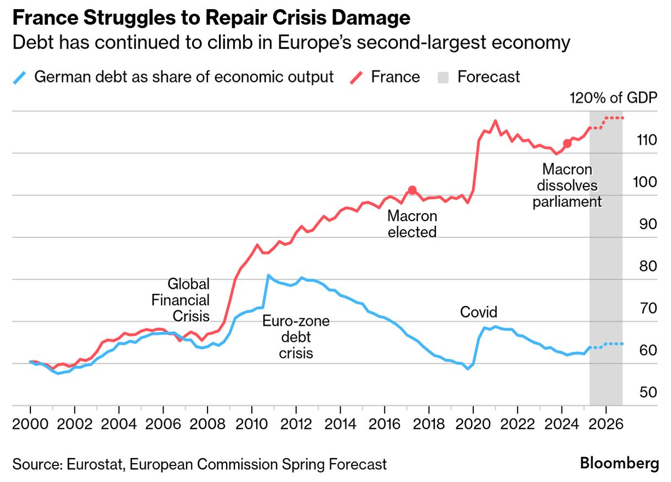

The political crisis in France (which started with President Macron’s snap election last year following his party’s humiliating defeat during European Parliamentary elections) culminated last evening in the ousting of the Prime Minister (the fourth in two years). Mr. Francois Bayrou’s tenure as PM was just nine months, and his ousting followed the rejection of the previous PM’s government (Michel Barnier), whose tenure was less than four months. At the center of the political crisis was the effort to reduce the deficit and place France into a more sustainable debt trajectory. The figure below is indicative of France’s uniquely diverging path relative to the other major sick economy in Europe (that of Germany).

Of course, such outcome is the symptom and not the cause of an EU-wide (and not only) political crisis whose origins are threefold: The shrinking middle class that sees everywhere dead ends in pursuit of a better life; the lack of leadership; and the bankruptcy of systems (chief among them – besides the political – the educational system) that pursue fulfillment through dialectic materialism (where people’s relationship to the means of production is the chief “virtue”/determinant of values, priorities, beliefs, and priorities).

As implied above, we treat the French political crisis as indicative of a global political crisis. Last week, the Deputy PM of the United Kingdom resigned (let’s not forget that in the last 10 years, the UK has changed seven PMs), and a government reshuffling took place in Britain. Over the weekend, the PM of Japan submitted his resignation too, facing the lost confidence of his lawmakers and deputies. And in Argentina, the appeal of “chainsaw” Milei is fading as he lost big in local elections over the weekend. In other Asian countries (besides Japan), we saw early this morning the PM of Nepal resigning, while a few weeks ago, Thailand’s PM was forced out of office, and in Indonesia, a major turmoil is brewing. Of course, all these developments (including the brewing turmoil in the US) will have significant market consequences. The bond and equity markets will be impacted, along with currency and commodity markets.

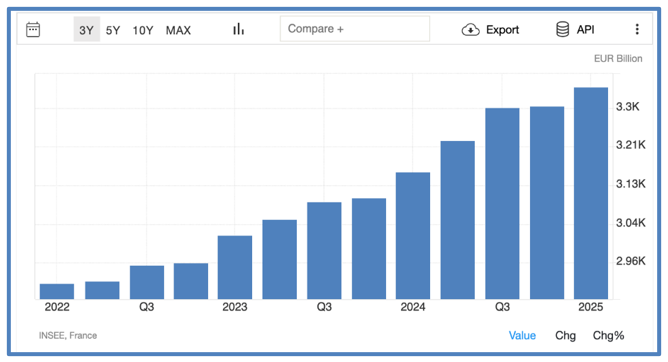

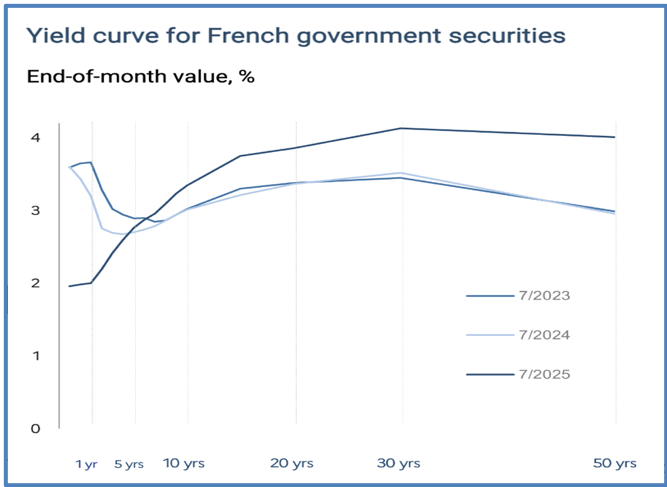

France has the largest fiscal deficit in the EU, and the costs of servicing its debt undermine its ability to uphold the social contract that it traditionally has with the public. The pursuit of a sustainable path (budget cuts, pension reforms, tax legislation, viable priorities within a visionary plan for the next 15-20 years, etc.) faces a fragmented political system marked by parties whose political goals include extreme positions. The prognosis? Unsustainable illusions and the recycling of crises and systems. The graph above and the two below portray the French standing, but they are also indicative of the EU-wide (and probably global) forming crisis that destabilizes economies, cancels social contracts, postpones fulfillment of promises, terminates the dreams of the younger generations, impairs retirements, subverts civility and political cohesion, disrupts progress, undermines families, weakens social mobility, sabotages the middle class, ruins development, and wrecks leaderships.

The rising yields of long-term French bonds partially reflect the concerns of an unsustainable path undermined by fiscal profligacy/accumulation of deficits, betrayal of the middle class, the tensions of political stalemate, and the rising of extreme voices (we could certainly say almost the same for a number of major countries around the world, and as readers would recall, we have raised the red flag regarding US debt and fiscal profligacy on numerous occasions).

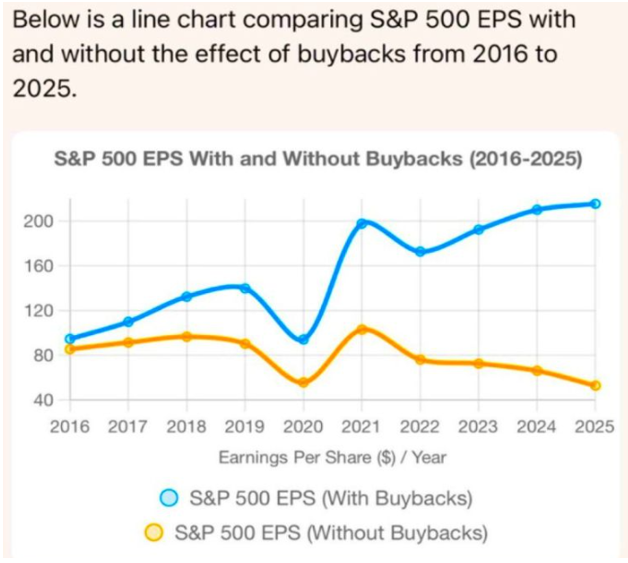

So, while we recognize some of the arguments/merits of bullish calls regarding US equities (which see the S&P 500 reaching 7000 by year’s end), it cannot escape our attention that the arguments used to justify the market’s value are presented as arguments based on earnings’ fundamentals. However, we cannot ignore the fact that other fundamentals are pointing to an overvalued market that is led by momentum, overconcentration, higher multiples, and liquidity. To that, we should also add that, as is shown below and reported by Charles-Henry Monchau, without buybacks, we would be facing a different market. Buybacks artificially enhance earnings, giving the illusion of rising earnings while fundamentals may be simply flat (similarly to the job market that has ceased creating new jobs).in equal estimation?”

In times like these, investors should seek solid anchors, and while we recognize that there are some very strong companies (US and elsewhere) that could play that role, our focus for decades now has been on the anchor role that precious metals play during times of turbulence and when crises are emerging.

Here are some arguments that precious metals should have a prominent place in investors’ portfolios:

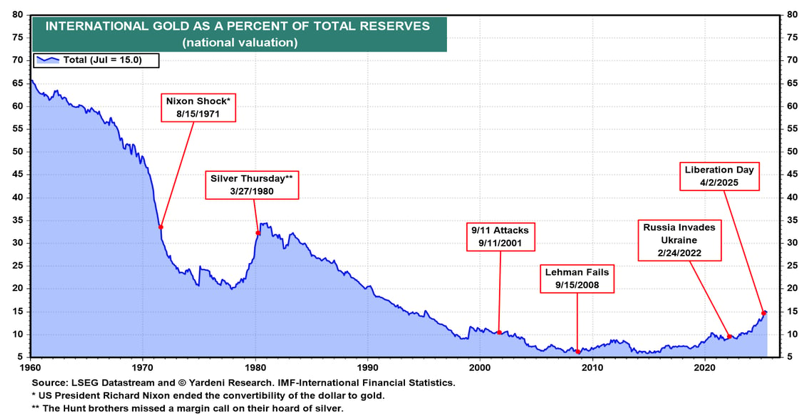

- Central banks around the world are adding gold to their holdings and diversifying their reserves from pure fiat currency and bonds (which are still other parties’ liabilities) to gold. As shown below, in the last three years, that percentage jumped from 9 to 15%. If that trend continues, and especially if the mid-1980s target-point is adopted (25% of central banks’ reserves), then we could see a major increase in precious metal prices.

- If just 1% of the money invested in bonds and stocks migrates to precious metals (gold and silver), we wouldn’t be surprised if by mid-2026 those precious metals gain an additional 25%.

- Geopolitical crises are expected to increase and expand and, consequently, the need for a haven will continue rising.

- Attacks on central banks’ independence undermine their credibility and strengthen the argument for assets that are not determined by governments’ dictates.

- International investors (especially in Asia) who question the economic policies and/or the valuation of equity markets, could seek safety in precious metals, boosting demand and thus precious metals’ prices.

- The low correlation between precious metals and other asset classes enhances the argument for adding more precious metals in portfolios (at this junction, we believe they should represent at least 8-10% of a portfolio).

- If the Fed starts its easing cycle again on September 17th by lowering short-term rates, then precious metals’ appeal will become even brighter, especially if a few weeks and months from now inflationary pressures are revitalized.

One of the best thinkers the world has ever seen was Origen of Alexandria, Egypt (born around 185 AD). Eusebius called him Adamantius (Man of Steel). Origen’s concept of a universal restoration may represent the best hope that the world can envision during turmoil and crises. However, such restoration presupposes the renewal of the mind. Can we hope for that?