The Wooden Nickel is a collection of roughly a handful of recent topics that have caught our attention. Here you’ll find current, open-ended thoughts. We wish to use this piece as a way to think out loud in public rather than make formal proclamations or projections.

1. Software Transitions

Just under 15 years ago, Adobe began the transition from selling its software from a buy-once, use forever type of model (called a “perpetual” license) to one where users could pay a monthly subscription fee and have their software always updated with the latest tools, features, as well as security and support; your version was always the latest and greatest. While it wasn’t the exact birth of the SaaS era, it was certainly a milestone event given Adobe’s dominant market position and envious financials, regularly posting sales growth of 20%-30% with Operating Margins in the high 20s and mid-30s.

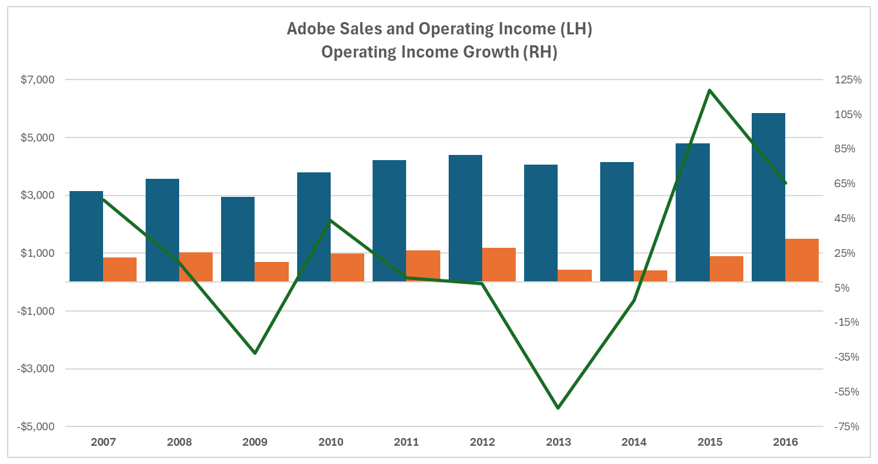

Figure 1: Adobe’s Transition to Cloud

Despite the Cambrian Explosion of software and cloud businesses that would follow for a decade plus, the transition was anything but clear and painless. After the 2011 presentation and announcement Adobe made to investors and Wall St analysts, sales would stagnate for roughly the next three years. Operating Income collapsed 64% in 2013 on the business transition; for context, operating income only fell 33% in the aftermath of the GFC. It would take 5 years for Operating Income dollars to recover their pre-SaaS peak. 5 years of no Operating Income growth. After those years, of course, the coast was clear, but only after substantial new investments in distribution strategy, corporate restructuring, handholding of customers and investors, and lots of work.

Much about the micro-economics of AI (especially from an end user perspective rather than training of new models) is largely under wraps, given that the major innovators are mostly private (OpenAI and Anthropic) or within a larger behemoth (Google and Meta). Larger macro and industry-wide prognostications have been made with the SaaS industry in the crosshairs; if software takes away jobs, then selling a license on a per-user basis is a melting ice cube. And so at best, we have another transition before us in the software space that will be greeted with a myriad of tactics and strategies (new product development, new go-to-market strategies, new pricing structures, partnerships, M&A, etc.). At worst, we have a terminal value question. In this current market regime, markets have taken a “better safe than sorry” approach, meaning, assume the worst (terminal value impairment) rather than stick around and hope for the best; stocks that used to trade on an EV to Sales metric now can often trade at GAAP earnings multiples. That’s been the level of price destruction. It’s shoot first and think and analyze later.

Well, we may now be getting some interesting data points regarding what they’re shooting at in the first place. Take ServiceNow’s. For a long time, the company was one of the best SaaS stories: a strong technology stack with sticky customers who loved the product, a clean history of growth without M&A, a strong financial profile, and year after year of 20% plus growth. It has been almost as early and active an adopter and partner to LLMs as you could ask for among the major public software companies. Yet it too has been caught up in the software slump, down over 60% from its high last September. In its most recent earnings call, the following data point disclosed by its CEO caught attention:

“I know many are interested in the progress of our hybrid business model, especially with regard to consumption pricing. You’ll be happy to know that 50% of net new business now comes from a non-seat-based pricing model.”

It’s certainly an encouraging data point if you’re under the belief that a software business will have to show AI-sourced acceleration in its top line to fight back against the drawdown (or else morph into an entirely different operating model). But if we apply a little bit of analysis to those incremental, consumption dollars, the hit to profitability brings up other concerns: how much margin are you willing to give up to see sales growth reaccelerate?

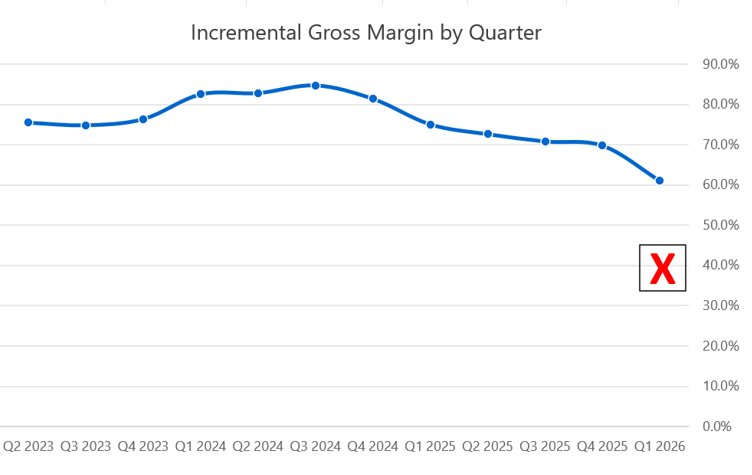

Figure 2: ServiceNow Incremental Gross Margin % and Consumption Gross Margin Estimate

The blue line represents the incremental gross profit margin for every additional $1 of sales to ServiceNow for the past 10+ quarters. For every additional dollar of sales made by the company, roughly 80 cents was left over to cover operating costs. That level has drifted down in the last year as additional cloud investments weigh on the company.

The red x, however, denotes an estimate of what the gross margin level would be on just the portion of new business that is consumption-based, i.e., the portion not sold on a per-seat license basis and is instead sold as consumption of invoking AI products. The only assumption behind the math is that the remaining new business is indeed subscription and holds to historic Gross Margin rates. If that’s the case, then we can see that new products have roughly half the historic unit profitability that the SaaS business does. If you have half the gross profit dollars left over to run your business, that will require an enormous rethink of how resources get divided and organized internally before impacting your bottom line.

Here’s the ironic thing: strictly from a pricing perspective (not a business strategy or technology strategy view), it’s most likely the right approach. Trying to protect your gross margins in an era of technology transition is a textbook error in the greatest stories of disruption history. But it still may not be enough.

2. Microsoft and OpenAI Make a Deal

Last week, Microsoft and OpenAI amended the terms of their business relationship, once again. What was once an exclusive arrangement between financial capital, technical infrastructure, and product distribution on the one end and innovative IP in the hands of a non-profit on the other has dissolved into a much more standard affair.

It is not simply the result of a falling out of trust after the brief dismissal of OpenAI CEO Sam Altman a few years ago. In fact, that lack of trust may not be the primary motivation for this latest revision to terms. Both companies stood at a crossroads where the greatest likelihood of success for each company, respectively, as things stood today, required being unattached from the other.

For OpenAI, it has enormous technological costs and even greater spending ambitions in the near future ($600 Billion by 2030, reportedly). Spending of that magnitude requires serving as many customers as possible in order to amortize costs over a wider base. The greater distribution of costs improves the economics of the business, which buoys the ability to tap the markets for another capital raise should OpenAI increase infrastructure investments further. By being locked into one cloud (Microsoft Azure), OpenAI’s potential growth was held back; after all, the largest cloud service provider in the world is Amazon.

For Microsoft, it’s been clear for quite some time that CEO Satya Nadella does not want to be commoditized away; he does not simply want to be a raw provider of chips and other hardware. Doing so surrenders his moat and sacrifices any differentiation. This was only further emphasized, albeit not head-on, in January during earnings:

“Sometimes I think it’s probably better to think about the Azure guidance that we give as an allocated capacity guide about what we can deliver in Azure revenue, because as we spend the capital and put GPUs specifically, it applies to CPUs, but GPUs more specifically, we’re really making long-term decisions.

And the first thing we’re doing is solving for the increased usage and sales and the accelerating pace of M365 Copilot as well as GitHub Copilot, our first-party apps. Then we make sure we’re investing in the long-term nature of R&D and product innovation. And much of the acceleration that I think you’ve seen from us in products over the past bit is coming because we are allocating GPUs and capacity to many of the talented AI people we’ve been hiring over the past years. Then when you end up, is that you end up with the remainder going towards serving the Azure capacity that continues to grow in terms of demand.”

To translate: GPUs are a scarce resource. When we (Microsoft) secure them, our first priority is being able to serve our own products. Our second priority is internal R&D for new products. Our third priority is making them available for rent to others, whether that’s OpenAI or someone in the Fortune 500 experimenting with AI.

Allocating computing resources in this manner is not conducive to current growth; in fact, management explicitly stated that growth would be higher on current financials if they just rented them all out. But if you’re looking to deepen your relationship with 250 million Microsoft users rather than just feeding the upstarts, it’s a smart terminal value bet.

But keeping GPUs for Microsoft products first and second means a cap on OpenAI’s growth and product development. And that means IP that Microsoft misses out on and cannot incorporate into its own products. Finally, Microsoft is still a significant shareholder in OpenAI with a stake of ~27% in the now for-profit entity. Stewarding that investment required letting OpenAI grow as efficiently as possible.

Which leads to the current arrangement, though it’s more of a separation on the margins.

But it all begs the question: if these two companies, who have been at the heart of the development of LLMs and AI infrastructure, keep needing substantial alterations to their terms of engagement, then how can anyone have certainty about how any part of this AI race is going to play out?