It has been an eventful year, at least thus far. It started with the Venezuelan bang, and continues with significant volatility in equities (especially tech-related), precious metals, and bitcoin. Speaking of the latter, it has lost 50% of its value since last October and close to 30% since the beginning of this year. However, that should be expected from anything that has no intrinsic value behind it (needless to say that we cannot buy the arguments for a safe haven against inflation, fiat currencies, or geopolitical upheaval).

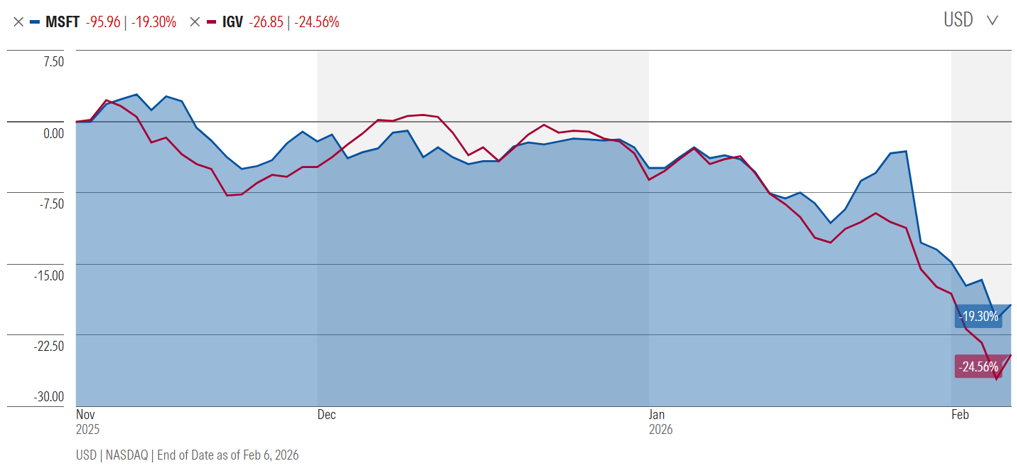

Are we in a phase where a reset in risk appetite is taking place? The turmoil in the tech sector focuses on software companies, but not only. Software companies experienced significant declines as the fear that AI tools will make their mission obsolete starts spreading in investment circles. Let’s see, for example, the price movement of a software-related ETF in comparison with Microsoft’s stock price in the last three months.

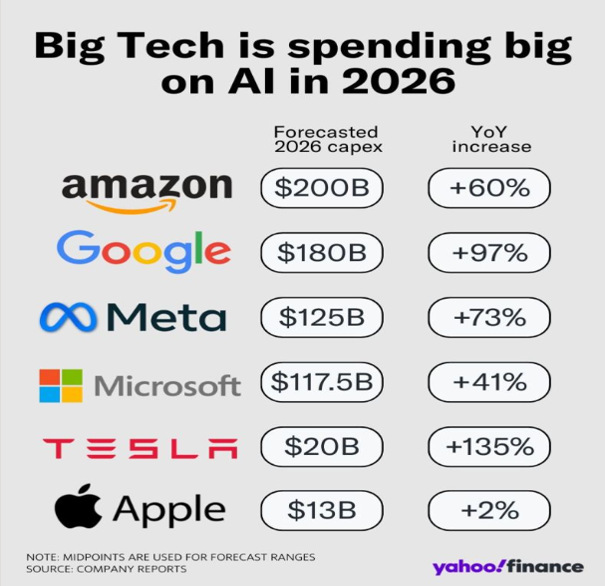

As we can clearly see, the software-related ETF has lost almost one quarter of its value in the last three months, and Microsoft has lost almost 20% of its value. It seems that the tech sector in general, and especially some names in the Magnificent Seven, are left behind in the general market trajectory. The reasons for this could range from valuation concerns to a movement towards cheaper non-US alternatives, and from questions related to profitability to concerns about whether the future profits will justify current rising expenditures. Speaking of the latter, the graph below is indicative of those concerns.

The unanswered question at this stage is whether we are experiencing a shift in the tech sector away from expensive stocks towards those with cheaper valuations (e.g. European or Chinese ones), and whether that shift also entails a movement away from the hyperscalers (Amazon, Meta, etc.) to those who benefit from the unquestionable productivity gains due to AI.

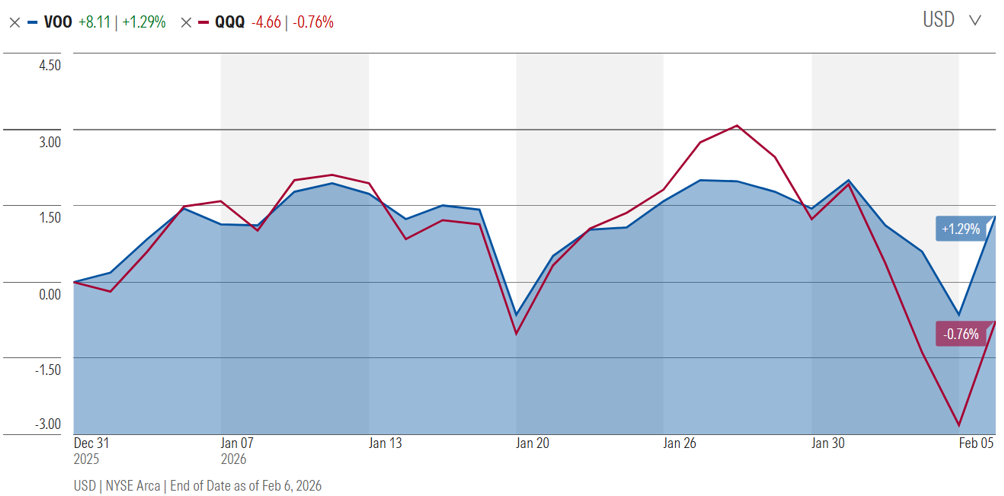

The tech turmoil may partially ricochet in the overall market conditions, especially when we take into account weak employment data (significant layoffs have been announced and slowing job growth was reported). As the graph below shows, the S&P 500 (VOO) has experienced some gains so far this year, but with significant volatility. The top tech companies (QQQ), however, have dropped a little bit so far in 2026.

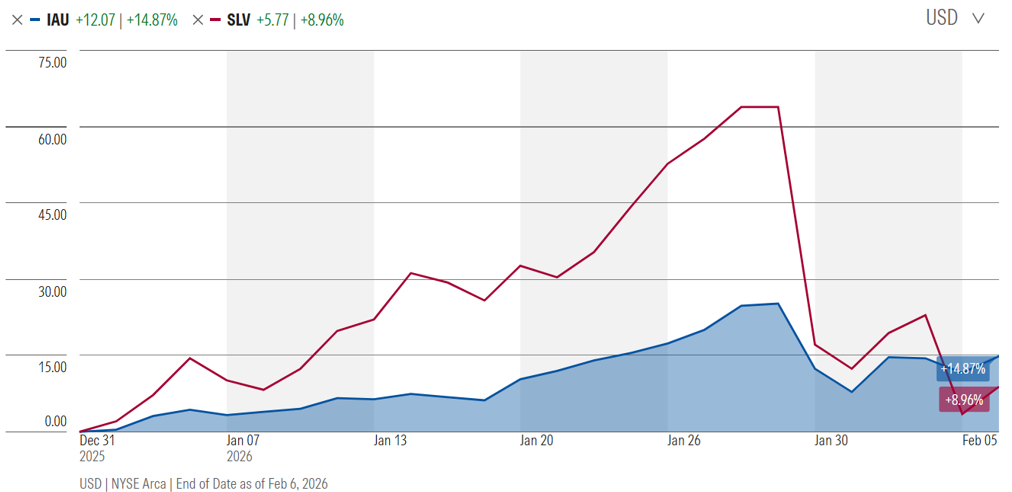

It is time now to shift our discussion to precious metals, whose volatility has been significantly higher this year relative to the market and the tech sector. As the graph below shows, gold prices gained almost 25% between January 1st and January 29th, while silver gained close to 64% over the same period. Since then, both have declined, and so far this year, they are up almost 15 and 9 percent, respectively. Certainly, such gains are very good for a period of five weeks.

Here are our thoughts on the volatility observed in precious metals:

First, the exponential rise for both was not justified. Such movements could be justified under war conditions or situations where an economic or financial crisis is imminent. Therefore, the downturn brought some normalcy in the upward trajectory of precious metals.

Second, both gold and silver experienced extraordinary gains in 2025 (64% and 144%, respectively). The extraordinary gains in the first month of 2026 on top of the gains in 2025 initiated some profit taking.

Third, there has been a reciprocal mechanism between spot and futures prices. In the futures market, significant leverage has been used. The trading margin requirements keep rising in the last couple of months. The requirement to post higher and higher collateral discourages buying and has also been forcing sales, which push prices down. We have seen the story before: every time that the margin requirements are raised, precious metal prices are pushed down.

Fourth, there has been an alleged manipulation in the market for precious metals, and especially for silver. There are several public records where well-known entities have paid fines in the hundreds of millions of dollars related to precious metal trades. If an entity has shorted, for example, a stock or silver, it will make money only if that security drops in price. If on the other hand that security’s price keeps rising, then the losses accumulate and become significant. It is natural for that entity to wish for a drop in the price to cover its short positions.

Fifth, the demand and supply fundamentals for silver favored a rising price. Demand for industrial and data centers’ use is on an upward trajectory, supply is facing major constraints (with China limiting it in a significant manner), and physical deliveries are confronted with delays. Consequently, prices from a fundamentals perspective point to an upward trajectory.

In conclusion:

- Mispricing and overvaluation concerns may continue nudging volatility.

- Questions related to rising expenditures of the big tech, along with expected profitability, may continue bringing volatility.

- Geopolitical fears could expand, which naturally would demand from investors restraint, caution, and the seeking out of safe havens.

- Internal political conflicts and boneheaded policies usually backfire for consumers and investors.

- Value-oriented stocks may continue performing better in the future (as they have been doing in the last few months).

- Foreign equities may also continue performing better than US equities, as they did in 2025.

- The Fed transition to new leadership may be tested, which means more volatility.

I recently visited Rimini in Italy. The only reason I wanted to visit was the fact that this is the place where Julius Caesar crossed the Rubicon, declaring war on his own country, ignoring the laws and the Roman institutions, and marking the abolition of the Roman Republic while starting the age of empires.