Welcome to our monthly newsletter which covers key developments in major non-US markets. With this newsletter, we highlight corporate, debt, and monetary policy news in European, Asian, and Latin American markets. We end this piece with a spotlight on commodities.

European Markets

Corporate and Business News

- UniCredit’s Commerzbank bid reignites cross-border bank consolidation, with scope for sweeter terms keeping European financials on M&A watch. The €35 billion bid and implied €30.8 per‑share valuation underscore intensifying pressure on European lenders to scale in response to squeezed margins and a more volatile geopolitical backdrop.

- Engie’s £10.5B UK Power Networks acquisition marks a landmark grid deal and sharpens investor focus on regulated‑utility scale and network growth. The transaction brings 8.5 million customers, 71 TWh of annual electricity delivery, and a £15.8 billion enterprise value into Engie’s portfolio.

- LSEG’s record £3B buyback, higher guidance, and firmer AI messaging trigger a powerful relief rally in UK market infrastructure. The company highlighted stronger‑than‑expected profit growth, expanded AI partnerships with firms including Microsoft, Anthropic, and Databricks, and a reinforced positioning as the “partner of choice” for licensed, high‑quality data.

- Schneider Electric beats on data‑centre demand, reinforcing Europe’s AI‑electrification winners across industrials, power, and automation. The company reported triple‑digit growth in its pure data‑centre segment and 10.7% organic quarterly revenue growth.

- Adidas disappoints on profit guidance as tariffs, dollar weakness, and Middle East disruption weigh on the consumer discretionary outlook. Management warned that U.S. tariffs and adverse currency movements will cut 2026 earnings by roughly €400 million, while store closures and logistics interruptions across the Middle East introduce further downside risk to both revenue and margin recovery.

- Europe’s defence trade gathers pace as Indra and Hensoldt post surging backlogs, extending the sector’s re‑rating on rearmament demand. Hensoldt’s order book alone has swelled to more than €8.8 billion—up over 60% year‑on‑year—reflecting accelerated procurement cycles across Europe as governments convert rising defence budgets into concrete multi‑year radar, sensor and electronic‑warfare contracts.

Debt and Monetary Policy News

- The ECB held at 2% but turns more alert on inflation, as the energy shock pushes euro rates markets from cut assumptions toward renewed hike pricing. Incoming projections now show headline inflation revised up to 2.6% for 2026 as the Iran‑related energy spike materially elevates near‑term price risks, prompting traders to price in one to two potential hikes later this year.

- BoE unanimously held at 3.75% jolts gilts, with a sharper inflation warning reversing expectations for cuts and reviving a hikes narrative. Two‑year gilt yields surged to their highest level since early 2025 as policymakers warned inflation could climb toward 3.5% in the coming quarters, signalling that even dovish MPC members see a higher bar for future easing.

- UK fiscal strains return to the foreground as borrowing overshoots forecasts and debt‑interest costs surge, driving a fresh risk premium into government bonds. February’s borrowing hit £14.3 billion—almost double OBR projections—while record debt‑interest payments amplified concerns that higher gilt yields and wartime energy pressures will continue to destabilise the fiscal outlook.

- Bunds lose some of their traditional safe‑haven edge as Germany’s heavier borrowing outlook and ECB balance‑sheet runoff erode scarcity support for core euro debt. Strategists note that rising fiscal issuance, combined with ECB portfolio reduction, has pushed Bund valuations to their cheapest levels since 2014, weakening their relative appeal versus Treasuries and gold during recent volatility.

Asian Markets

Corporate and Business News

- Apple posted a +23% surge in China smartphone sales in the first nine weeks of 2026, bucking a broader market decline as some Android phone makers raised prices in response to higher memory‑chip costs. The jump was driven by e‑commerce discounts and Apple’s eligibility for state subsidies on the base iPhone 17 model, reinforcing its ability to hold pricing steady even as competitors pass cost pressures to consumers.

- Tencent Holdings said it plans to increase investment in artificial intelligence this year, including developing proprietary models, after acknowledging that chip export restrictions held back its 2025 spending plans. Management said it will ramp up capital expenditure in 2026, expand AI talent hiring, and roll out upgrades to its Hunyuan model and OpenClaw‑based AI tools as competition with Alibaba and ByteDance intensifies.

- Tesla is looking to buy equipment worth $2.9B for manufacturing solar panels and cells from Chinese suppliers including Suzhou Maxwell Technologies as CEO Elon Musk aims to add 100 gigawatts of solar capacity in the United States. Suppliers have been instructed to deliver the machinery before autumn, with shipments expected to head to Texas as Tesla accelerates its goal of building 100 GW of U.S. solar manufacturing capacity by 2028.

- Taiwan’s Foxconn, the world’s largest contract electronics maker, said it expected strong revenue growth in the first quarter and the whole of this year, even as it posted a -2% quarterly profit decline, lagging estimates. The company attributed the profit shortfall partly to a higher tax rate but reiterated that surging demand for AI servers—where its market share could reach 40%—will drive growth through 2026.

- Samsonite shareholders approved a set of resolutions designed to pave the way for a U.S. dual listing, as the Hong Kong‑listed luggage maker seeks greater exposure to U.S. investors and improved share liquidity. The mandate allows issuance of up to 138.3 million shares for a potential ADS listing, though the company has not yet set a timetable and says any deal will depend on market conditions.

- AstraZeneca said it will build a cell‑therapy manufacturing and supply base and an innovation centre in Shanghai, aiming to become the first global drugmaker with end‑to‑end cell‑therapy capabilities in China. The facility will produce autologous CAR‑T therapies for China and other Asian markets, backed by a broader $15B investment commitment that includes expanded R&D and radioconjugate drug capabilities.

- Nvidia gets Beijing’s approval to sell the H200 chip, its second‑most powerful AI chip, to China. The regulatory greenlight allows Nvidia to resume H200 production and fulfill purchase orders from major Chinese tech firms after months of delays tied to dual U.S.–China licensing requirements.

Debt and Monetary Policy News

- The BoJ held interest rates steady but maintained its bias for tighter monetary policy, warning that surging oil prices driven by the Middle East conflict could exacerbate inflationary pressures. Governor Kazuo Ueda said the BoJ board was somewhat more focused on upside risks to inflation than downside risks to growth from the conflict, keeping alive market expectations for a near-term rate hike. BoJ Governor Kazuo Ueda said underlying inflation is accelerating toward the bank’s 2% target, stressing that price rises must be matched by solid wage gains.

- Japan and South Korea expressed concern about the rapid declines in their currencies, saying they were ready to act against excessive foreign-exchange volatility. Finance Ministers Satsuki Katayama of Japan and Koo Yun-cheol of South Korea “expressed serious concern over the recent sharp depreciation of the Korean won and the Japanese yen,” they said in a statement after their annual meeting in Tokyo.

- Nearly all major developed market central banks kept rates unchanged this week, but emphasized their readiness to act to curb inflation should the energy shock caused by the U.S.-Israeli strikes on Iran drive a broader surge in prices. Global bond markets tumbled as an intensifying U.S.-Israeli war with Iran pushed oil briefly toward $120 a barrel, heightening inflation concerns and fueling expectations that European CBs could tighten policy later this year.

Latin American Markets

Corporate and Business News

- EV maker Xpeng said it aims to double overseas sales this year to raise the contribution from international markets to 20% of revenue, as it prepares to launch its G6 and G9 models in Mexico on March 25. The Mexico debut marks a key step in its broader Latin American push after reporting its first-ever quarterly profit, as the company seeks growth abroad amid slowing demand in China.

- U.S. miner Freeport-McMoRan has begun the process of obtaining an environmental permit for a $7.5B expansion of its El Abra copper mine in Chile, the company said. The project, the largest mining investment submitted to Chile’s regulator since 1992, would lift output by more than 300,000 tonnes annually and could make El Abra the country’s third‑largest copper operation.

- Brazil could face fertilizer supply problems if the conflict in the Middle East does not ease soon, the nation’s farm minister said, criticizing sellers for sharp increases in local urea prices as analysts said farmers may turn to cheaper alternatives. Urea prices jumped about 35% in two weeks amid disruptions in the Strait of Hormuz, prompting concerns that farmers may be forced to switch to lower‑concentration nitrogen products.

- Ride-hailing application Uber will invest $500M in Argentina over the next three years, the Economy Minister said. The investment follows an “excellent” meeting with Uber’s CEO and will support the expansion of operations, including the relaunch of Uber Eats in major cities.

- E-commerce firm MercadoLibre expects to invest $3.4B in Argentina this year, Chief Executive Officer Ariel Szarfsztejn said. The plan represents a 30% increase from last year and includes expanding logistics, building new distribution centers, upgrading technology, and creating nearly 2,000 new jobs.

- Australian mining major Rio Tinto said it has secured a $1.175B financing package from four international lenders to support development of its Rincon lithium project in Argentina’s Salta province. The funding will advance construction of a plant targeting up to 60,000 tonnes of battery‑grade lithium carbonate annually, with first production expected in 2028.

Debt and Monetary Policy News

- Brazil’s central bank began a long-awaited easing cycle with a cautious 25 bps cut, holding off on explicit guidance for next steps as an oil shock tied to the U.S.-Israeli war on Iran stoked global inflation fears.

- Brazil’s 12-month inflation slowed in February to its lowest level in almost two years, official data showed, potentially paving the way for the central bank to kick off an easing cycle next week despite the recent spike in oil prices.

- Chile’s government has ordered a blanket spending cut of nearly $4B as part of a plan to improve public finances and safeguard social benefits over the medium term. Chile’s economy grew more slowly in 2025 than in the previous year, despite returning to growth in the fourth quarter. Full-year GDP expanded 2.5%, central bank data showed, down from a revised 2.8% in 2024.

- Argentina’s monthly inflation rate was 2.9% in February, stable from the level registered in the first month of 2026 but a tick above analysts’ forecast of 2.7%, official data showed.

Commodities Spotlight

Energy

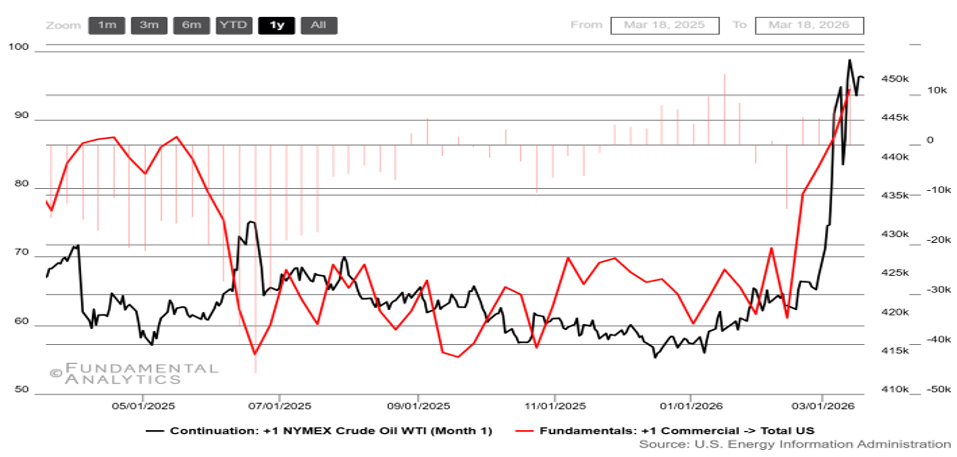

US-Iran conflict sent WTI above $100, +53% in ONE DAY!

Source: Fundamental Analytics

NYMEX WTI front-month exploded from the mid-$60s to near $100/bbl as the U.S.-Israeli conflict with Iran escalated, disrupting Hormuz traffic and exposing Gulf export infrastructure to repeated attacks. U.S. fundamentals were mixed; crude inventories built sharply on stronger imports from Venezuela and Mexico, while exports also jumped and gasoline and distillate stocks fell, signaling resilient product demand. In the end, geopolitics overwhelmed the bearish effect of higher U.S. crude stockpiles.

Agriculture

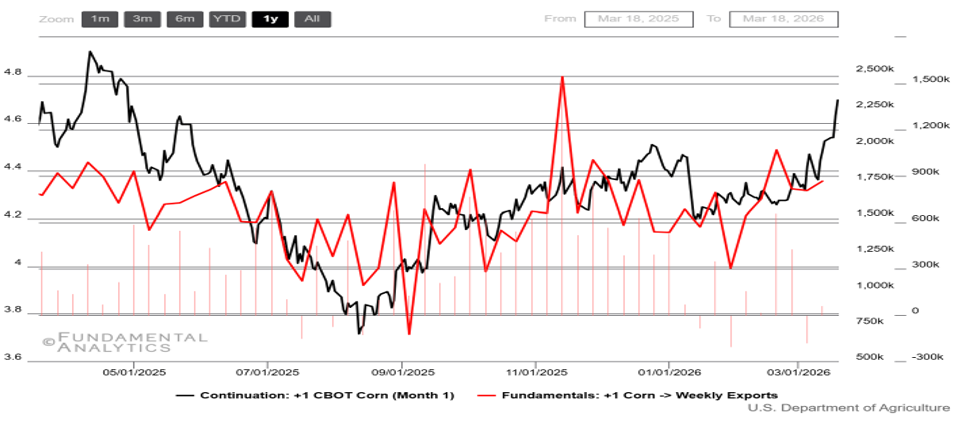

Corn in 8 months high on stronger than expected biofuel-demand and US-Iran conflict

Source: Fundamental Analytics

CBOT corn front-month rallied from oversupplied lows to its highest level since May 2025. Ample U.S. stocks and the overhang from a record U.S. crop initially capped gains, while the USDA still projected weaker 2026/27 exports amid tougher South American competition. Prices then strengthened as biofuel-demand expectations improved and the Iran war disrupted fertilizer and fuel markets, threatening Brazilian planting and export logistics and adding a broader geopolitical risk premium to grains.