On September 2nd, 1870, Otto von Bismarck met Napoleon III outside Sedan. The French had lost the decisive battle of Sedan and surrendered. A few weeks later, the Germans advanced, laying siege to Paris. On January 18th, 1871, in Versailles (of all places), the new German Empire (at the objections of Bismarck) would impose severe financial penalties on France, and later that year, under the Treaty of Frankfort, the Germans forced a humiliating agreement on France, which included the ceding of territories. The French had to wait until 1919 and repay the Germans in Versailles with the same currency.

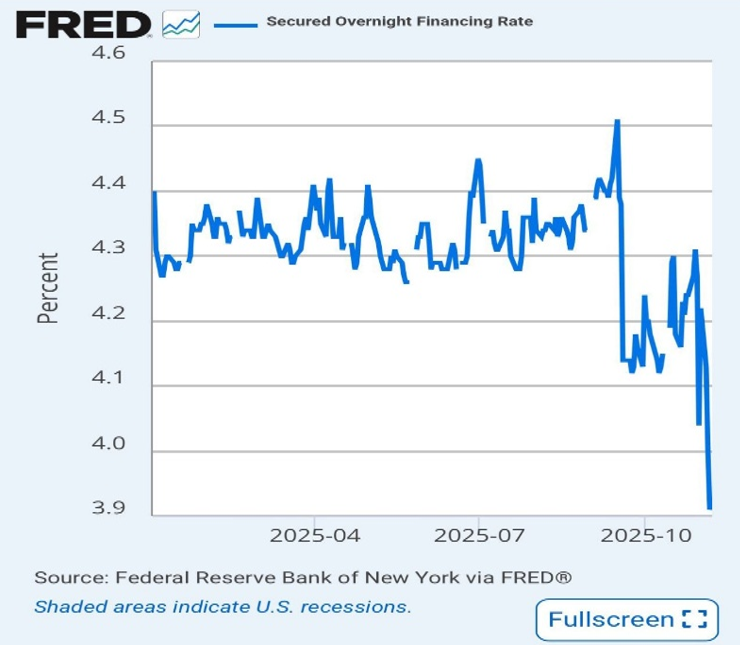

When looking at the SOFR rate (which replaced the LIBOR and controls $397 trillion in global derivative contracts), we get the impression that it, too, surrendered to some unseen forces.

What have we observed in the markets over the course of the last two weeks?

- Growing uneasiness regarding AI spending and developments (see also here)

- Signs of the labor market softening and rising layoffs

- Good profit margins and earnings reports, which, however, are mostly attributed to momentum related to AI

- The breadth of the market (advancing vs. declining stocks) continues to be narrow

- The S&P 500 has never been so expensive (numerous benchmarks and indicators such as Price-to-Sale, Price-to-Earnings, Price-to-Book, etc., are exceeding dot-com era multiples)

- Supreme Court ongoing tariff hearings (chances are that the Trump administration would have to improvise to retain the tariff regime), which could unsettle the markets if hundreds of billions of taxes collected from US businesses would have to be refunded

- Rising concerns over private credit

- The Buffett indicator (market cap to GDP ratio) is at an all-time high, marking two standard deviations above its average (something that only happened in 1970, 2000, and 2021)

- Repo market concerns related to tightening liquidity, and corresponding rising Fed loans using the emergency cash window

- US manufacturing sector continues to be in recession

- Asian tech shares have plunged recently

- Warnings from S.E.C. commissioner that the agency’s policies are “a reckless game of regulatory Jenga”

- Reports from reputable institutions which project that for several years in the future, large stocks may experience negative real returns

Otto von Bismarck had a single focus: To unite Germany under Prussian control. He pushed a cousin of King William I (1797-1888) to seek the Spanish throne. To the French, that was unacceptable, and thus he faced only two options: Either persuade Berlin to retract the candidacy or declare war on Prussia. They knew that the chances of the first option were zero, so on July 15th, 1870, France declared war on Germany. That war of 1870-71 is somehow forgotten, yet the defeat of the French under humiliating conditions became the fertilizer of the Great War that erupted in August 1914. So, while France was branded as the aggressor, the fact is that through the infamous Ems Dispatch, Bismarck manipulated the Prussian reply to France’s request for a withdrawal of the candidacy in a way certain to provoke the proud French into fury.

The dramatic decline of the SOFR matters because it represents the benchmark rate for derivatives, corporate loans, adjustable credit facilities, i.e., securities which are worth fifteen times the global GDP (after all, the main culprit of the 2008 financial crisis were those derivative contracts). So, while we can put on the optimist hat and adopt the belief that such a drop will facilitate growth and earnings, the concern is multifold: The drop may be the outcome of a serious underlying problem, such as market overconcentration, it might reflect credit risks of counterparties, or an effort to postpone reckoning, or even an attempt to prolog a bubble. In all cases, a serious risk may be at work and rising. The drop reminds us of the humiliating German penalties on the French, which Bismarck disapproved of, knowing what eventually would happen.

Bismarck was certain that his strategy would entice the French into a war that they would lose, given the multiple fronts that the French were fighting, the superior weapons that the Germans had, as well as the sheer numbers of the respective armies. Furthermore, Bismarck’s strategy encircled the French forces (markets today are encircled by leverage and hooked to an overvaluation diet), knowing well that a win would redefine the geopolitical order, something that he needed to push for his reunification goal of an Empire, which ultimately would challenge the English.

Similarly, the market nowadays is encircled by a handful of firms. Bismarck used modern tech (rail and telegraph), and today’s tech leaders not only control tech advancements but systematically control the adoption of tech developments. The French predicament reflects today’s trajectory, where market participants have limited choices given the power of the tech mega corps. Bismarck’s communication strategy and maneuvering is like today’s market momentum, which might ignore balance sheets and cash flow statements. Given the above, the French predicament may be like the current market’s trajectory. Sooner or later, the AI frenzy and the market momentum will cease. Will the portfolios be caught on the Bismarck or on the Napoleon III side in the forthcoming battle of modern Sedan?

Portfolios today do not face a frontal assault. They are rather encircled by mega corps that reshape the economic terrain by creating and controlling ecosystems that have become inescapable for other market participants. The real threat might resemble that of the German victory at the battle of Sedan: Are today’s tech and market developments sowing the seeds of a major disruption that will change the order of doing business?

Amid rising risks (and the central bank’s efforts to avoid a hard landing by injecting more liquidity into the markets), could it be prudent to buy out-of-money hedges such as Puts on over-valued indexes and/or buying out-of-money Calls on precious metals?