Welcome to our monthly newsletter which covers key developments in major non-US markets. With this newsletter, we highlight corporate, debt, and monetary policy news in European, Asian, and Latin American markets. We end this piece with a spotlight on commodities.

European Markets

Corporate and Business News

- Rheinmetall and Anduril formalized a partnership to co-develop and manufacture autonomous aerial systems and advanced propulsion technologies as part of a wider European Union (EU) plan to strengthen its defense industry.

- France’s banking group BPCE has agreed to acquire Portugal’s Novo Banco in a deal valued at €6.4 billion (approximately $7.4 billion), marking one of the largest cross-border banking acquisitions in Europe in over a decade.

- The EU has proposed a full ban on Russian oil and gas imports by the end of 2027, aiming to boost energy security and reduce geopolitical dependence. The plan includes halting new contracts by 2026 and phasing out existing ones, with limited exceptions for landlocked countries.

- In April 2025, British exports to the United States dropped by a record 33%, falling from £6.1 billion in March to just £4.1 billion, the lowest level since February 2022. These measures significantly widened the UK’s trade deficit and contributed to a 0.3% contraction in GDP for April. While the UK has reached a preliminary agreement with the U.S. to lift some of these tariffs, the broader 10% tariff remains in place, continuing to pressure exporters.

- German exports and industrial output fell sharply in April 2025, ending a temporary surge caused by companies rushing shipments ahead of new U.S. tariffs. Exports to the U.S. dropped over 10%, contributing to a broader 1.7% decline in total exports and a 1.4% drop in industrial production.

- According to France’s national statistics agency INSEE, the French economy is projected to grow by 0.6% in 2025, down from 1.1% in 2024. This slowdown is attributed to weak manufacturing output, sluggish foreign trade, and limited consumer spending.

- In April 2025, UK house price growth halved to 3.5% year-on-year, down from 7.0% in March, according to the Office for National Statistics (ONS). This sharp slowdown coincided with the implementation of a new property transaction tax hike, which significantly cooled buyer activity and dampened market momentum.

Debt and Monetary Policy News

- The European Central Bank (ECB) cut interest rates on June 5th, lowering its three key rates by 25 basis points. This brought the deposit facility rate to 2.00%, the main refinancing operations rate to 2.15%, and the marginal lending facility rate to 2.40%, reflecting the ECB’s confidence that inflation is stabilizing near its 2% target.

- On June 19th, the Swiss National Bank (SNB) cut its key interest rate by 25 basis points to 0%, marking a return to a zero interest rate environment for the first time since 2022.

- The European Central Bank has warned eurozone banks to stay alert for a potential rise in bad loans, especially in sectors like small businesses, consumer credit, and commercial real estate. While current non-performing loan levels remain low, early signs of stress—such as rising arrears—suggest banks should prepare for worsening credit conditions amid economic and geopolitical uncertainty.

- The SNB denied allegations of currency manipulation after being placed on a U.S. Treasury watch list for potentially unfair trade and currency practices this month. The SNB emphasized that its foreign exchange interventions are solely aimed at maintaining price stability and not at gaining competitive trade advantages.

Asian Markets

Corporate and Business News

- Toyota Motor Corporation has proposed a ¥4.7 trillion (approx. $33 billion) buyout of Toyota Industries to strengthen group integration and reduce market pressure as it shifts toward a broader mobility strategy. The deal has sparked criticism from some investors over its pricing and governance implications, though it has strong backing from Toyota leadership and major Japanese banks.

- China’s outbound shipments of rare earths in May jumped 23% on the month to their highest in a year, though Beijing’s export curbs on some of the critical minerals halted some overseas sales, with shortages rippling through global manufacturing.

- China’s factory output growth hit a six-month low in May, while retail sales picked up steam, offering temporary relief for the world’s second-largest economy amid a fragile truce in its trade war with the United States.

- In May 2025, China’s soybean imports jumped nearly 129% from the previous month to 13.92 million metric tons, driven by improved customs clearance and increased demand from crushing plants. Meanwhile, imports of crude oil, coal, and iron ore all declined, reflecting shifting industrial activity and inventory adjustments.

- Japanese manufacturers grew less confident about business conditions in June and expressed caution about the outlook for the next three months, citing U.S. tariff uncertainties and weak Chinese demand.

- Demand for palm oil from India and China is expected to rise significantly in the coming months, driven by a recent 12% price correction that has made palm oil more competitive compared to alternatives like soybean and sunflower oilsChina’s car sales rise in May, but price wars cloud outlook.

Debt and Monetary Policy News

- The People’s Bank of China (PBOC) kept its benchmark lending rates unchanged, as widely expected. This decision follows a round of sweeping monetary easing in May, including rate cuts and lower deposit rates by major state banks, aimed at supporting the economy amid weak demand, deflationary pressures, and a fragile trade truce with the U.S.

- China is intensifying its push to promote the digital yuan (e-CNY) as part of a broader strategy to reshape the global monetary system into a multi-polar currency framework, reducing reliance on the U.S. dollar. At the Lujiazui Forum in Shanghai, PBOC Governor Pan Gongsheng emphasized that a diversified currency system—where several sovereign currencies coexist—would enhance global financial stability and reduce systemic risks tied to dollar dominance.

- The Bank of Japan (BoJ) kept interest rates steady and decided to slow the pace of reduction in its bond purchases from the next fiscal year, signalling its preference to move cautiously in normalising still-easy monetary policy. However, Japan’s core inflation hit a 2-year high, keeping rate-hike bets alive.

- Japan’s government has announced a rare mid-year revision to its bond issuance program, cutting sales of super-long Japanese government bonds (JGBs) by about 10% for the current fiscal year to ease market concerns over rising yields and weak auction demand.

Latin American Markets

Corporate and Business News

- China floods Brazil with cheap EVs, triggering backlash as Brazilian auto-industry officials and labor leaders worry that the vast influx of cars from BYD and other Chinese automakers will set back domestic auto production and hurt jobs.

- Brazil has declared itself free of the bird flu virus on commercial flocks after observing a 28-day period without any new commercial farm outbreaks.Brazil is the world’s largest poultry exporter, accounting for nearly 39% of global chicken trade. Mexico eased a ban on chicken shipments from Brazil, setting the restriction now only to products coming from the Brazilian state of Rio Grande do Sul, instead of a previous countrywide ban.

- Brazil’s JBS, the world’s largest meatpacker, made a high-profile return to the spotlight by listing on the New York Stock Exchange. This marks a major milestone for the Batista family and a significant move for Brazilian agribusiness on the global stage.

- Ecuador’s mining ministry announced on Monday the launch of a new registry of concessions for the first time in seven years in an effort to attract more mining projects to the South American country and curb illegal operations. The registry was shut down in 2018, and since then, no new mining licenses have been issued, stalling development despite Ecuador’s rich reserves of copper, gold, and silver.

- Mexico’s antitrust authority, Cofece, has closed its investigation into Google without imposing a fine, finding insufficient evidence that the company engaged in monopolistic practices in digital advertising. The case, which began in 2020, could have resulted in a fine of up to 8% of Google’s revenue in Mexico.

- Capitan Silver agreed to acquire seven mining concessions from Fresnillo for $4 million, significantly expanding its Cruz de Plata silver-gold project in Durango, Mexico. The deal boosts Capitan’s land holdings by 85% and extends its mineralized trend by 1.2 kilometers, signaling continued consolidation in Mexico’s mining industry.

Debt and Monetary Policy News

- The World Bank forecasted steady but modest growth for Latin America and the Caribbean at 2.3% in 2025, with risks from global trade tensions, commodity price softening, and policy uncertainty.

- In May 2025, Brazil’s monthly inflation rate slowed to 0.26%, down from 0.43% in April, and the annual inflation rate eased to 5.32%, marking a three-month low. Despite this improvement, inflation remains above the central bank’s upper target of 4.5% for the seventh consecutive month, driven by persistent price pressures in housing and utilities, even as food and transportation costs declined.

- Brazil’s central bank raised its benchmark Selic interest rate by 25 basis points to 15%, the highest level since 2006. This marked the seventh consecutive rate hike, driven by persistent inflation concerns, resilient economic activity, and unanchored inflation expectations.

- In May 2025, Argentina’s monthly inflation rate dropped to 1.5%, the lowest level in five years and a major milestone for President Javier Milei’s economic reform agenda. To further stabilize the economy and boost foreign reserves, Argentina also launched a $2 billion repurchase agreement with a consortium of seven international banks, including JPMorgan and the Bank of China.

- Mexico’s central bank, Banco de México (Banxico), continued its monetary easing cycle by cutting the benchmark interest rate by 50 basis points to 8.5%, marking the third consecutive half-point cut.

Commodities Spotlight

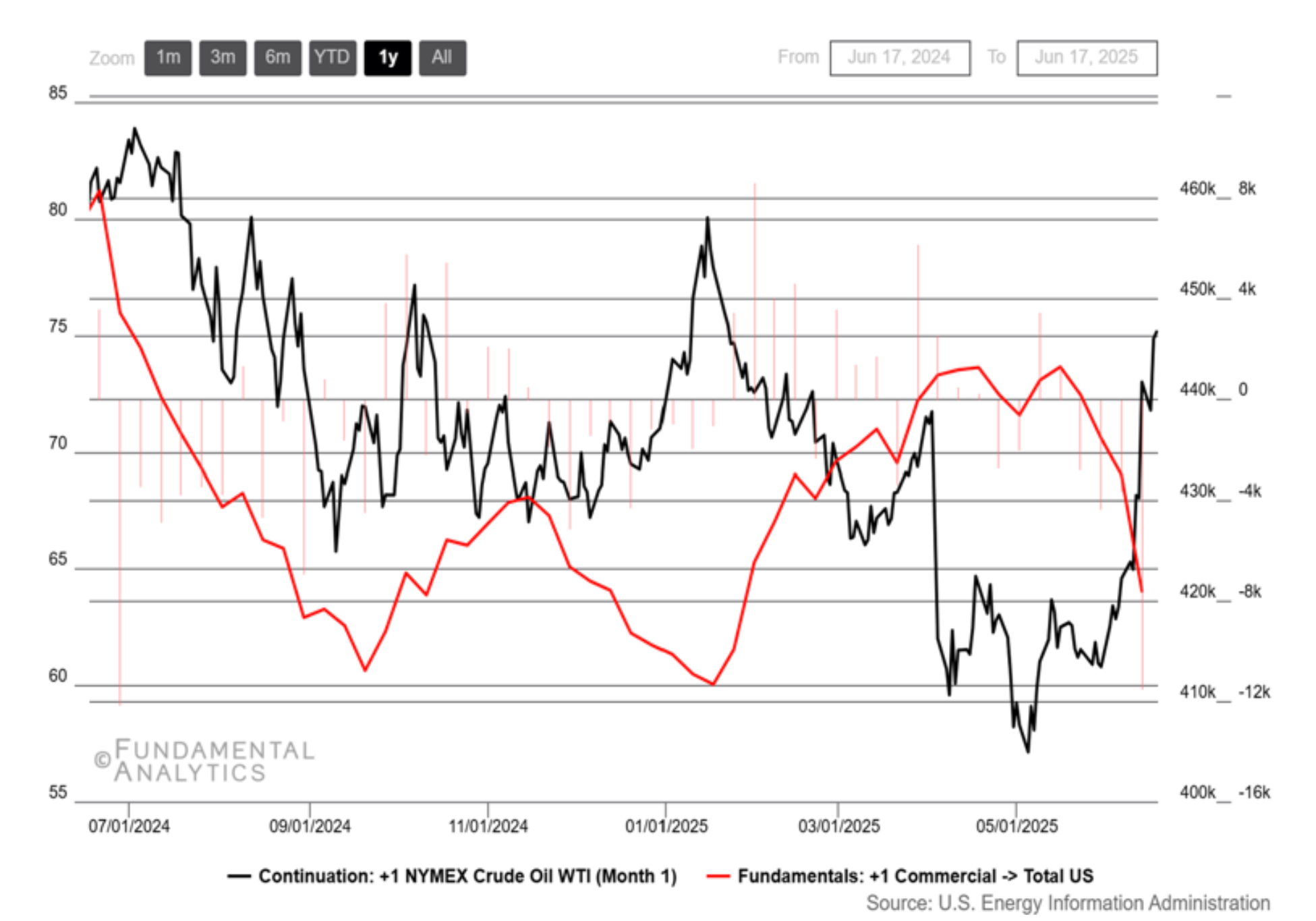

Crude Oil rises, as Israel-Iran hostilities continue

Source: Fundamental Analytics

WTI crude oil futures posted a third-consecutive weekly gain, as tension in the Middle East remains volatile, with Israeli Prime Minister Benjamin Netanyahu reportedly ordering intensified strikes on strategic and government sites in Iran. Despite the heightened tensions, Iran has continued crude exports, reportedly loading 2.2 million barrels per day this week. Meanwhile, oil prices found support from a sharper-than-expected drop in U.S. crude inventories, with government data earlier in the week showing the largest weekly drawdown in a year. This mix of geopolitical risk and tightening supply helped maintain overall bullish sentiment in the oil market.

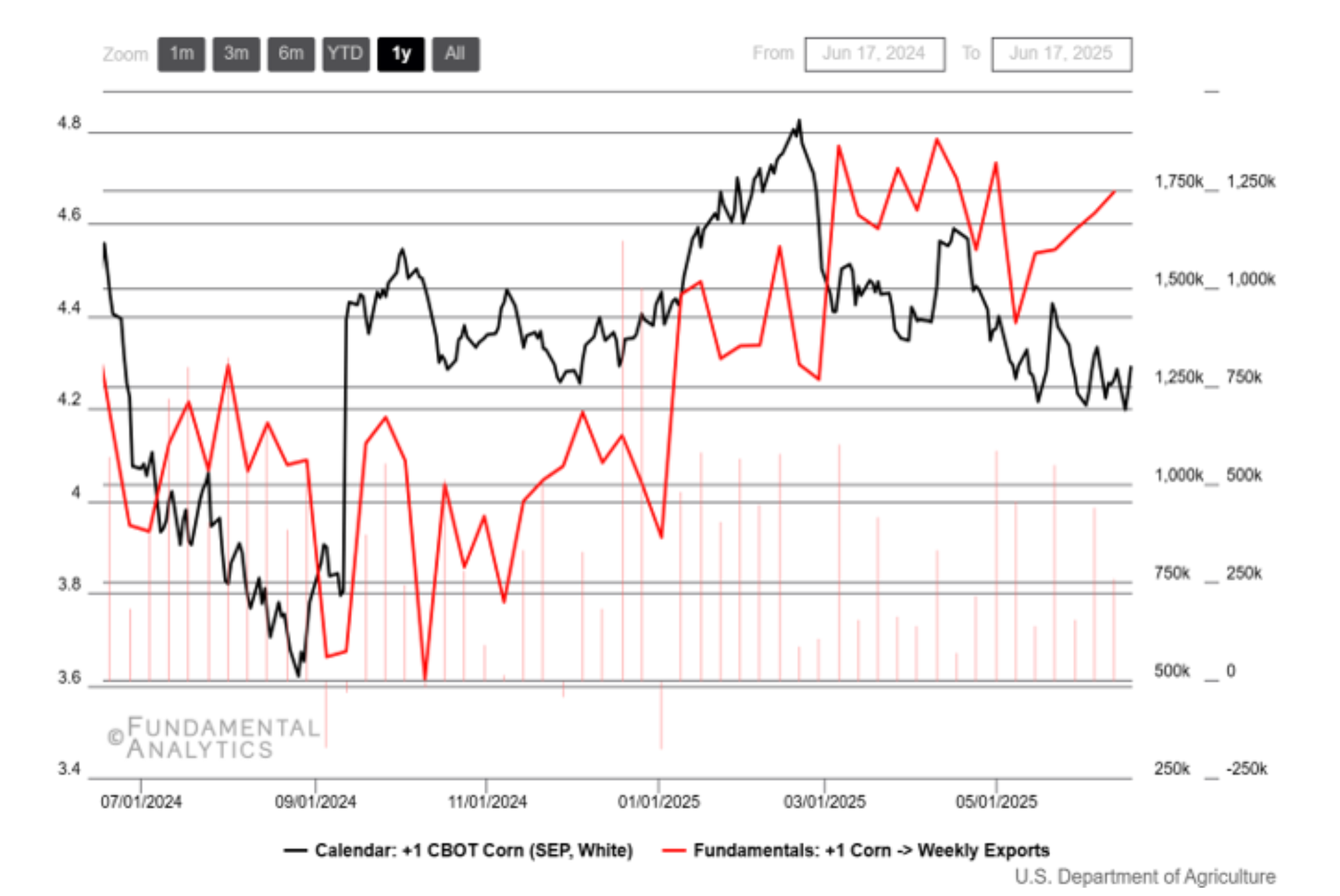

Corn futures tumble despite strengthened U.S. exports

Source: Fundamental Analytics

Corn futures slipped toward $4.30 per bushel, approaching the six-month low of $4.335 set on June 9th, as a glut of supply collides with seasonally subdued summer demand and forecasts for record harvests, while weekly export inspections have consistently exceeded forecasts, signaling strong overseas appetite. In the U.S., the USDA’s 2025–26 corn estimate of 15.82 billion bushels at 181 bu/acre, the largest on record, alongside renewed rains and warmer temperatures in the Eastern Corn Belt, has cemented expectations of a bumper yield.