The Wooden Nickel is a collection of roughly a handful of recent topics that have caught our attention. Here you’ll find current,open-ended thoughts. We wish to use this piece as a way to think out loud in public rather than formal proclamations or projections.

1. Nothing Like Price to Change Sentiment…or Theses

For much of the last ten to fifteen years in the stock market, we have seen the financial press drown us in the idea that one of the main reasons for the concentrated dominance of equity returns in a handful of names (from the FAANG to now the MAG7) is due to their capital light nature. Buffett himself remarked way back in 2017 that many of these companies represented the ideal business because “You really don’t need any money to run these companies.” They possessed unique characteristics that belied economic convention; they could grow their profits with very little incremental investment at exceptional rates of return while warding off competitive threats. Traditional/antiquated methods of financial analysis obfuscated value as the rise of intangibles necessitated an evolution in how to understand value.

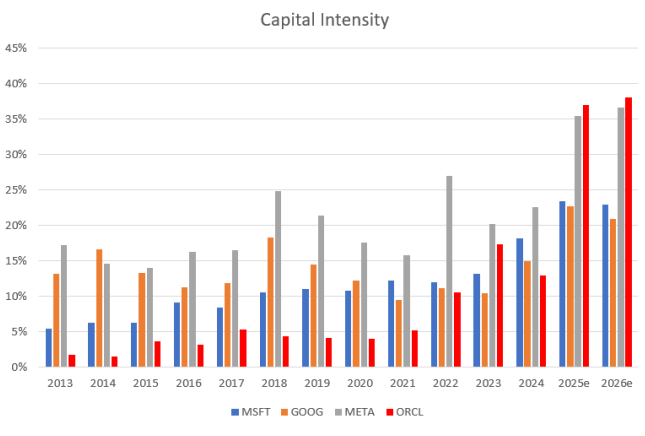

Today, with the potential of AI marking a new technological and computing paradigm (allegedly), we find ourselves in a vastly different financial and market environment (Figure 1).

Figure 1: AI’s Capital Intensity

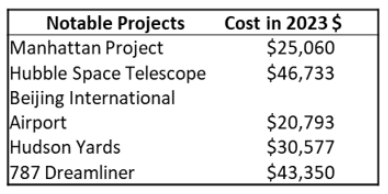

There has been plenty of chatter as to the astronomical amounts being spent by those chasing “artificial” dreams, rightly so. While Figure 1 shows the shifting business model, we must remember these percentages are based on much larger revenue bases than what many of these companies were generating a decade ago. Google, on its own, will spend about $75B in capital expenditures this year, worth about 3 Manhattan Projects adjusted for inflation.

But while most of these names cited above have been some of the most beloved by the markets over the last decade, plus for their (lack of) capital intensity it seems the love continues to pour on them despite the fact that no one can say with a straight face that there is a capital light business model at play. To be sure, both of these business models can work; they are not mutually exclusive. If the incremental returns following these additional expenditures are healthy, then the financials of these respective companies should be ok (equity returns given starting multiples are another matter entirely)

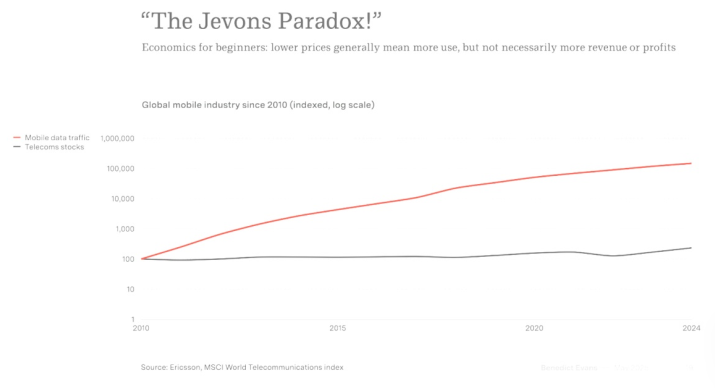

.But all this brings to mind another Buffett quote: “The best business is a royalty on the growth of others, requiring little capital itself.” Not only are investors betting that a new platform shift will accelerate profits for these giant companies going forward, but they’re bucking against the last major platform shift from the dot-com bubble. Back then, it was not the spenders who were the winners of disruption. AT&T, Verizon, and a host of other telecom and cable operators were spending north of 20% of their sales on capital expenditures (and with much more leverage) only to see the royalties accrue to firms that did not even exist yet (Meta, Google, etc.) or were afterthoughts at the time (Apple). The rise of the internet did come indeed but not returns for the spenders of capital (Figure 2).

Figure 2: More Use Doesn’t Mean More Profits, Source: Benedict Evans

2. The Best Doesn’t Always Matter (or Win)

“When should we have known about Nvidia?”

If you would have come to me as someone from the future in 2021 and pointed to the calendar and said that by the fall of 2022 Artificial Intelligence would the topic du jour in markets and the economy, catalyzing hundreds of billions of dollars in investments and asked me what company would stand to benefit the most, there are a lot of people who could have told you Nvidia. But I think this does the company a disservice as merely the residual in a massive, rising tide and dilutes the 10-15 years of investment, enabling new forms of computation that preceded the ChatGPT era.

But more important than the investments, the technological assets, and the intellectual property nurtured over such a timeline, the answer to the opening question is probably in the mid-2000s. Granted, most of us haven’t been paying attention that long, and back then, Nvidia was essentially known as a gaming company with some diversifying lines into high-end workstations for the sciences.

Nvidia’s roots were indeed as a graphics company, believing that gaming would grow into a huge market and necessitated specific, purpose-built hardware. Its first product, the NV1, hoped to blow competing graphics chips out of the water with farhigher resolution, faster speeds, and better-quality output. Delivering the required novel techniques for handling, processing, and displaying textures, while every other hardware maker used triangles as the default means of rendering polygons, Nvidia would use quadrilaterals. The technique would save on the computer’s use of costly memory. The savings could be deployed elsewhere for superior graphics. The fact that the entire ecosystem of publishers and content creators for the market they hoped to serve would have to rewrite everything just to get their games to work on an Nvidia card was a secondary thought; after all, the best should win, right?

The only problem was that between starting the design process for the NV1 and the actual shipment of the card memory, prices collapsed by 90% from $50 per megabyte to $5, which meant competitors could simply deploy more memory on their chips and save their customers hundreds of hours of development time and cost. The technically superior advantage got rapidly diminished. Instead of recovering development costs, the flop of the company’s first product put the company into a dash for cash.

Fast forward twelve years, and Nvidia is on top of the graphics market and pushing into other end markets like high-end scientific computing, physics simulation, and hoping to crack into data centers. To spark adoption, Nvidia spent close to $500M dollars over the course of three years developing CUDA, its proprietary software platform for programming its chips (for reference, designing a new chip in 2020 cost roughly $500M and here Nvidia was spending the same amount 15 years earlier for a program in secret development; this isn’t Apple just spending more for a chip to go into its already proven phones). Why did it cost so much? Per company executives, “You can’t just throw technology over the wall and expect people to adopt it. You can’t simply say, ‘Here’s our new GPU, go crazy.’”

Both episodes are told in detail in The Nvidia Way, Tae Kim’s history of the company. The second episode stands in direct contrast to the first. They had learned everything they could after almost going belly up a decade earlier and had internalized it into the company’s culture and way of operating. That’s when one could have reasonably understood that there was something different about the company, something about the way that it operated that set it apart from competitors. The assets, the IP, more innovation would come that put it in a position to capitalize the greatest tech arms race in history but if it wasn’t for the engrained ethos twenty years ago, I think we’d be in a much more competitive landscape.

The contrast between the two episodes is a clear reminder that the best doesn’t always matter. And it doesn’t always win. And those lessons apply doubly in technology with its fast innovation cycles and large profit pools attracting competitors.

And also, don’t put great leaders and inventors in a box. It’s just as important to know the jockey as it is the horse you are betting on.

3. Aim Small, Miss Small

There’s a classic video shown every year to millions of business school students in their introductory marketing class of Malcolm Gladwell discussing Prego and the perfect spaghetti sauce. The lecture traveled through the evolution of consumer goods marketing over the latter part of the 20th century and touched on several important marketing truisms. One of its more profound takeaways was that the perfect consumer good did not exist, and the “right” product was not a discrete entity. Rather, pleasing consumers existed at the juxtaposition of variability and specificity. Market segmentation existed on a spectrum.

Being as we are in the golden age of content, it is easier than ever for professional and enterprising investors alike to find, consume, and reflect on a broad wealth of investment related content: from podcasts, to Substack, to social media engagement, to investment fund letters, to academic lectures, and more, it is easier than ever to find quality analysis and methods for selecting investments, constructing portfolios, and building wealth (it’s also easier than ever to find junk, but I digress).

Some people opt for the classic cigar-butt style investing of Ben Graham; others advocate for quality compounders a la Phil Fisher. Some like to hold hundreds of positions, like Peter Lynch. Others prefer a concentrated style like Buffett, especially in his early years. Some like to screen for companies with founders at the helm, others for firms with high insider ownership. Some like to look for singles and doubles and make quick returns over several months, while others hope to slug one over the fence for years. The list of ways to do this is endless, and the permutations even more interminable.

Amateur marksmen are taught early on when keying in on their target to “aim small, miss small” (the phrase was popularized in the 2000 film The Patriot). The phrase emphasizes focus and clarity of thought while eschewing the arrogance of perfection; aim for the bullseye, and if you miss (which is likely) you will still hit the target. Zoom out, and aim for the periphery, and you are likely to miss the target altogether.

When it comes to the practice of investing it is important not to “confuse stillness with inaction.” Nor should we confuse the exhaustive list and ways in which to find superior returns as a tool of exclusion. Rather, we study how the best do it, not to find something that checks every box on the list but just to know what the boxes are. The purpose of reading investors like Buffett, Munger, Lynch, Marks, etc. is not to try and synthesize them all into one. That would be like trying to take perfectly fresh ceviche, a decadent pasta, and rich tiramisu and putting them all in a blender, thinking they go together. The purpose of studying great investors and great businesses is not to be in pursuit of the perfect business nor the perfect investment. The reason behind it is just to have a greater toolset and confidence in getting good returns rather than a microscopic chance at the astronomical. Zoom in on the small so you can fish in the biggest pond

4. Recommended Reads and Listens

Benedict Evans’ 2025 Presentation

How Huawei Became Nvidia’s Biggest Threat

More on Repealing the Laws of Economics

Moats, Money, and Management’s Mettle