Some have described Thomas Mann’s book Mario and the Magician as one of the finest novels written in the 20th century (for a brief summary of the book, see the end of the commentary). Most certainly, when it was written in 1929, it was a pivotal moment in world history, and Thomas Mann has been credited with the foresight of seeing through the native German dark clouds when he drafted the novel. Could the book’s message have any relevance to contemporary developments?

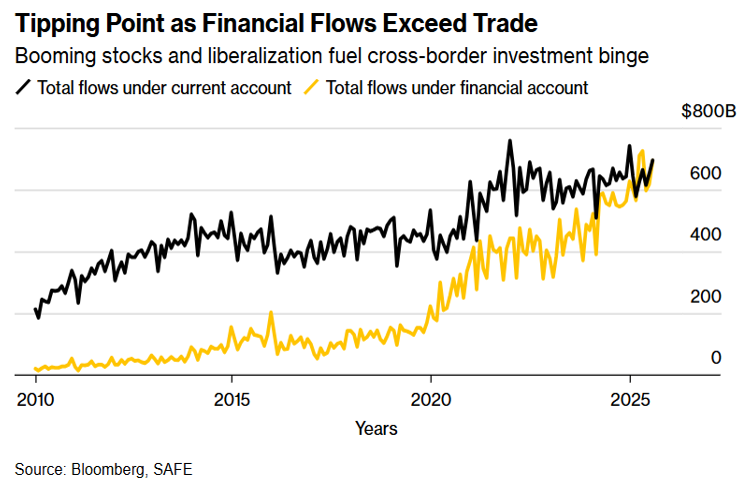

Pivotal moments in history are usually understood with hindsight vision, unless foresight through trends is evaluated within its historical context, in a similar manner to Thomas Mann’s novel. So, when we look at the following graph, we naturally wonder if we are on the verge of such a pivot.

The phrase “China shock” for decades meant the impact on employment in the US and Europe of Chinese imports, following the accession of China to the WTO. The extended version is the monetary aspect of that shock in a globalized economy, which, as Chairman Volcker used to say, was marked by “non-system, system”, following the collapse of Bretton Woods in the early 1970s. The massive Chinese exports resulted in immense trade surpluses/accumulation of foreign reserves, which China started circulating around the world. The consequences of the recycling of such reserves have been both geopolitical (see the impact of the Belt and Road Initiative) and geoeconomic, where the recycling of surpluses into US Treasuries (along with the spending profligacy of the executive and legislative branches of the government) led to the US economy’s addiction to a debt/spending mentality.

For decades (well before the starting point of the graph above), the value of Chinese goods traded far exceeded the flow of funds pouring into China. That appears to be changing now. The consequences of that reversal would be historic and world-changing, as China pursues de-dollarization via six distinct strategies, namely: Reduced holdings of US securities; accumulation of gold as an alternative to dollar reserves; lending to other countries in renminbi; executing trade agreements in renminbi; pursuing a sphere of geopolitical influence opposing to US interests and pursuits in conjunction with its useful idiots; and a systematic conquest of cutting-edge technologies. The last, sixth strategy has been labeled as “China Shock 2.0”.

For a good chunk of the first part of the 21st century, the Chinese used to lead in 3-4 technologies vs. the 60 technologies the US led in. The latest reports show that China now leads the US in well over 65% of critical technologies. Can the US really fight such a historical pivot using tariffs or by assembling iPhones when the factories will be ready in 3-5 years? And what will happen to the US dollar when China decides to intensify those six strategies described above (especially its mission to become the global science and technology powerhouse) and ends up opening and liberalizing its financial markets?

But going back to the effects of China Shock 1.0, we cannot ignore the fact that if we add together the manufacturing prowess of the US, Japan, Germany, and South Korea, the sum would be below Chinese manufacturing power. Chinese exports account for 36% of global exports, and when we consider the competitive advantage China is building in technologies, then a consideration should be made regarding the geopolitics of trade and how the latter will affect Chinese influence in Asian, African, and Latin American markets, let alone European ones. Thus, despite the disorderly competition of Chinese firms, along with huge amounts of internal debts, as well as the large numbers of unprofitable enterprises which have been propped up by local administrators, a pivot seems to be underway within China, where local governments are ceasing the support to doomed companies while taking measures to boost domestic demand.

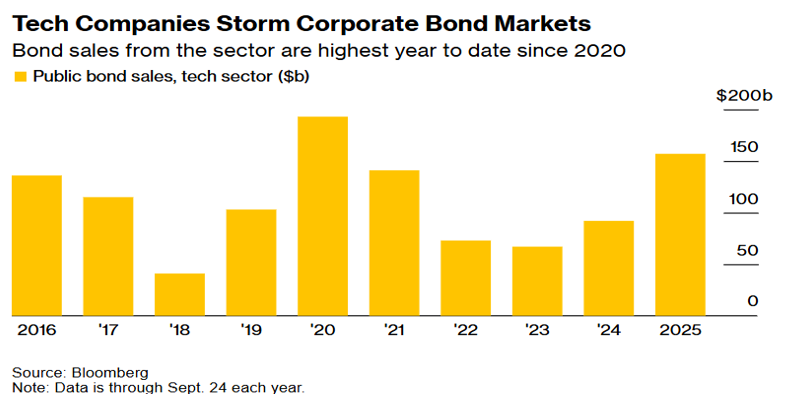

Against the above background, we are assessing the market’s prospects under conditions of massive corporate bond issuance related to the euphoria around AI. The graph below tells us of such hunger/hype to overspend on AI ambitions by tech firms, which in turn, find willing investors to finance undertakings whose ultimate payoff remains questionable.

Hence, the equity euphoria now hits the debt markets, which seem to send the message “there is no room for error”. Consequently, spreads between Treasuries and investment-grade bonds are disappearing and everything seems to be priced at perfection, despite the MIT findings that 95% of companies’ AI pilots didn’t produce a positive return on their investment, and a recent warning that “AI firms’ revenue is likely to fall around $800 billion short of what’s needed to fund the computing power to meet projected demand by 2030.”

Also, against the evolving geopolitical and geoeconomic environment described above, one has to wonder if, in the landscape of plentiful liquidity, a bubble-like “money merry-go-round” phenomenon is at work that inflates involved companies’ valuations. Let’s consider the following facts:

- OpenAI reportedly signed a $300 billion cloud contract with Oracle to secure cloud computing services for its AI models and data centers.

- Oracle spends tens of billions of dollars to buy NVIDIA’s GPUs and meet the demand from clients like OpenAI.

- NVIDIA turns and invests $100 billion into OpenAI, and the cash is disbursed as gigawatts of the new data centers coming online.

In Mann’s novel, a German family is vacationing at a hotel where a charming individual by the name Mario works. Mario is loved by all the guests for his good humor, humility, and great service. Just before the vacation ends, the family attends a performance by a famous magician. The magician, who goes by the name Cavaliere Cipolla, is apparently a fraud. He performs even the simplest tricks badly, and yet he holds his audience with a strange power that they cannot resist. The family wants to leave the performance, but strangely enough, something seems to be holding them in their chairs. Just before the end of the performance, Mario is called on stage to assist the magician. However, the magician’s intent is nothing but to humiliate Mario by forcing him to act in a loathsome way. Upon awaking from the trance, Mario obtains his revenge, but it gives neither him nor those who like and respect him for his cheerfulness and decency any satisfaction. There is no remedy in that environment. There is only hope that the performance will end at some point.

Are we active participants in an era when it is hard to distinguish between reality and illusion, partly because perceptions become realities, and what is real has become less real, while the creators of illusions have become so adept? We still believe in assets that represent no one else’s liabilities.