The Wooden Nickel is a collection of roughly a handful of recent topics that have caught our attention. Here you’ll find current, open-ended thoughts. We wish to use this piece as a way to think out loud in public rather than make formal proclamations or projections.

1. Where Does SaaS Go From Here?

The selloff in software stocks that started in December and crescendoed in the first quarter of the year crystallized two chronic issues hiding in plain sight for most (but not all) software companies: software as a group had a valuation problem and an (lack of) innovation problem. Software companies, and their management teams, still believed they lived in a world of elevated multiples (on sales, not profits) even though growth peaked years ago. Related, as maturity in growth was brought forward, it wasn’t met with financial stewardship; bloated cost structures, excessive stock-based compensation, and minimal capital return programs were the norm.

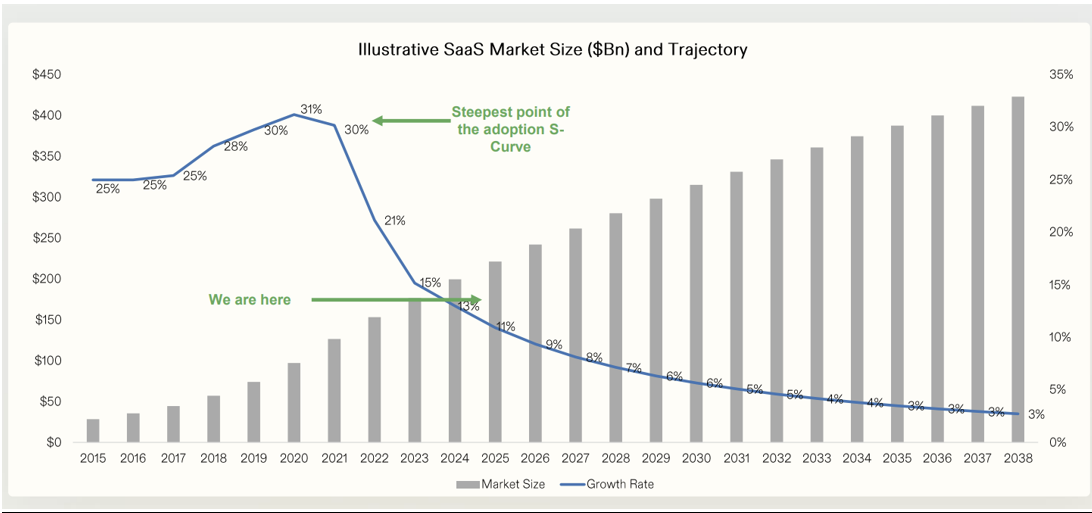

Figure 1: Growth Has Dramatically Slowed, Source: Avenir

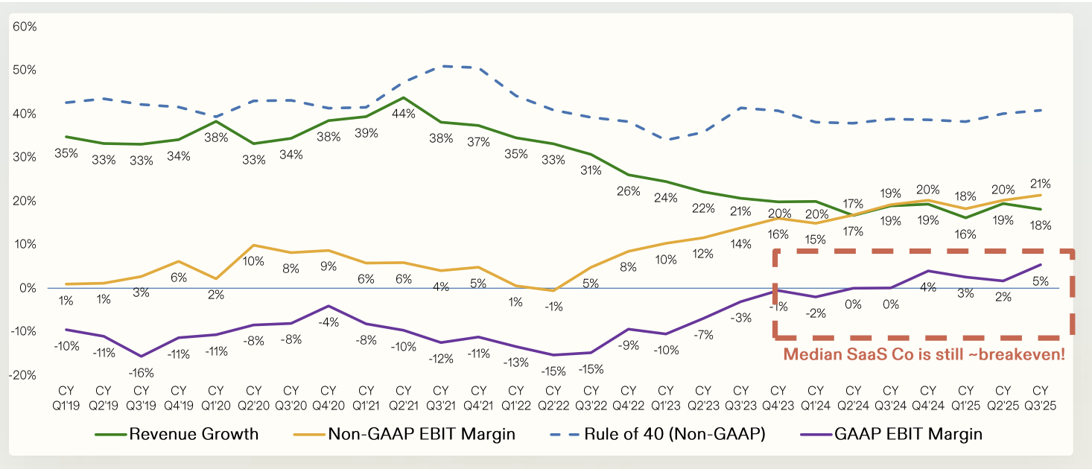

Figure 2: The Median SaaS Company Barely Breaks Even, Source: Avenir

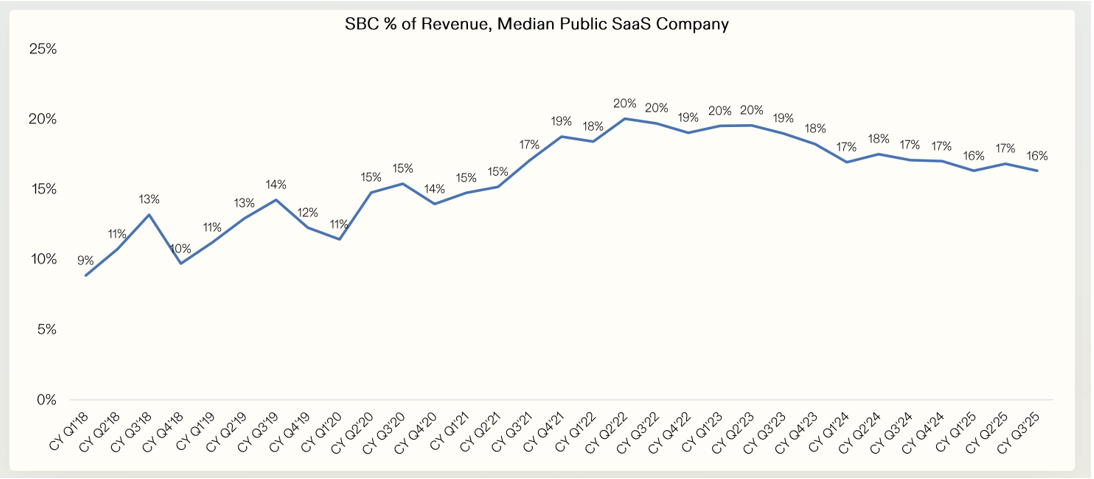

Figure 3: Cost Structures, Like SBC, Have Not Matured, Source: Avenir

The old saying that there’s an inherent race between “innovation finding distribution before distribution can find innovation” has come to the forefront. The development of coding agents has lowered the barriers and costs of developing software in the first place. But that belies the real issue; lines of code have never been the moat for these businesses. Free, open-source software has existed for decades, if companies wanted to take hold of it themselves and run their own technology systems. If costs were the motivation, insourcing would have taken place long before the development of generative AI.

The bigger issue is that the development of LLMs, when paired with agents, has raised the bar for what a software application/platform should be, what it should look like, how it should function, and what it should be able to accomplish. As a result, software companies are having to fight two battles at once: drastically increase their productivity and innovation pipeline while getting their cost structure in line. The former demands more attention to R&D as opposed to the giant sales forces that have been built over the last decade plus. It’s a new, different set of muscles than what they’ve had to use. The latter demands that those investments ultimately show up in the bottom line rather than just the top line.

Going forward, a number of areas will serve as critical pivot points for understanding the industry’s evolution.

- There will be significant turnover in management teams. In fact, this has already started with the founder of Workday returning as CEO and the retirement of Adobe’s CEO.

- Some companies will try to deal their way through the challenges via M&A. Will they try to merge legacy business models to try and wring out efficiencies with greater scale? Or will various software adjacencies be brought together for models to work across a greater landscape and work across more touchpoints?

- How will monetization models shift and evolve? Will LLMs and agents be built into existing license agreements? Will seat-based pricing go extinct and make way for companies to charge for outcomes?

- Who is the bigger threat to incumbents: the giant AI labs or new startups built with AI at the start?

- In what industries or positions will an incumbent position be helpful? Where will having data be useful to make the transition? After all, there was a point in time in which Salesforce, ServiceNow, Workday, etc. didn’t have any data. They were the upstarts. And they took share on the basis of a different value proposition. Will AI unfold the same way?

2. Meaningless Metrics

In the elusive quest to find a “perfect” metric to trade with or against last month, some people clung to headlines about a race to cash as a sign that the worst is over. One such example from Bloomberg a month ago:

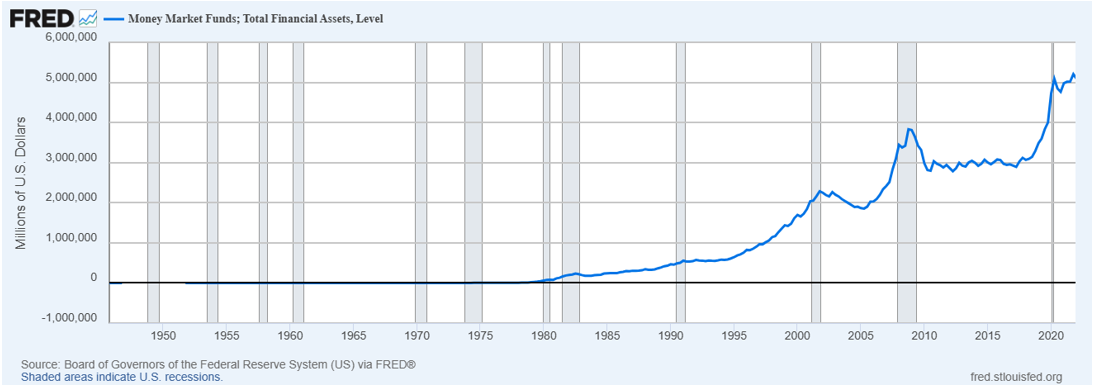

From the standpoint of a contrarian proxy, it is a classic Type 1 Error: assuming a signal where there is none. Just look at where balances of money market fund assets stood on the eve of our last bear market in 2022: at another record high.

Figure 4: Money Market Funds at All-Time High Prior to 2022 Bear Market

Notice some other all-time highs (at the respective time): on the eve of the Covid crash, the GFC, and the Dot-Com Bust.

Further, here’s where the market capitalizations of the current major S&P indices currently stand:

- S&P 500 Large Cap: $56 Trillion

- S&P 400 Mid Cap: $3 Trillion

- S&P 600 Small Cap: $1.5 Trillion

From their peak level during the GFC, money funds fell by roughly one-third. For argument’s sake, let’s ignore small and mid-capitalization stocks. Let’s ignore the Russell indices (which bring in further candidates for investment due to looser qualification rules). Let’s ignore every single other equity market around the world. Let’s ignore the entirety of the bond market (which makes global equities look like a rounding error). And let’s assume that roughly half of money funds get deployed into large-cap US stocks, or roughly $4 Trillion, a far greater percentage than seen historically. Your reward is a ~7% return assuming no other destination exists. Is this a compelling risk-reward? Is this a compelling thesis?

Not only would I enthusiastically say no. I would push back on the premise as irrelevant. The whole idea ignores the endogenous nature of credit/demand. With over $250 Trillion in invested assets globally, the ability to lever up in either direction is plentiful and isn’t accounted for in traditional metrics.