Louis XVI had his own Machiavellian vested interests in mind when he decided to assist in the American war for independence. His reward was a lost throne, a guillotine, and a number of un-Machiavellian claims related to universal rights. The French Revolution a few years later gave ground to the era of Terror and was followed by the reign of Napoleon. On June 24, 1812, Napoleon decided to cross the river Niemen with over 600,000 troops that separated the French-controlled territory from the Russian empire. On his retreat from the Russian front, the exhausted French troops wouldn’t exceed 90,000.

Crossing micro waterfronts could have severe macro implications for Napoleon, as Xerxes in Hellespont and Julius Caesar in Rimini had learned before him. As Napoleon was advancing deeper inside Russia, the Russians were retreating. Finally, his troops confronted the Russian forces in the small village of Borodino, just 75 miles outside of Moscow, on September 7th, 1812.

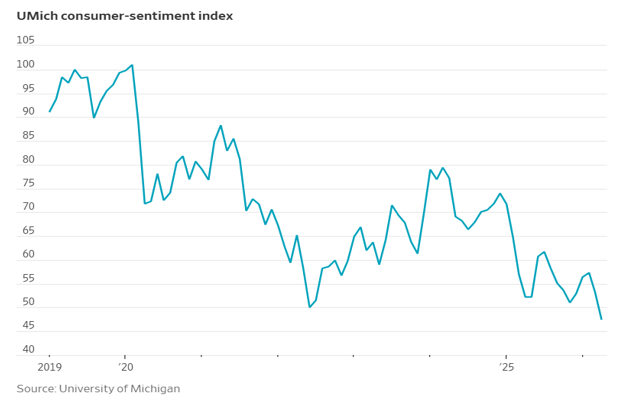

The markets started off this year with the aura of optimism. Then, concerns over AI turned the mood sour. The war with Iran exacerbated those concerns, with the Nasdaq experiencing a correction. However, optimism seems to be returning as fears retreat. Despite known unknowns such as rising inflation and declining sentiment (see graph below), the markets take a condescending and complacent view of those risks.

The scar tissue left over from the war (assuming a holding truce) could be lasting, leaving global markets with elevated energy prices (the damage to Gulf infrastructure is significant), elevated yields (due to higher inflation), and consequently slower growth. The drop of the dollar following the announced truce might be indicative of the fragile financial architecture. The grammar of investing in a fragile environment depends on its oxygenation. The nature of oxygen serves a dual purpose: First, it cannot be seen, but without it, we cannot live; second, the higher we go, the thinner the oxygen becomes.

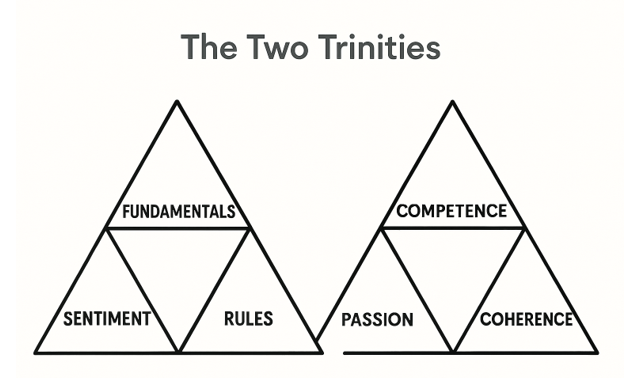

Nowadays, the landscape of investing faces two trinities: In the first trinity, investors evaluate fundamentals (such as earnings and rates), sentiment (such as consumer and business confidence), and rules (guided by risk analysis). In the second trinity (that of fragility), the investors face the competence of the decision makers, the passion of the combatants (whether it’s geopolitical or geoeconomic conflict), and the coherence of the political objectives.

However, the problem lies in the fact that in this fragile landscape, balancing between those trinities reflects an exercise of an object suspended among three magnets. As the pendulum swings, investment exercise dances between order (the first magnet) and chaos (the opposite second magnet). The third magnet shifts the oscillation from regularity to randomness.

War reflects politics, which (if politicians act within reason) should be subordinated to policy, otherwise it could turn out to be useless violence as the means (war) are isolated from the purpose. Similarly, investing has a purpose (growth, income) which is accommodated by strategic means (equity, debt, hybrid), unless someone believes in throwing darts to make selections of names to invest in.

Xerxes’ crossing of the Hellespont and acting on impulse, believing that his massive forces would humiliate the Greeks, backfired, and not only were the Persian forces humiliated, but they suffered irreparable damage. No one could dispute Julius Caesar’s genius. However, his actions by crossing the waterway of the Rubicon at Rimini brought a civil war, ended the Roman Republic, and became the foundation of political and monetary instability (as future emperors would bribe the army – to retain favor – by devaluing the currency). Similarly, Napoleon’s crossing of the Niemen River gave him temporary satisfaction of invading Russia and seeing Tsar Alexander’s I army retreating and even abandoning Moscow. However, within weeks, the sense of defeat was evident in his army, and he started his withdrawal, only to face the winter catastrophe on his way back to France, amplified by Russian attacks. At the battle of Borodino, the French pyrrhic victory coronated the Russian general Mikhail Kutuzov as one of the very few figures in military history who accomplished so much by appearing to do less, as Tolstoy explained in his novel War and Peace.

It’s not the place to discuss the vulnerabilities of the economic system due to chokepoints and single points of failure capable of creating massive and costly disruptions, but it might be worth highlighting some on top of the headlines related to the Strait of Hormuz:

- Strait of Malacca between Malaysia and Indonesia; Suez Canal; Panama Canal

- Japanese dominance of microcontrollers and engine airflow sensors, as we witnessed a few years ago

- ASML’s dominance in producing ultraviolet lithography equipment, which is required for advanced semiconductors

- Rare earths’ mining (60%) and processing (90%) controlled by China

- A financial architecture that is overburdened with debt, unfunded liabilities, and questionable rehypothecated assets

The master strategist Carl von Clausewitz, in his unfinished masterful work titled On War, calls the battle of Borodino Napoleon’s “culminating point”, as the French defeated themselves by exhausting themselves. “Genius does not constitute in a single appropriate gift – courage, for example – while other qualities of mind or temperament…are not suited to war.” Clausewitz’s answer lies in the marriage of strategy and imagination, or what he calls coup d’ oeil, a.k.a. an “inward eye.” The strategy maps out possibilities, alternatives, and frictions that can derail the whole enterprise. Ascending costs wear out plans and entrap pursuits into ignoring fundamentals. Similarly, investing by ignoring anchors and fundamentals emboldens defeat rather than an investment plan that embraces liberating but calculated risks with clearly marked exits.