As I was approaching the train’s platform in Washington, D.C., I observed that the wagons had been painted with the phrase “From R to R”. Strange, I thought. Is that a message/warning for an incoming recession?

I took my seat, and across from me, two familiar faces were conversing. “Good evening, gentlemen, I said.” “Welcome on board,” the gentleman on the left said, while rising and extending his hand to introduce himself as “Lorenzo de Medici, and here is the revolutionary Martin Luther,” he said.

“I get it now,” I said, “from the Renaissance that Lorenzo the Magnificent spearheaded, to the Reformation that Martin Luther initiated.” “We also need to talk about the Enlightenment that wouldn’t have happened without those two Rs,” Luther added. “I hope that before we touch on the Enlightenment we would be discussing that 40-year period that saw the likes of Boticelli, Leonardo Da Vinci, Michelangelo, Savonarola, and of course Machiavelli whose work still impact us today, without neglecting the corruption of the church and of the political powers of that day, which led to wars in Europe,” I added, before stating: “Gentlemen, your subject is of utmost importance as it is the crown jewel of those few 40-year periods in human history that are marked as revolutionary devolutions, but we have to take it up another time. Today, the focus should be on Schrödinger’s Cat.”

By the end of 2025, the consensus was that 2026 would be a good year for stocks and possibly bonds (implying price gains as yields were anticipated to decrease). The rationale for that was based on good earnings, AI euphoria, corporate spending, consumer spending (it’s the era of baby boomers’ retirement and wealth transfer after all), fiscal boosts via deficit spending and tax policy, and monetary expansion via the Fed’s expansion of the balance sheet, regulatory changes, and lower rates.

The problem is that as we are approaching the end of the second month, serious concerns have given credence to the possibility that the opposite may be happening. Those concerns focus on the sustainability and profitability of all that AI spending, while questioning valuation models and market multiples. However, if those were the main concerns, someone could say that’s what market evolution is all about. The problems arise because the concerns reach well beyond the questioning of valuations, and rather hit the core of the monetary system, the stability of the debt machinery, the geopolitical order, and touch on the engine of finance, a.k.a. war.

What is it then? Upswing or downturn? Welcome to Schrödinger’s Cat, a concept from quantum physics that describes the period during which more than one antithetical outcome could be simultaneously true or false. That period/state of events is called superposition, and the judgment call could not be made until a catalyst forces the opening of the box.

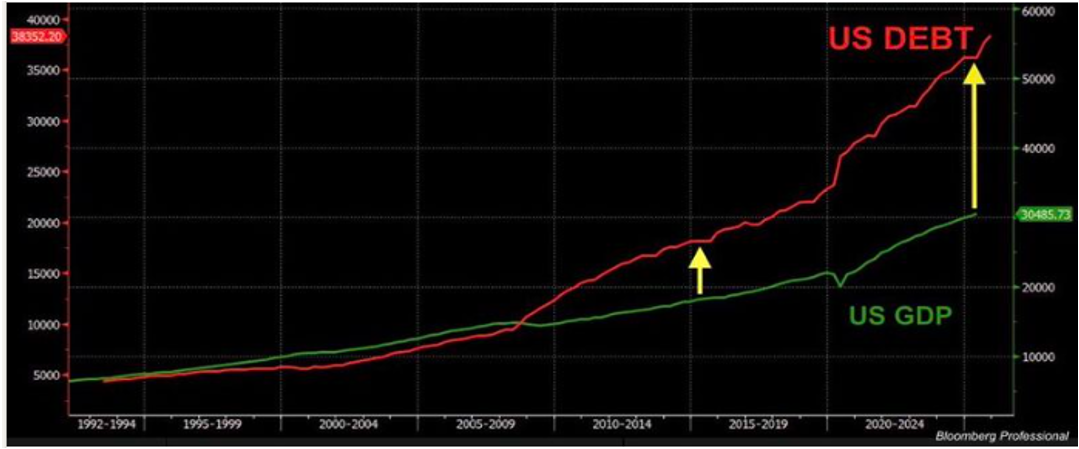

This is not a time of answers. This is the time of questioning the answers we have been provided. Let’s start then: Is the debt sustainable when primary deficits expand at a time when growth is taking place? Is the debt sustainable when it grows faster than GDP? Is the debt sustainable when the economy grows at a rate below the primary interest rate? Do the demographics support the debt expansion? Are the AI productivity gains capable of reversing possible debt unsustainability? For how long can we wait? And if the situation raises red flags for the US, then what can we say for China, where credit expansion is massive, and M2-to-GDP seems to be higher than 240%? What can we say of the enormous debts of the LGFVs (Local Government Financing Vehicles) that are hiding trillions of debts (measures in USD), which, in connection to the SOE’s debts (State Owned Enterprises) make Chinese debt also unsustainable?

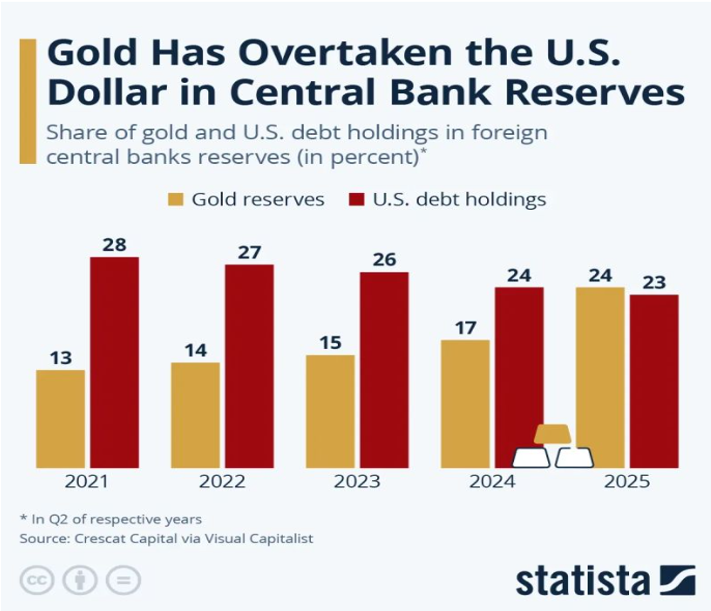

Is the global monetary system based on fiat currencies sustainable? If it is, why then do central banks’ reserves keep increasing their gold positions while reducing their Treasury holdings? Why such a significant shift (see table below) in just a short four-year period?

2021: Gold 13%, U.S. debt 28%

2023: Gold 15%, U.S. debt 26%

2025: Gold 24%, U.S. debt 23%

Could those shifts reflect a prolegomenon to a rebalancing of the global financial architecture, which, in turn, may be accompanied by fiat currency instability? When we ponder the latter in combination with the debt concerns, should we start hedging now?

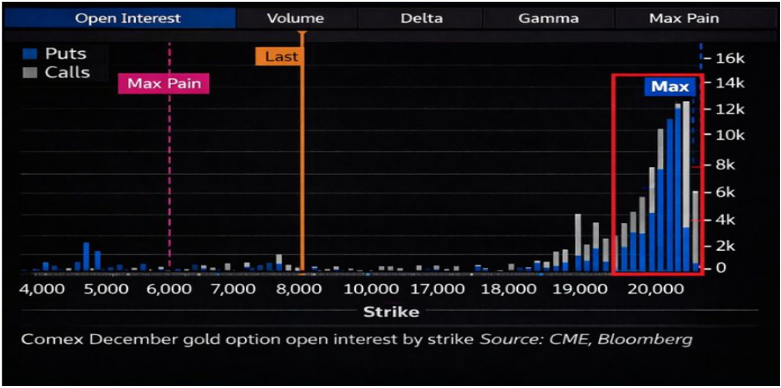

And then, what does the following graph imply in terms of gold trajectory? Why do we see so many December options on gold at prices that represent a three-fold increase? Do those options point to a hedge against a potential overhaul of the monetary system?

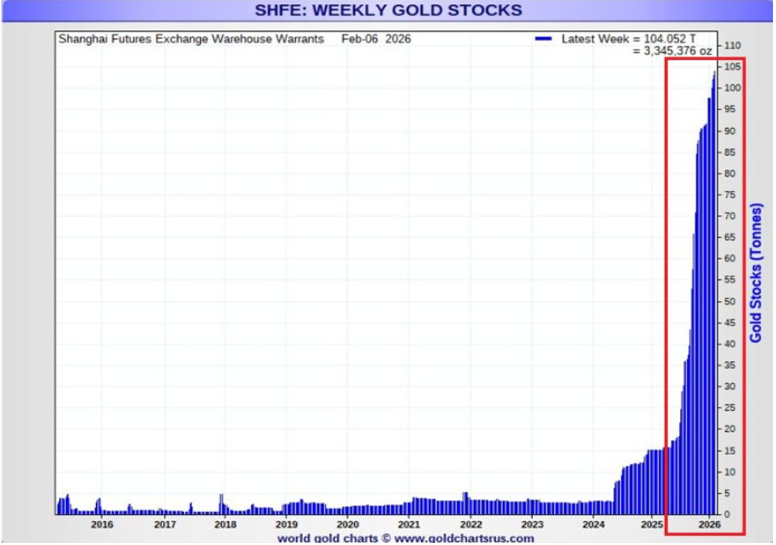

And why has China been accumulating deliverable gold through warrants, as shown below? What does such quadrupling tell us about hedging?

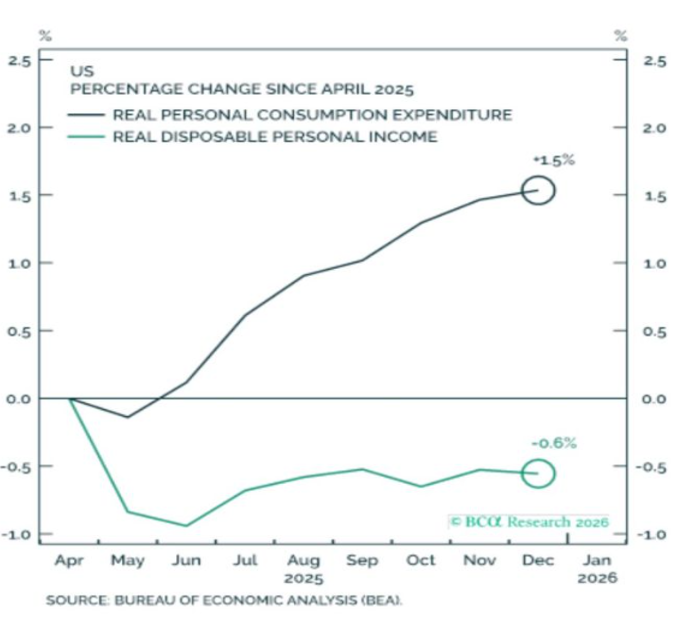

As we are pondering about rising budget and trade deficits and the slowing down of the GDP growth rate (as reported late last week), what can we say of the following graph, as reported by BCA Research? Shouldn’t something have to give in?

The questions above point to the superposition reality where price discovery (whether for stocks, bonds, precious metals, industrial and rare earths, etc.), may have already entered into a quantum phase where multiple potential states not only exist but possibly are exacerbated, bringing forth a sealed box that may or may not contain a hypothetical subject which may be alive or dead, true or false, happening and not happening, simultaneously, a.k.a, Schrödinger’s Cat.

Let’s close with some reflections on the happening/not happening attack on Iran. Who could suffer the most from that attack? Could Chinese oil imports be affected even more after the Venezuela hit? Could Japan also be affected? What would the effects be on interest rates? Could the bond market experience a shock if the Japanese are forced to sell Treasuries at a time when the refinancing of Treasuries at higher rates creates a number of headaches?

“When Savonarola started undermining my position in Florence, I started planting the seeds of having two Popes out of the Medici family,” Lorenzo Medici pronounced, offering the thought more as a strategic hedge than a certainty, only to hear Luther stating, “indulgences won’t get you to heaven.”

That extraordinary 40‑year interval between Renaissance and Reformation has much to teach us, so it is a conversation we will return to very soon.