Welcome to our monthly newsletter, Carbon Market News Roundup, the goal of which is to introduce our audience to a new asset class market in the making: the carbon market. Our previous issues, along with the rest of our commentaries, may be read here.

EU ETS Updates

EU countries demand stricter controls on new CO2 price

Kate Abnett, Reuters

Dutch abolish CO2 levy to create ‘level playing field’ with EU

Quantum Commodity Intelligence

Several European Union member states have recently called for changes to carbon pricing. In late June, 16 countries, including Germany and Poland, asked Brussels to strengthen the safeguard in the upcoming transport-and-heating fuels carbon market (ETS2) that would automatically release extra permits if prices spike. These governments want more aggressive triggers to add allowances and avoid sudden price surges that could affect consumers. At the same time, the European Commission is under pressure to contain energy costs. A draft EU plan announced on June 24 would let eligible heavy industries receive temporary electricity price relief for up to three years, as part of a new state-aid regime. This relief, capped at 50% of power costs and contingent on green investments, aims to keep industry competitive while advancing the green transition.

Industry groups have warned that high carbon and energy prices threaten competitiveness. For example, Eurometaux (a metals industry group) petitioned EU leaders to ease rules, arguing that European factories face higher costs than U.S. or Chinese rivals. The draft state-aid rules explicitly acknowledge this concern, noting that “until the decarbonization of the Union’s electricity system fully translates into lower electricity prices, industries … will continue to face higher costs compared to competitors in jurisdictions with less ambitious climate policies.” Policymakers are trying to navigate this by providing targeted support without diluting the overall emissions cap.

Some countries are also adjusting national carbon policies to align with EU systems. In the Netherlands, for example, parliament voted in late June to scrap a national CO2 levy on industry that was layered on top of the EU ETS. Lawmakers noted the measure was creating competitive distortions, so removing it will put Dutch industry on the same footing as EU peers. This move reflects a tension in compliance markets: while emissions targets tighten, countries must ensure their firms are not unduly disadvantaged. The Netherlands’ decision has been framed as creating a “level playing field” within Europe.

Looking ahead, EU emissions trading and related policies remain the linchpin of Europe’s climate strategy. The latest reports show emissions in the power sector are declining (helped by renewables and nuclear) but gains in transport or industry are slower.

Source: EuroNews

Regulators in Brussels have agreed to use some revenues from the new transport/heating carbon market to cushion energy bills, while negotiations continue over broader targets (e.g. the 2040 climate goal). In sum, compliance markets are under stress from macro factors (geopolitics, energy prices) even as regulators seek to ensure that markets remain robust and fair.

A U.S. CBAM?

Harvard Says U.S. CBAM Could Deliver $200 Billion – and a Cleaner Future

Saptakee S – Carbon Credits

Trade in the Age of Climate Change: The Role of a U.S. Carbon Border Adjustment Mechanism

Hadley Brown, EESI

Lisa Zelljadt, Veyt

As global climate policy advances, the U.S. is facing growing pressure to adopt tools that protect its domestic industries while encouraging lower emissions abroad. One such tool, the Carbon Border Adjustment Mechanism (CBAM), is already being rolled out in the European Union. A U.S. version is now under active discussion, with bipartisan proposals emerging in Congress and strong backing from leading think tanks and industry players. But what would a U.S. CBAM look like in practice? Is it politically feasible? And how might it affect domestic competitiveness and global trade?

Already, US producers are among the cleanest in key sectors, such as steel and aluminum.

Source: Climate Leadership Council

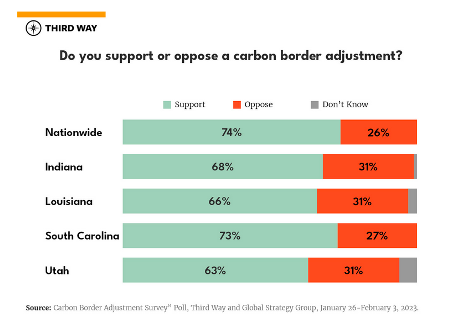

Additionally, support for a CBAM cuts across party lines, especially when framed as protecting U.S. manufacturing jobs from unfair foreign competition. Polling by Third Way shows that once informed, nearly 75% of U.S. voters back a carbon import fee, with strong support even in fossil fuel-heavy states.

Source: Third Way

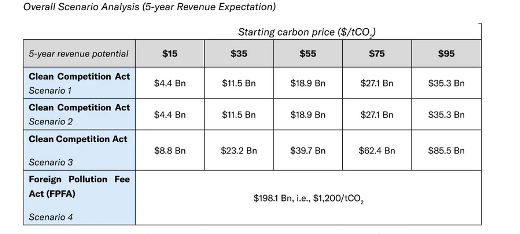

Republican Senators Bill Cassidy (R-LA) and Lindsey Graham (R-SC) have introduced the Foreign Pollution Fee Act, which would impose a tariff based on how much CO2 the exporter has emitted. Yet, political disagreements remain over the inclusion of a domestic carbon price, which Democrats favor but Republicans oppose. Critics warn that a CBAM without a domestic carbon price could be seen as protectionism, especially by emerging economic, and thus be challenged in the WTO.

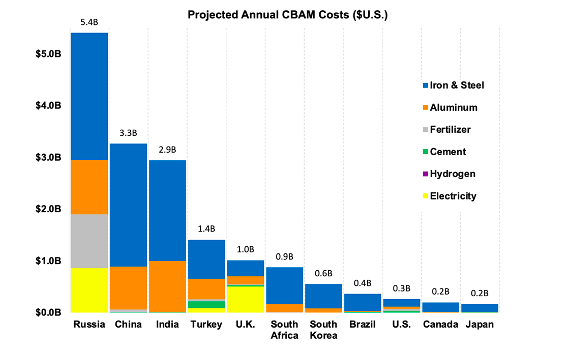

Moreover, the fiscal potential is enormous. A new study by Harvard Business School estimates that a U.S. CBAM could generate $200 billion in new revenue over a decade.

Source: Harvard Report: The Revenue Potential and Country Exposure of a U.S. Border Carbon Adjustment

The study emphasizes how a carbon import fee – set at $55 per ton – would impact emissions-heavy sectors like cement, steel, and aluminum. Importantly, it argues that such a policy could accelerate global decarbonization by rewarding cleaner supply chains, while the revenue could fund domestic green investments or reduce fiscal deficits. The report also highlights that without a CBAM, the U.S. risks becoming a dumping ground for carbon-intensive goods, undermining domestic climate progress.

Maritime Shipping and Alternative Fuel Developments

Tighter carbon rules, slower economy to erode bunker demand growth, IEA says

Enes Tunagur, Reuters

HPCL to Invest $231 Million in Push to Scale Compressed Biogas in India

Energy, Oil, & Gas Magazine

Brazil Raises Biofuel Levels, Sees Gasoline Self-Sufficiency

World Energy

The International Maritime Organization (IMO) and regional regulators are tightening carbon policies, which in turn affects shipping fuel demand. A mid-June report by the International Energy Agency forecast that global bunker-fuel demand will plateau due to stricter regulations and sluggish economic growth. The IEA projects bunker demand around 5 million barrels per day through 2050, a far slower rise than earlier expectations. These changes come even as oil prices have eased, cushioning the near-term cost of marine fuel. However, going forward, ships will face new costs: the IMO recently agreed to introduce a carbon-pricing mechanism for international shipping, making shipowners pay penalties for above-target emissions from 2028.

Member states of the UN shipping agency approved a global fund and levy system to push the sector toward net-zero by 2050 . Under this deal, carriers will cover 100% of their carbon costs, and a separate fund will finance green R&D, with initial fees starting in 2027 and full payments from 2028. While details are still being worked out, this marks the first global carbon price on any industry, and it will significantly raise shipping’s cost of operations. In parallel, the EU’s FuelEU Maritime regulation entered into force in early 2025, mandating increased use of renewable and low-carbon fuels for ships calling at EU ports. Together with IMO rules, these measures mean shipping companies must plan for a shift to biofuels, synthetic fuels, and other innovations in the next few years.

Concrete steps toward such fuels are happening in Asia. In India, state oil firm HPCL announced plans on June 20 to invest around ₹20 billion ($231 million) in compressed biogas projects over the next 2–3 years. HPCL’s goal is to build 24 biogas plants, converting agricultural and organic waste into biomethane. This renewable gas will be blended into cooking fuel and transport gas to reduce emissions. While aimed at road and cooking gas markets, such efforts could indirectly benefit shipping: cleaner fuel availability onshore can encourage shipping companies (especially coastal shipping and short sea operators) to use LNG/biogas blends. India’s push also underscores how major economies are diversifying their fuel mix: HPCL’s move is part of India’s broader strategy to reach 15% gas in its energy mix by 2030, up from ~6% today.

In Latin America, Brazil took steps that will affect fuel markets. On June 25, Brazil’s government raised mandatory biofuel blending targets for gasoline, ethanol and biodiesel. The mandate for ethanol in gasoline was increased (from 27% to 29% by the end of 2025), moving toward energy self-sufficiency. Biodiesel blending requirements were also raised. Although these changes target road transport, they signal increasing biofuel production capacity in Brazil (already a global biofuels leader). In the longer term, expanded biofuel supply could be tapped for marine uses. Shipowners are eyeing sustainable biofuels (like used cooking oil-based fuels) as a drop-in solution, and more available biofuels globally can ease the transition mandated by rules like FuelEU Maritime and the upcoming IMO standards.

Overall, shipping is in a state of adaptation. Tighter international rules (IMO pricing, EU fuel standards) mean carriers face rising compliance costs and must invest in cleaner technology. At the same time, governments and companies are building cleaner fuel supply chains (from biogas plants in India to higher ethanol blends in Brazil) that will help decarbonize transport broadly. We expect to see continued focus on maritime emissions at the next IMO meeting in October, and likely pilot projects using sustainable fuels in global fleets. With bunkering infrastructure slowly catching up and carbon costs on the horizon, ship operators are weighing investments in efficiency and alternative fuels to prepare for the new regime.

Recommended Reads

China’s carbon emissions may have peaked

Extreme Heat Waves Are Longer and Hitting the Tropics Hardest