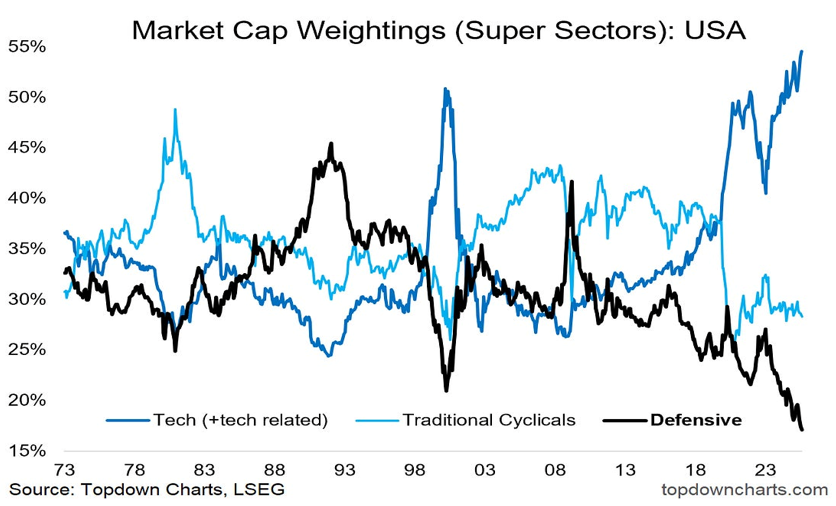

When we look at different market sectors (even if we were novice market participants), it cannot escape us that the tech-related sector (which includes communication-related stocks) has supercharged above and beyond the dot-com era valuations, while defensive (utilities, consumer staples, healthcare) as well as more traditional cyclical sectors (energy, financials, industrials) have declined in the past 50+ years (in terms of market cap weighting), as the following figure shows.

The period of interregnum is defined as the era between two regimes. The late 1990s served as an interregnum period (fueled by tech speculation), setting the stage for the 2007-’09 collapse. As the figure above shows, the cyclical sector retained its relative weight between 1973 (the collapse of Bretton Woods and the starting point of major geopolitical and geoeconomic events) and today, with normal deviations from its mean value during times of economic upswing or downturn. The defensive sector, on the other hand, retained its mean weight between 1973 and 2020 (with normal deviations during times of downturns or upswings). However, the tech sector has supercharged forward at an astonishing pace in the last twenty years, fueled by sentiment, exuberance, liquidity, and unrealistic expectations/valuations.

It’s interesting to note that the collapse of the late 1990s tech bubble coincided with a new geopolitical order, while the new supercharged tech era that started in mid/late 2010s is also marked by the rise of rogue regimes which are set to challenge the US global position, especially if a market shock is to take place in the next two-three years, given the accumulated challenges that the US economy faces, starting with its debt position.

The market recovery from its lows on April 9th of this year has been accompanied by a rise in sentiment, expectations, good earnings, stable employment, and modest price pressures despite the volatile economic policies. Euphoric markets can be observed from the S&P 500 that reached a new all-time high this month, to bitcoin highs, as well as the resurgence of meme stocks. Euphoria and the speculative spirit (in the sense of lottery ticket mentality) are moving together, and historically speaking, can lead to bubbles, which always burst. Such an assessment can be supported by looking into fundamental measures such as price-to-sales ratio, price-to-cash flow, price-to-book, and price-to-dividends, which are all near record levels.

Several tech and especially AI-related securities are priced not only to perfection, but they are also priced as if there will be no competition, especially from China, which obviously dominates the EV sector (with BYD), the renewable energy sector (JinkoSolar, JA Solar, LONGiGreen Energy), the battery sector (CATL, BYD), the drones sector (with its DJI company), and the fast-rising houses of Huawei (telecom), DeepSeek (AI), and SMIC and YMTC (semiconductors).

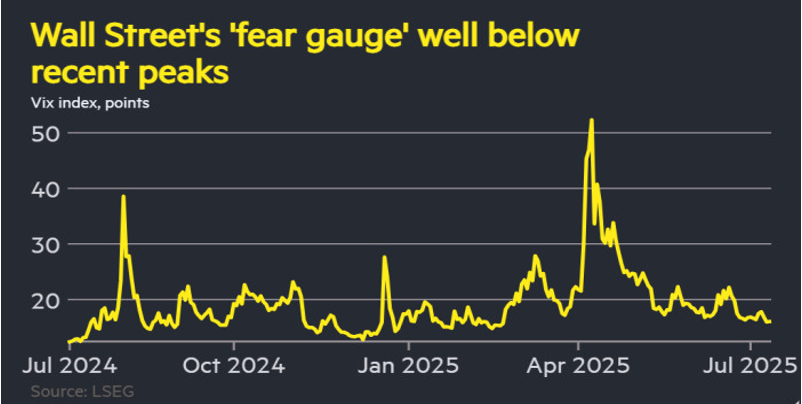

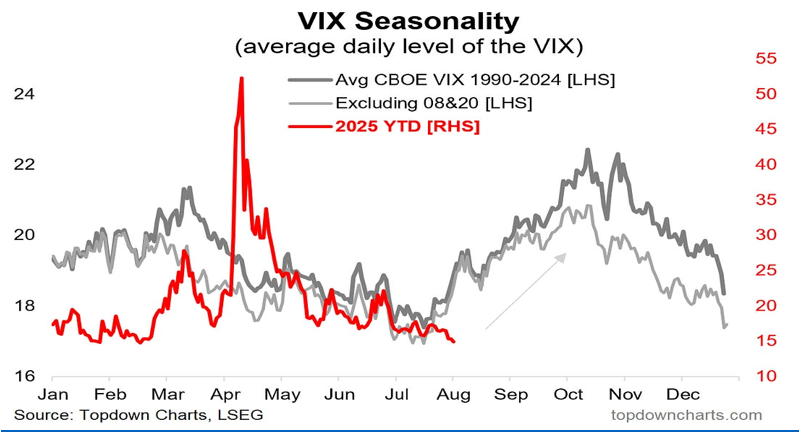

The current receding of market volatility (as shown in the graph below), when it is viewed in relation to the historic August-October period (as shown in the second graph below), calls for caution as it could reflect dangerous acquiescence at a time when the margin of safety appears to be very thin.

What is perceived as resilience of the economy (in spite of labor supply pressures due to immigration policy changes, record high tariffs for at least the last 40 years, dramatic government downsizing with record-breaking budget deficit and debt, a significant decline in the dollar, and the undermining of Fed’s independence), could be hiding significant vulnerabilities, and turn out to be a façade as liquidity is still plentiful and wealth effects may be hiding undercurrent trends that are being ignored.

So, in that environment the fear of missing out on a market upswing fuels speculation, despite the fact that there are market warnings about inflation picking up speed in late 2025 and early 2026 and consumer spending slowing down along with corporate earnings by early 2026, the combination of which could undermine such resilience, especially under conditions of market pressures and possible correction.

By 2027, approximately 45% of the OECD countries’ debt needs to be refinanced. That debt stands now at about $60 trillion. Refinancing will be taking place at higher rates (most of that debt was issued at very low rates), which will raise the governments’ costs and the respective deficits at a time of geopolitical inflection and potentially during times of market corrections with the threat of recession over market participants’ heads. If the route chosen at that time is the tightening of belts and austerity, we may be facing the shock that AI, by that time, will be incorporated in the managers’ portfolios. Last time, the central banks stepped in and bought the excess bonds issued due to the financial crisis. Will private digital currencies step in at that time, or will we observe the bursting of their bubbles? The arithmetic of bond markets in lieu of rising Japanese yields has changed the game at a time when supply will be rising and demand will be falling.

Are we facing a cycle when momentum could be replaced by oxidation before interregnum rests among us, inaugurating a new era that is too soon to speculate what it will entail?