June as it continues normalising policy amid rising inflation linked to the Iran war. Although rates were held at 0.75% last month, dissent among board members highlights growing concern over energy-driven inflation pressures, with the OECD backing further hikes toward 2% by 2027 as domestic demand and wage growth strengthen.

- China’s central bank is maintaining a “moderately loose” monetary policy stance while increasing liquidity support, even as weak credit demand highlights fragility in the domestic economy. New yuan loans unexpectedly contracted in April and credit growth missed forecasts, underscoring subdued borrowing activity. The People’s Bank of China has pledged to keep liquidity ample through targeted tools while warning of “imported inflation” risks from higher energy prices, with policymakers expected to rely on measures like reserve requirement ratio cuts rather than broad rate reductions to support growth and maintain yuan stability.

Latin American Markets

Corporate and Business News

- The future of Pemex CEO Victor Rodríguez is increasingly uncertain as the longtime ally of President Claudia Sheinbaum struggles to turn around Mexico’s embattled state oil company. The first 18 months of his tenure at Pemex have been marked by worsening internal divisions, a major oil spill, and a deadly refinery accident. Production is just 1.6 million barrels a day, short of a 1.8 million target, and the company has been unable to take advantage of the surge in oil prices resulting from the Iran war.

- Brazil’s retail sales volumes beat expectations and reached a record high in March, data from statistics agency IBGE, though high borrowing costs continue to restrain a broader recovery. Sales rose 0.5% in March from the previous month and it was the third consecutive monthly increase, with five of eight sectors posting gains.

- China’s CMOC Group has agreed a $1.7 billion deal to develop Ecuador’s largest gold mine, the Los Cangrejos project, after securing the asset through its acquisition of Lumina Gold. The project is expected to generate more than $4 billion in state revenue and marks a significant expansion of China’s presence in Latin America’s mining sector.

- Petrobras has signed a $2.2 billion contract to build and operate vessels, underscoring continued heavy investment in offshore oil infrastructure to boost production capacity, as the company seeks to expand output from key deepwater fields and strengthen its position as a leading global energy producer.

- Mexican retail and bottling group FEMSA , which runs OXXO convenience stores and gas stations, said its payments unit NetPay is launching a digital payments system for gas stations in the country, as the government pushes the sector to move away from cash.

- Mexico has suspended imports from the U.S. of breeding pigs, viscera, and pork offal products after U.S. authorities detected pseudorabies virus antibodies in some swine, the head of Mexican pork producers’ group Opormex told. The suspension affects about 10% of Mexico’s total pork-product imports from the U.S. but does not include pork meat because it does not pose a transmission risk.

- Brazil’s JBS, the world’s largest meatpacker, posted a 56% decline in its first-quarter net profit, missing market estimates as the firm grappled with challenges across its beef and poultry operations in North America. The company, whose products include beef, poultry, and pork, reported a net profit of $221 million in the January-March period, compared to a forecast of $236 million from analysts polled by LSEG.

Debt and Monetary Policy News

- Venezuela announced on Wednesday it would begin restructuring its external debt, which has been in default since 2017 and is estimated by analysts to exceed $150 billion in unpaid bonds, arbitration awards and interest. Restructuring Venezuela’s sovereign debt and that of state oil firm PDVSA will bring the country “out of the shadows” of the global financial system, interim Central Bank President Luis Perez said.

- Argentina’s monthly inflation rate was 2.6% in April, down from the 3.4% registered in March but slightly above analysts’ forecast of 2.5% despite increases in all sectors, data from national statistics agency INDEC showed. In the 12 months through April prices rose 32.4%, edging below the previous month’s rate of 32.6% and in line with analyst forecasts.

- Argentina’s country risk hit its lowest level since the beginning of February as confidence in the government’s ability to pay back its debt grows, triggering talk about whether it is time for the South American country to return to international capital markets. The country’s risk index tightened to 498 basis points on JPMorgan’s EMBI Global Diversified Index.

- Credit ratings agency S&P revised Mexico’s outlook to “negative” from “stable”, citing the risk of very slow fiscal consolidation largely due to weak economic growth that could lead to a faster-than-expected buildup in government debt and a higher interest burden.

- The Bank of Mexico cut its benchmark interest rate in a split decision and said it was ending an over two-year-long easing cycle as it balances concerns over above-target inflation with pressure to revive Mexico’s slowing economy. The 25 basis point cut brings the rate to 6.50%, its lowest since May 2022.

Commodities Spotlight

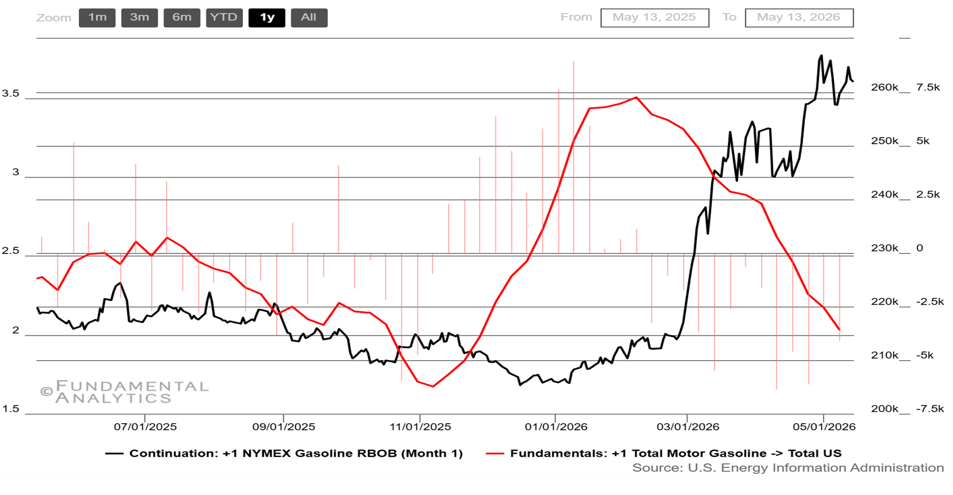

Gasoline Futures Hit 4-Year High As Inventories Slump

Source: Fundamental Analytics

RBOB gasoline front-month stayed strongly bid and volatile, as persistent U.S. gasoline stock draws, inventories slipping below seasonal norms, and refinery runs near 90% tightened the domestic balance ahead of peak driving demand. Record crude and product exports also drained supply, while the Iran war and Ukrainian strikes on Russian refineries disrupted global refining capacity and amplified product-market stress. Prices remained elevated despite occasional relief on ceasefire headlines, because the underlying gasoline supply cushion kept shrinking.

Wheat Prices Return to 10-Month High on Longer Than Expected Dryness and Middle East Conflict

Source: Fundamental Analytics

CBOT wheat front-month firmed overall, with weather risk overtaking the broader supply backdrop. Persistent dryness in the U.S. winter-wheat belt and later USDA cuts to U.S. production and ending-stocks expectations lifted prices toward multi-year highs. That upside was partly tempered by timely rain improving European crop prospects, ample Indian state reserves despite a smaller harvest, and continued competition from low-cost exporters. Middle East tensions also added indirect support by raising fertilizer and freight costs, reinforcing concern over next-season global grain supply.