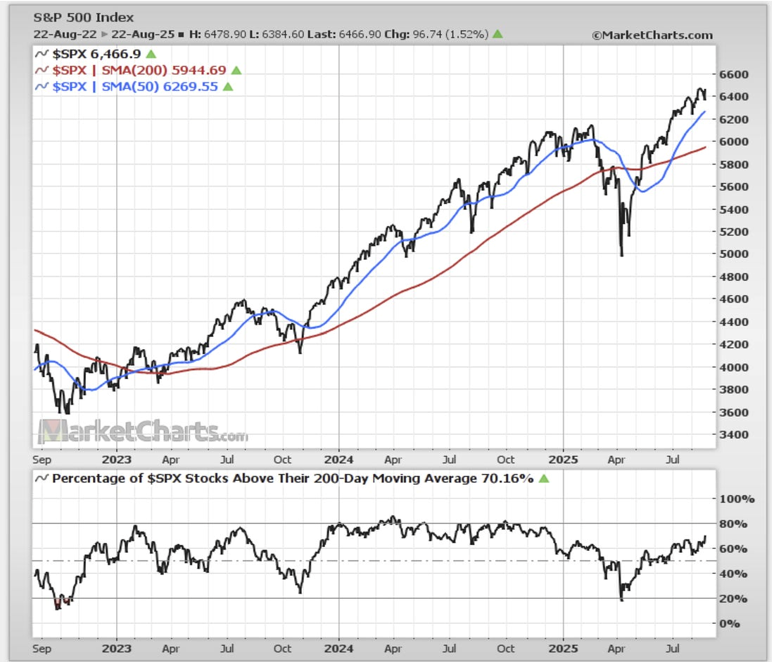

There is little doubt that momentum, liquidity, and earnings have been driving the equity market higher. Market breadth (advancing stocks relative to declining ones) has been coming back following significant drops, leading the indexes to higher highs and higher lows, as indicated by the graph below (this applies to the 200-day moving average, the 50-day moving average, and, of course, the current value of the S&P 500). As the bottom of the graph also shows, more than 70% of the stocks in the S&P 500 index stand above their 200-day moving average. Someone could say that the rising tide lifts all boats.

Stretched valuations and questions related to over-exposure in mega cap stocks (especially the top ten ones), along with concerns about AI profitability (especially after depreciation and on a free-cash flow basis), may continue pushing for an anacyclosis/reshuffling of holdings within a portfolio, increasing the portfolio’s exposure to more traditional sectors such as consumer staples, healthcare, international, and small caps. In the latest high volatility incidents/events observed last week, consumer staples and healthcare advanced during the times of turmoil (especially for tech stocks).

The Magnificent Seven are assumed to represent the aristocracy of stocks, which brings to our minds Polybius’ description of political systems (discussed in Book VI of Histories). In that book, we find what we call the anacyclosis/recycling/reshuffling of political systems. The cycle starts with a monarchical system that evolves into a corrup,t tyrannical system, which eventually is overthrown by an aristocratic system where few lead and which is perceived as a just and fair system.

However, that system sooner or later is replaced by a corrupt oligarchy where few dominate at the expense of the masses. It is unknown when democracy will eventually replace oligarchy. However, even democracy is not the end of the line, as democracy itself is replaced by ochlocracy, where the rule of the mob becomes the order of the day. The lack of order will eventually push the people to seek a new system (possibly a rule-by-one), so that the anacyclosis of the systems will keep repeating over time.

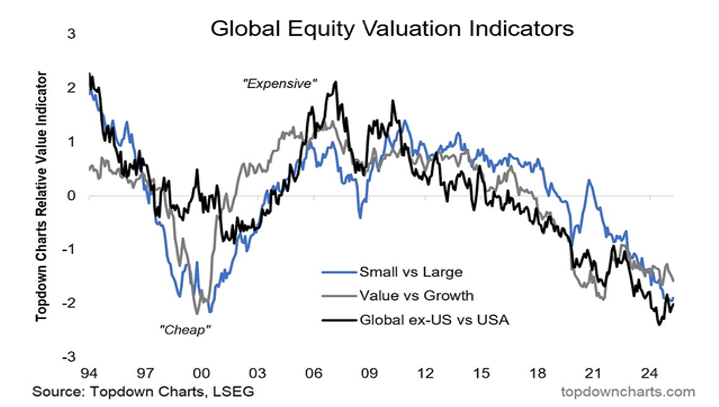

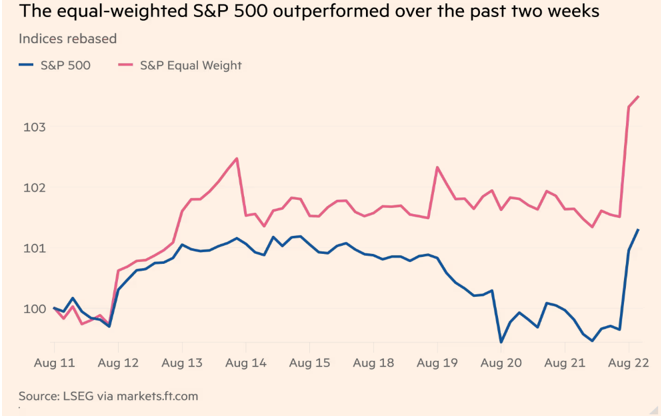

The argument that some anacyclosis may be useful to a portfolio might be supported by the following two graphs which portray that value, global (ex-US), and small caps may be attractive propositions relative to mega and large caps (first graph), while the second graph shows that in the last two weeks (which of course can hardly qualify for a trend) the equal-weight S&P 500 has outpaced the cap-weighted index (where the top 10 stocks make up 40% of the index).

If the law of diminishing returns related to AI spending starts landing in the valuation runway, investors’ appetite may turn sour, especially when we consider the conclusions of the MIT study regarding returns to AI spending: “Just 5 percent of integrated AI pilots are extracting millions in value, while the vast majority remain stuck with no measurable P&L impact.”

Any reshuffling should also incorporate another kind of anacyclosis that goes from euphoria (current market cycle) to a melt-up phase of complacency and exuberance, and from the latter, to correction and possibly to a bear market. Of course, in such a scenario of anacyclosis, one has to consider the trigger for such a transition. Current suspects discussed among analysts range from earnings failing to meet expectations, a revival of inflationary pressures, geopolitical shocks, and restrained consumer spending.

However, one scenario that seems to be missing from the current analysis is currency debasement, especially when we take into account the extraordinary amounts of governments’ debt around the world. In that scenario, a beggar-thy-neighbor race to the bottom (in terms of currency devaluations and depreciations) may unfold, which could have fatal consequences, including asset repricing. In the not-so-distant past (1960s), major countries went through such a phase, and when we consider a similar move by China just ten years ago, we may want to start thinking and hedging against that scenario, especially under the currently evolving political system.

The anacyclosis of political systems is a function of human nature, and regarding the latter, Polybius writes:

“For it is the people which alone has the right to confer honors and inflict punishment, the only bonds by which kingdoms and states and in a word human society in general are held together. For where the distinction between these is overlooked or is observed but ill applied, no affairs can be properly administered. How indeed is this possible when good and evil man are held in equal estimation?”