The British Empire excelled in overextending itself in military, political, economic, and financial matters. Prior to that, at the turn of the fifteenth century, China was by all standards the most advanced civilization in the world. Around 1435, a movement of isolationism dominated and brought down the majesty of what the Ming Dynasty had accomplished. When political/geopolitical/geoeconomic policies misjudge and fail to follow a coherent strategy with concrete goals and exits, then a cacophony prevails where, instead of enjoying a concerto, the four rhythms (regular, alternating, flowing, and progressive) are mixed into a collision of sonic elements where competing tempos are marked by a mish-mash of unpleasant sounds. The four rhythms correspond to the four areas (military, political, geopolitical, and geoeconomic) that are primarily in the hands of governments. When to those four rhythms we add monetary and technological tempos – and depending on whether we have a concerto or a cacophony – then we may end up with a symphony (good scenario), or with very unpleasant sounds resembling the outcomes of the machine described in Kafka’s short story known as “In the Penal Colony”. We know from the writings of Immanuel Kant that the outcome is a function of the public moral philosophy administered by the State (see concluding remarks about Kafka and Kant).

For today’s commentary, let’s focus on two things: Facts of the war with Iran and questions surrounding that war.

Facts

- The tyrannical Iranian regime is a curse for its people and the world. Civilized world powers have a duty to restrain such regimes. However, the fallout from the war and rising energy prices expose vulnerabilities from valuations to credit concerns, and from rising deficits to the economic slowdown.

- Equity prices, bond prices, and precious metal prices are all declining in a synchronized manner as the dollar rises. The decline has not been significant so far, but it could accelerate if the war is prolonged and/or if the consequences are more severe than anticipated. Therefore, an additional drop of 10-14% cannot be excluded, with some analysts pointing out the possibility of a bear market.

- The equity markets are holding up due to earnings optimism supported by fiscal and regulatory measures, as well as by spending by retired boomers. That indeed provides a support level, as shown below, given that the 200-day moving average is holding.

- However, appetite is rising to target energy infrastructure in the Middle East region, which, if materialized, we will certainly be facing an energy crisis with economic and financial consequences that not only will boost inflation but also bring in a recession.

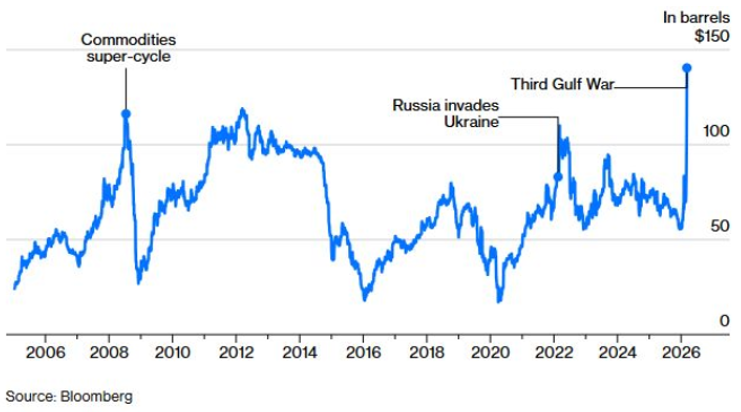

- If the world faces a second chokepoint besides the Strait of Hormuz (as discussed below), then refined energy products will face a squeeze that would be historic. To that effect, fuel oil prices (a.k.a. the bottom of the barrel) are skyrocketing, reaching levels not even seen in 2008 and 2022. This is a major problem for shipping that moves most of the world’s trade. If ports run dry, it will force shipping to a halt.

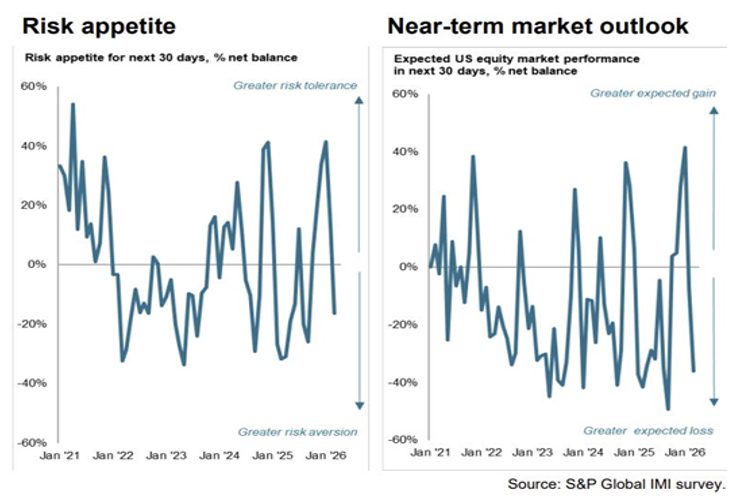

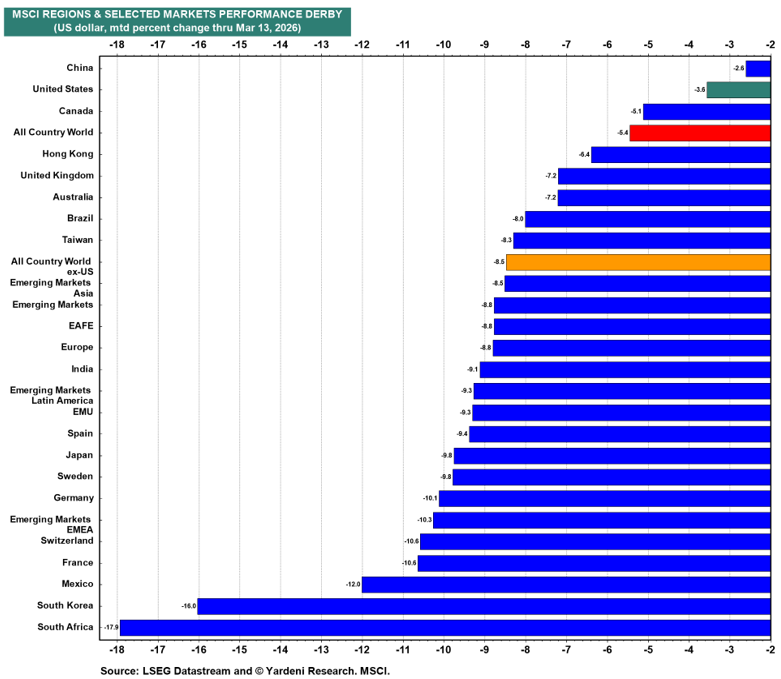

- Investment managers’ risk appetite, as well as their outlook, is becoming problematic, as it is shown below. The longer the war lasts, the worse both of those indicators will become. In that scenario, markets outside of the US will continue suffering more than US markets (mainly due to their oil dependency); however, the losses in US markets most probably will increase too. Hence, as the second figure below shows, we expect those international markets that are not already in correction territory to experience a correction too within two weeks if the war prolongs, and we also expect losses in US markets to exacerbate.

- The calculus of the conflict could change significantly if any of the following two scenarios occur: First, oil infrastructure (Iranian and regional) becomes a target. That would raise oil prices by at least 30% (from its current $100 level), with some energy analysts discussing a 50% increase. Second, if the Houthis start their attacks on the trade routes in the Red Sea again, then the world will be facing a second chokepoint in the Bab El-Mandeb Strait. Red Sea traffic carries about 15% of global trade and dominates Asian routes, especially for Europe. Rerouting through the Cape of Good Hope will add weeks to supply chains and, of course, will increase costs.

Questions

- Do we have our priorities right, and have we counted the costs?

- What will happen to the region, and what will be the global economic consequences on the Day After? Can the region and the world afford a chaotic civil war in Iran?

- Are we going to be better off following the war? By most scenarios, the emerging order in Iran will be chaotic at a time when valuable resources would have been spent. Could an emerging chaos in Iran engulf us in a long-lasting episode where bad judgment ends up squandering valuable resources?

- Will the outcome of the war embolden players like Russia and China?

- Could our resources have been used better in tech R&D, education, healthcare, and in developing alternatives to oil dependencies, especially when we consider that China is catching up on all kinds of tech developments, and our debt trajectory points to serious troubles starting in less than ten years? (Regarding the latter, it is a fact – as was reported recently by Kent Smetters, director of the Penn Wharton Budget Model – that from a pure accounting perspective, if we use the same standards that publicly traded companies have to use, our national debt is more than double what is being reported as $39 trillion when we take into account all obligations that the US has undertaken over the course of the next few decades. When we consider that the debt rises faster than the economy, and that several trust funds – including Social Security and Medicare – will run out of money within 10-14 years, then we should revisit the first fundamental question: Do we have our priorities right?

In Franz Kafka’s short story, “In the Penal Colony”, we meet a visitor who is shown by the colonial officer an ingenious machine which has been developed by his master. Any person who is accused or found guilty of an offense is strapped into the machine, which slowly and excruciatingly inscribes upon the body the law that was broken, and in the process tortures the person to death. The colonial officer happens to be so proud of the machine that he insists upon personally demonstrating its functionality to the visitor. So, the officer sets the machine to inscribe the words ‘Be Just’, and he places himself inside the machine. However, the machine starts malfunctioning so that instead of carrying out its intricate operation, it goes out of control and starts mutilating the officer, inflicting upon him an excruciating death.

Writing on the bankrupt moral philosophy of public action and course, Immanuel Kant in his 1785 Groundwork of the Metaphysics of Morals, laments the fact that it is not out of duty or morals that a course of action takes place, but rather out of self-love. Let’s listen to Kant: “Not that they have on that account questioned the soundness of the conception of morality; on the contrary, they have spoken with sincere regret of the frailty and corruption of human nature, which though noble enough to take as its law an idea so worthy of respect, is yet too weak to follow it…In fact, it is absolutely impossible to ascertain by experience with complete certainty a single case in which the maxim of action, however right in itself, rested simply on moral ground and on the conception of duty.”