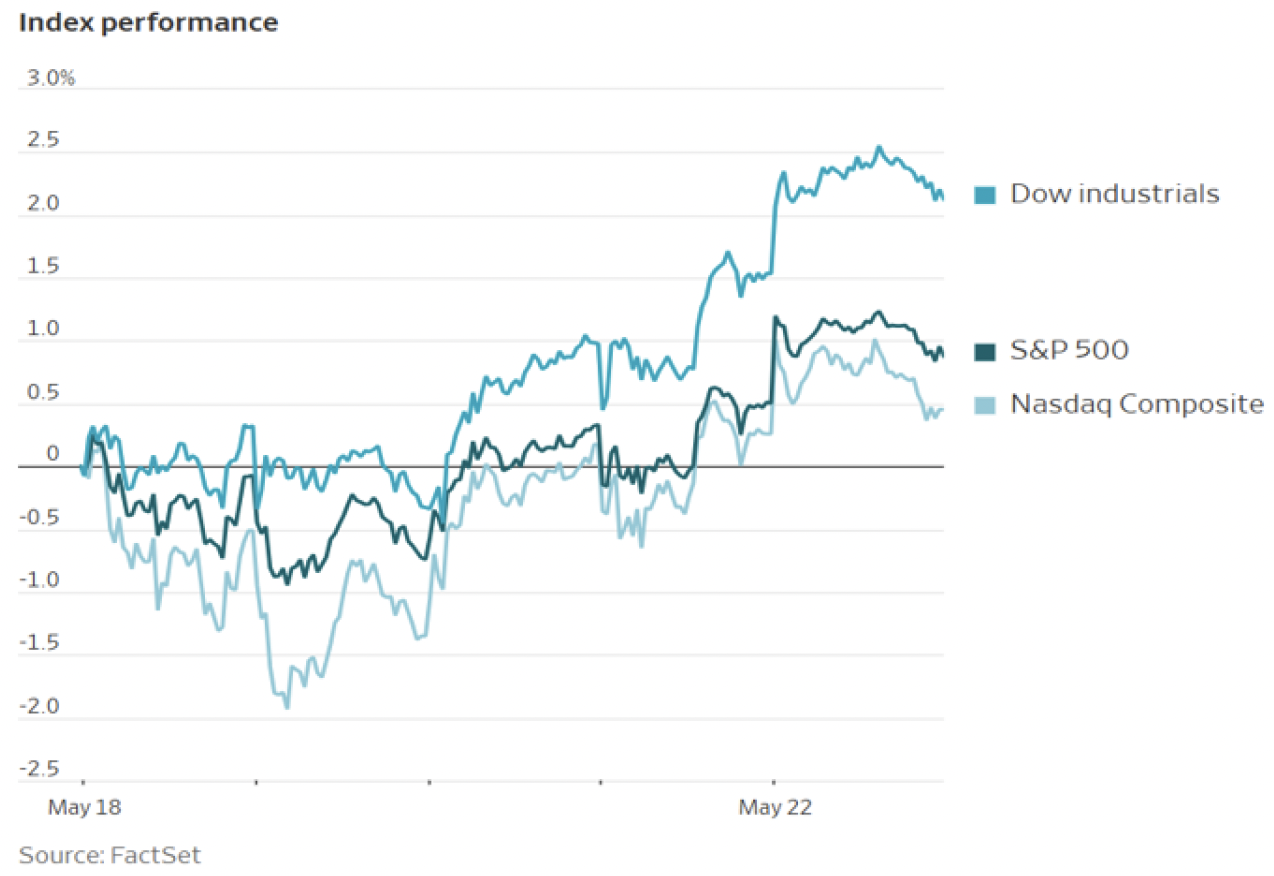

The Agricultural and Industrial Revolutions changed the economic, financial, political, social, and scientific landscapes when they took place in the 18th and 19th centuries. AI is destined to have the same impact. It has already made its significant mark in research and most definitely in the stock market. The latter’s upswing momentum is credited mostly to the spending and optimism that AI carries with it. That has made institutional investors have an almost 50% higher equity exposure than normal. It seems that nowadays investors’ appetite for equities is increasing exponentially.

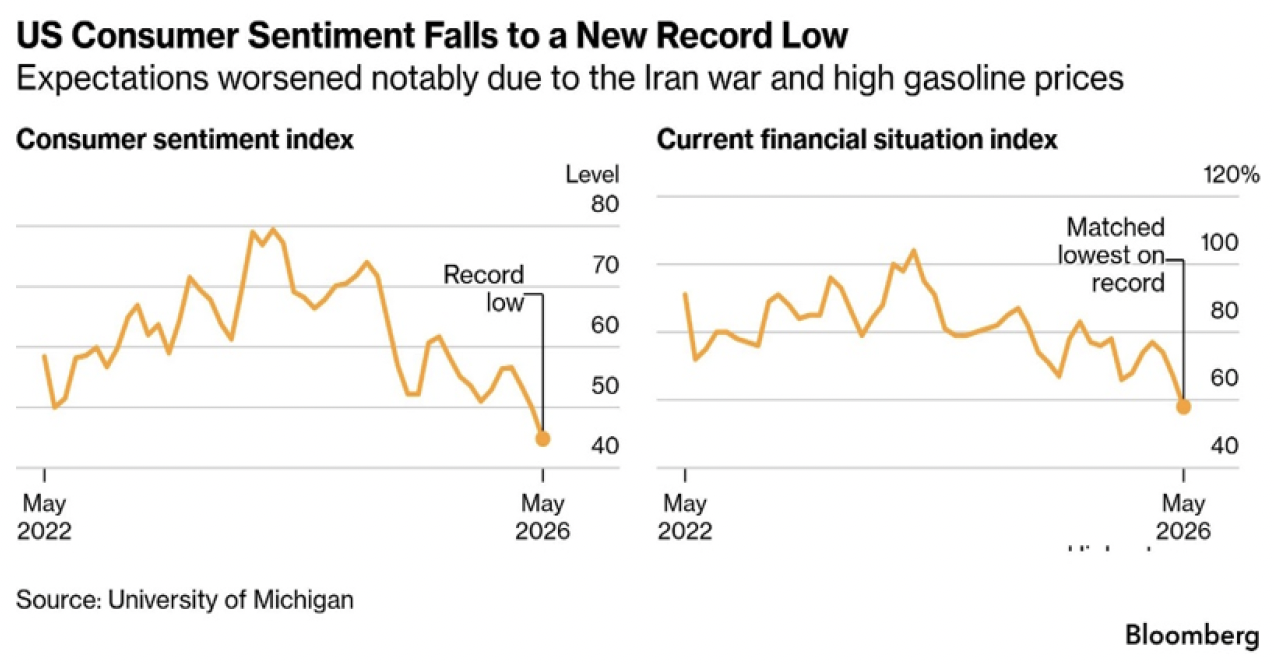

While earnings have been rising and stand at very healthy levels, consumers’ sentiment has been dropping and now stands at the lowest level in the last several decades, as shown below.

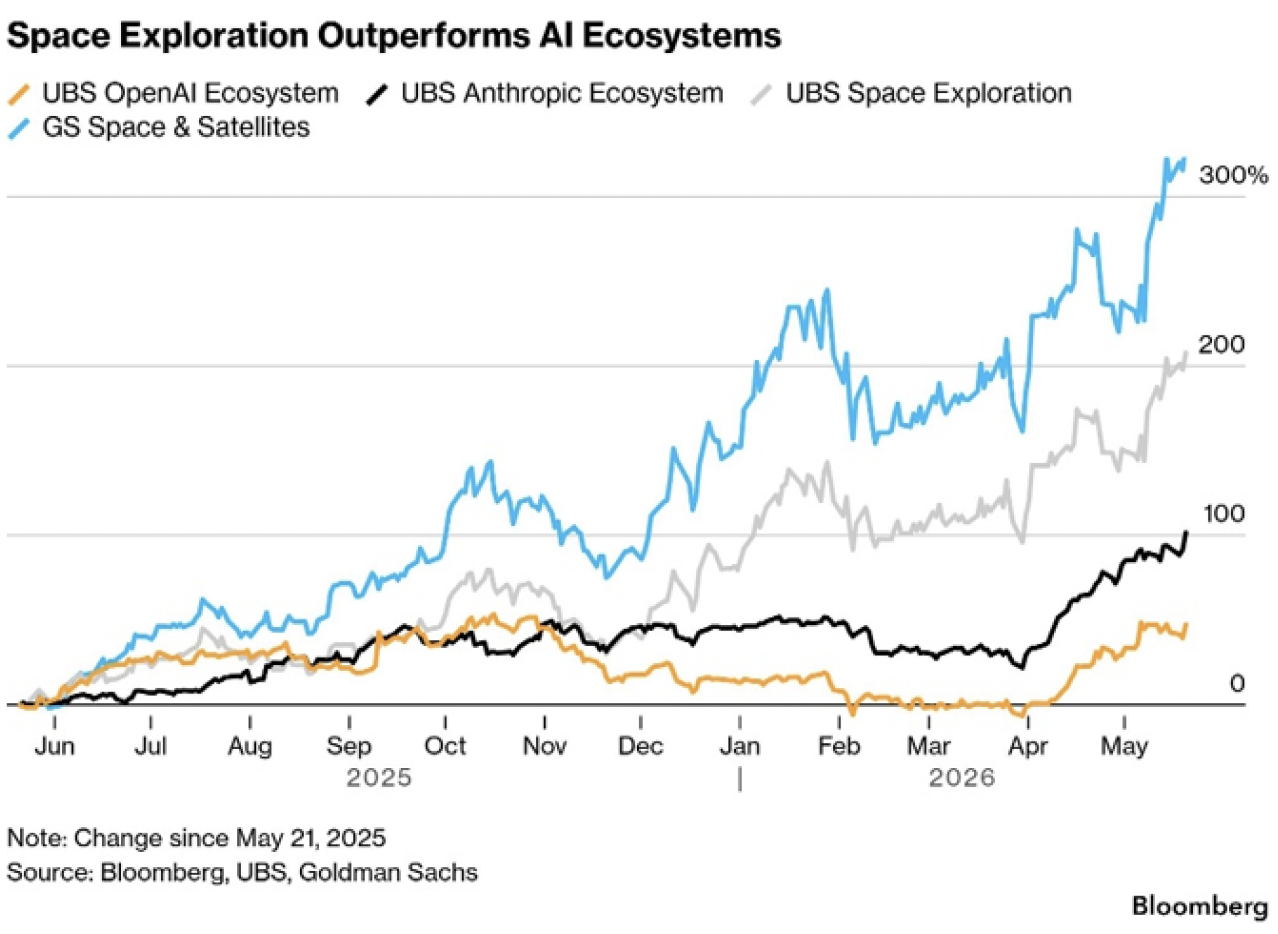

The promise and premises of AI and its effect on growth and productivity are well understood. The pessimism in consumers could be explained due to inflationary pressures (that might get worse), the political situation around the world, the war in Iran, the potential jobs apocalypse (as The Economist recently stated), the squeeze in incomes felt for the middle class, the rising yields that make financing more expensive, and the slowing comprehension of unstainable debts which historically have been the marks of major conflict around the world. At the epicenter of the equities’ upswing have been makers of semiconductors. Chip makers from South Korea, Japan, Taiwan, the EU, and, of course, the US are having a party. More speculative plays (like in quantum computing and the policies around it) contributed to another tech-related party over the past few days. On top of these developments, the SpaceX IPO (and its ambition to put 1 million inhabitants on Mars) led this past week to another boost in space-related and satellite stocks, as shown below.

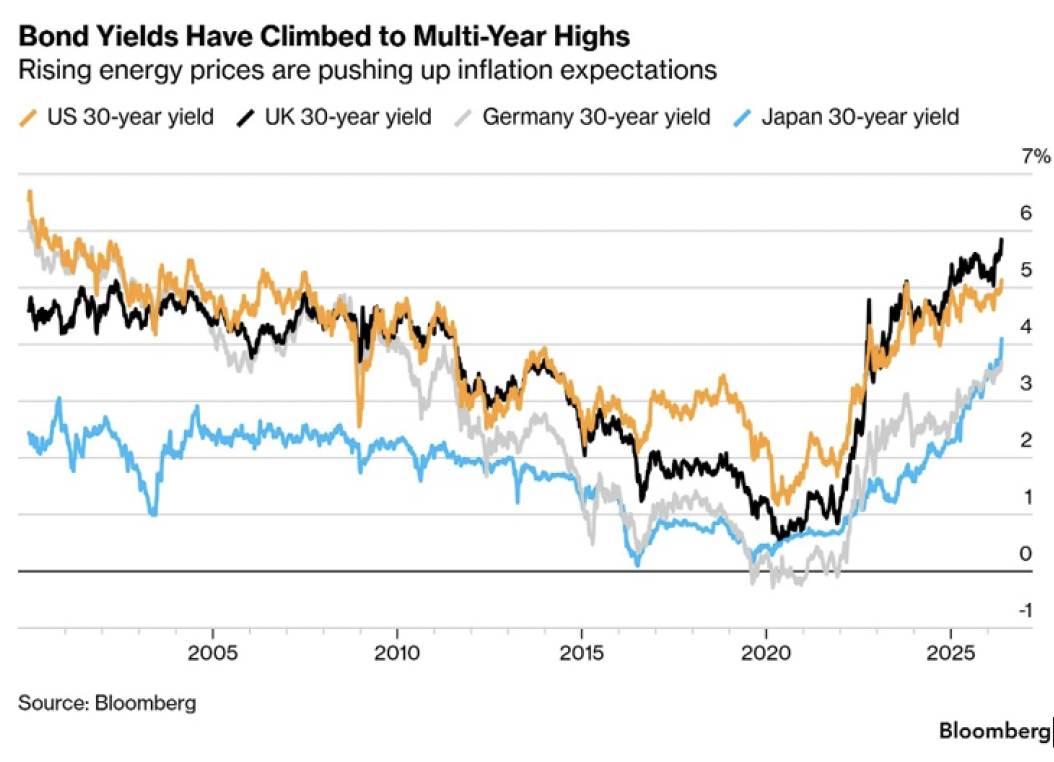

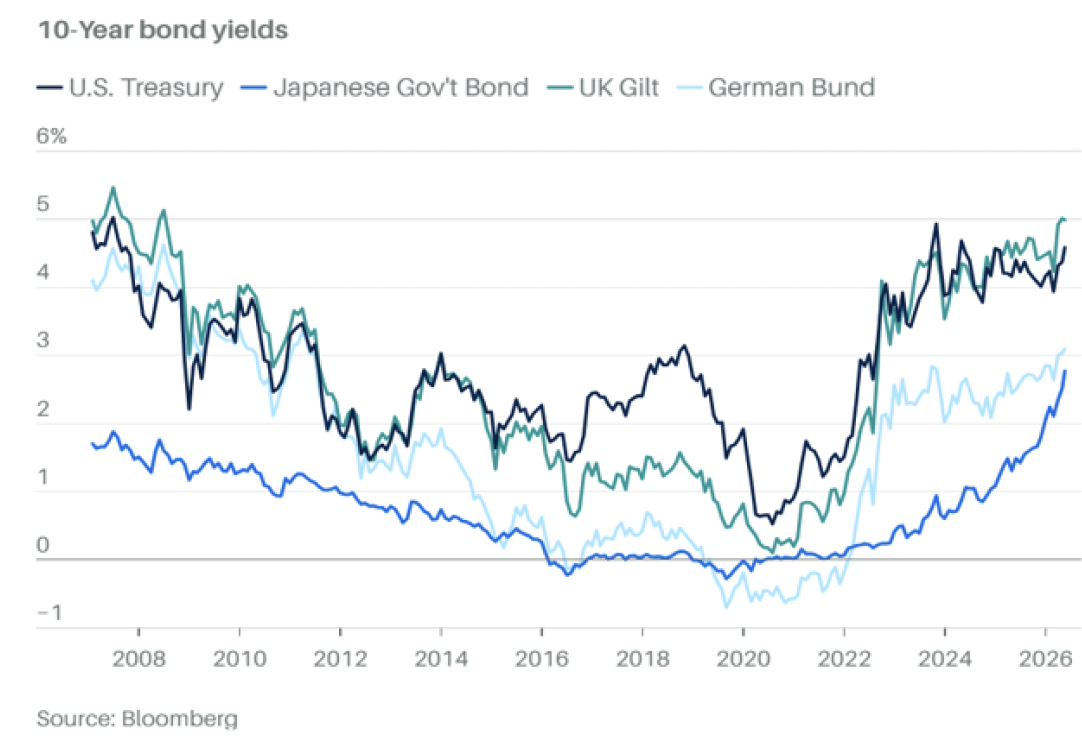

The equity mosaic is contrasted with the bond mosaic. A clear picture has emerged in the last few weeks: Rising yields around the world (see two graphs below on the 10- and 30-year bonds around the world) send a message that price pressures are becoming a serious problem that central banks must deal with by raising rates. The fact that central banks continue following an expansionary monetary policy (due to the simple fact – and not only – that their short-term rates are below inflation) reminds us of efforts to extinguish fire with gasoline. Of course, rising yields make financing – including government financing – more expensive, whose consequences could be significant.

Five years ago, the 10-year Treasury stood at 0.50%. Now, it stands at almost 4.6% due mainly to government profligacy. The fact that deficits keep rising is indicative of troubles down the road. When inflationary pressures are added to the picture, the clouds become darker. The Congressional Budget Office (CBO) estimates that over the next decade, the budget deficit (which is added to the rising debt) will average 6.1% of GDP, without recession! Rising deficits imply rising yields, which make the deficit even more expensive to finance, and force governments to pay more and more interest on the debt. Already, the US pays over $1 trillion annually on its debt. When the costs of financing the debt exceed the GDP growth rate (a fact for the US, the EU, and Japan), history tells us that major decisions need to be made that change the course of geopolitical developments. Rising yields abroad are now competing with US yields, which in turn could lead to sales by foreigners of US Treasuries, with the result being even higher yields! More corporate spending (especially related to AI, data centers, hardware, and electricity) will nudge rates too.

In the late nineteenth century, Britain squandered its global position through unnecessary wars, uncertain strategic positions, lack of planning, absence of vital alternative options and contingencies, let alone a domestic social and economic decline of its middle class. Nowadays, unsettled alliances, autocrats, imperial dreams, revanchist powers, territorial expansionary plans, nationalism fed by unbiblical theocratic visions, and a rapidly changing technological front, create an amalgam of uncertainty that traditionally results in a major war around the world.

Julius Caesar acquired two paintings by Timomachus. The first of Ajax during his madness, and the second one of Medea, when she was meditating on the slaying of her children. The Golden Fleece was Jason’s path to regaining power, yet he could not obtain it without Medea, the local princess of Colchis. Despite her crucial role in his success, Medea ultimately killed her own children as revenge for her husband’s rejection. When Timomachus painted Medea, he put two souls into the soulless image of her form. One reflected the jealousy of her husband, and the other her love for her children. Timomachus managed to tell us that we are dragged in diverse directions, like the equities and the bond market. Is Jason and his Golden Fleece today’s AI? Who is Medea, and who are her kids to be sacrificed?