Once, Henry Kissinger observed that “the attempt to achieve the ultimate in a finite period of time can produce extraordinary disasters.” The agora of ideas demands the best possible answers. The agora of policymaking/strategy demands preparation for the worst possible outcome. The main risk in the first agora is that the important can drive out the urgent. The main risk in the agora of policymaking is that the urgent can drive out the important. Welcome to the dilemmas of the current market for equities, debt, derivatives, and hybrid instruments. The inevitability of tragedy should always be taken into account, especially at times when the Fed might be playing with the fire of loosening its monetary policy and committing the carnal mistake of targeting interest rates while manipulating its balance sheet (see discussion at the end of this commentary).

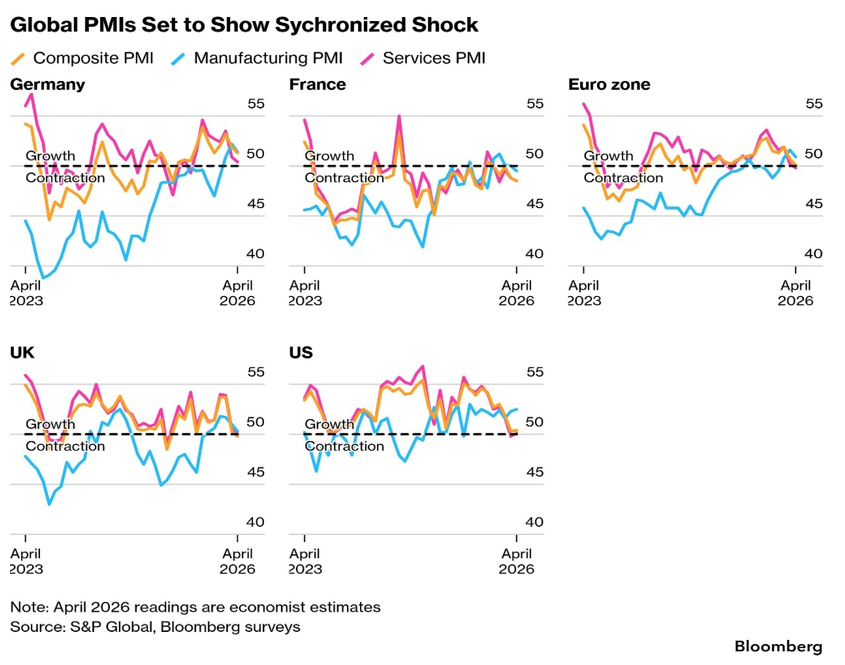

Recent articles (see here and here) are trying to explain how the market defies the current geopolitical circumstances. Marcus Tullius Cicero taught us that the ideal management of current affairs should combine experience in managing such important matters with the mastery of a philosophical understanding, i.e., how to operate within the limits of the possible. So, as we encounter the possible, we cannot escape the reality of the following graph.

What conclusion can we draw from the above? Could it be that there seems to be a synchronized contraction of global PMIs (in both manufacturing and services)? So, if that is true, why did the market recover its losses, and why does it keep charging upwards?

An immediate answer, which certainly carries some good weight, can be twofold: First, earnings –especially of tech-related companies – are good. Second, as forward earnings rise, the Price/Earnings (P/E) ratio drops, so the once assumed overstretched valuations look more reasonable now. Taking these two explanations as given, how then could we incorporate the reality of heading into the worst possible energy crisis of the last fifty years?

Of course, amidst such market enthusiasm (especially when “breaking news” of an imminent deal with Iran flashes on our screens), we should also be asking whether such momentum is dislocating reality (maybe even creating its own reality), resulting in mispricing and misallocation. Even if enthusiasm and momentum are sustained by the axiom of keeping money in the market during turbulent times, the reality is that volatility becomes fertile ground that exacerbates risks when it is augmented by loose monetary policy, especially in the absence of a pertinent philosophical paradigm.

When a realistic plan (in investment/politics and other arenas) is complemented by a solid/anchored philosophical idea/understanding, then a door to great and lasting consequences is opened. From a historical standpoint, when Byzantine Emperor Justinian collaborated with Tribonian (December 530 AD), the Corpus Juris Civilis was produced, which systematized Roman law and became the basis of our modern legal system. Towards the end of the eleventh century, in Bologna (the epicenter of the Renaissance’s legal rebirth), Irnerius resurrected that code which formed the basis of ratio scripta, a.k.a. written reason, to welcome Reformation and then Enlightenment. Later (in 1803), Napoleon collaborated with Portalis and designed the Civil Code, which is Napoleon’s greatest achievement. A few years before that took place (1776), a remarkable group of revolutionaries in the US steeped on the writings of Plato, Aristotle, Locke, Montesquieu, and Blackstone and designed a framework for the world’s most successful democratic experiment. When Paul Volcker accepted the chairmanship of the Fed (summer 1979) and told President Carter that under his leadership the Fed’s new policies will become the foundation of his political defeat the following year, but also the foundation of lasting economic prosperity, he had solid philosophical foundations in the concept of predictability (i.e., if inflationary pressures are defeated and predictability returns to the economic arena, then the economy and the markets will prosper for decades to come), based on his readings of Hume, Laplace, and Popper. Those readings (among others) can help us start comprehending the power of deterministic outcomes in providing a rational basis of action and reaction, both empowered by computational limitations and chaotic dynamics (butterfly effect).

So, which are the drivers for the equity markets’ rebound and upswing? As stated above, here is our list of suspects:

- Good earnings

- AI and tech momentum that uplifts the overall market

- Rate cut expectations

- Boomers’ $80+ trillion nest that boosts spending and thus GDP growth

- Global Wealth effect/recycling of savings

- Deficits which prolong a prosperity bought on credit

However, we believe that the most important explanation of why this is happening is due to the velocity of capital, a term that cannot exactly be found in academic circles. As velocity of capital expands along the lines of collateralization, securitization, and margins, then ample funds circulate around, which are partially funneled into the markets too, which consequently rise, not so much because of fundamentals but because of higher velocity of capital. The velocity of capital empowers the entire financial system to use its projects (e.g. data centers) and its “paper wealth” (e.g., portfolios) to create more “purchasing power.”

In bull markets, the ratio of capital velocity over GDP overshoots and makes the economy look even stronger, creating a feedback loop mechanism of feeding even higher market averages. In bear markets, the ratio can undershoot the real economy. When debt is paid down (deleveraging), or when the Fed shrinks its balance sheet, it acts as a negative velocity, sucking liquidity out of the system even if companies are still building factories (CapEx).

When the thymos (spiritedness/fire in the belly) of the soul complements the eros of the mind, then the likes of Cicero and Edmund Burke surface who prepare the oceans for smooth sailing.