Market Action

Global equities rose this week amid optimism over progress on US-China trade and on hopes that global growth may be stabilizing. The US 10-year Treasury note declined to 2.58% from 2.63% last week while the price of West Texas Intermediate crude oil rose $3 a barrel to $58.15. Volatility, as measured by the Chicago Board Options Exchange Volatility Index (VIX), fell to 13 from 17.8 last Friday.

The British Parliament undertook a series of votes this week to clear a path toward Brexit, which is scheduled to happen on 29 March, though how and when the United Kingdom’s withdrawal from the European Union will take place remains uncertain. Lawmakers rejected Prime Minister Theresa May’s proposed withdrawal agreement for a second time, though the margin of defeat was somewhat narrower this time. Parliament then voted against leaving the EU without a deal under any circumstances, at any time. Finally, a large majority voted to allow a short delay in the Brexit process, though any delay would require the unanimous approval of the 27 other members of the EU.

At the conclusion of the annual National People’s Congress, Premier Li Keqiang said that China has the capacity to reduce reserve requirements and interest rates in order to support economic growth. The country has been undertaking targeted forms of stimulus in recent months, but thus far has refrained from the large-scale stimulus efforts it has undertaken in the past as it attempts to rein in leverage. China’s industrial output grew 5.3% in the first two months of 2019, the slowest pace of expansion in 17 years. Investments picked up pace as the government fast-tracked more road and rail projects, while retail sales rose 8.2%. China generally combines January and February activity data in an attempt to smooth distortions created by the long Lunar New Year holidays.

US president Donald Trump acknowledged this week that China would likely prefer to conclude a trade agreement in advance of any meeting between Trump and China’s Xi Jinping in the wake of the failure to reach an agreement at the US-North Korea summit last month in Hanoi. China is said to be fearful that Trump could walk away from a deal if there are still unresolved issues when the leaders meet. The US president said he’s open to either finalizing a deal in advance of Xi’s visit or negotiating some final points in person with him. Chinese state media reported on Friday that the two countries have made concrete progress on the text of the agreement.

US consumer prices rose 1.5% in February compared with the same month a year ago, falling from January’s 1.6% pace. Core inflation, which excludes food and energy prices, fell to 2.1% from 2.2% the prior month. Additionally, the Federal Reserve Bank of New York’s Survey of Consumer Expectations reported a decline – from 3.0% in January to 2.8% in February – in inflation expectations held by the public for both the one- and three-year time horizons. Slowing growth and falling inflation are giving the Fed plenty of reason to remain on the monetary sidelines over the near term.

Eurozone industrial production rose a stronger-than-expected 1.4% month over month in January. Manufacturing activity tends to be more sensitive to the economic cycle than output from services. Those countries reporting improvements in activity include Spain, the Netherlands, Italy and France while Germany continued to display weakness (-0.8%). This week, the influential Ifo Institute lowered its 2019 German economic growth forecast to just 0.6% from 1.1% on weaker foreign demand for industrial goods.

Italy is considering borrowing from China’s Asian Infrastructure Investment Bank as part of plans to become the first G7 country to endorse Beijing’s controversial “Belt and Road Initiative.” An MoU will likely be signed on March 22. Until now, the majority of BRI infrastructure loans have come from the China Development Bank and the Export-Import Bank of China, but the AIIB lends according to international standards required inside the EU.

Click here for this week’s updated market returns table.

What could affect markets in the days ahead?

UK Prime Minister Theresa May is expected to seek a third parliamentary vote on the withdrawal agreement, perhaps on Tuesday, ahead of a European summit late in the week. The prime minister is said to be prepared to argue to euroskeptic legislators that if her deal is not approved, Brexit will face a protracted delay that would necessitate UK participation in upcoming elections for the European Parliament, a body the UK is trying to quit.

It’s been a rough old time for Europe’s economy, with momentum steadily waning last year even as the United States powered ahead. Growth warnings issued by the OECD and the European Central Bank have rattled investors further this year, as they try to assess what kind of toll the euro zone has suffered from trade wars, Brexit and Italian debt concerns. Whether this run continues or not will become evident in coming days. First up on Tuesday, comes Germany’s ZEW economic index. Purchasing manager indexes, a crucial forward-looking gauge, will be released on Friday from the United States, Euro zone and Japan.

The US Federal Reserve, meeting on Tuesday and Wednesday, is not poised to snatch away the proverbial punch bowl as unemployment is plumbing its lowest level in half a century and wages are ticking up. Labor shortages notwithstanding, the slowing economy is keeping prices in check, giving the central bank leeway to stand pat on interest rates after hiking four times in 2018. Compared to the Fed’s 2 percent inflation target, producer inflation was up 1.9 percent in the year to February, while consumer inflation rose just 1.5 percent to its smallest annual gain in 2-1/2 year. The next reading of the Fed’s preferred inflation measure, the core personal consumption expenditures price index, is due on March 29.

This Week from BlackSummit

Anti-Epics, Brexit, and Market Outcomes: A Mark of an Epic Misconception and Mismanagement

John E. Charalambakis

Listen on the go! Subscribe to the podcast Market Commentary with BlackSummit on iTunes, Android, Google Play, Stitcher, Spotify or TuneIn.

Recommended Reads

The High Costs of the New Cold War by Minxin Pei – Project Syndicate

Greece maps the long way back to a Brexit deal | Financial Times

China’s Slowdown Broadens, Despite Government Bid to Bolster Growth – WSJ

Gundlach Calls MMT `Complete Nonsense,’ Joining Naysayer Chorus – Bloomberg

A Rebuke for Populism? – The American Interest

Africa is attracting ever more interest from powers elsewhere – A sub-Saharan seduction

China’s Economic Slowdown, Explained

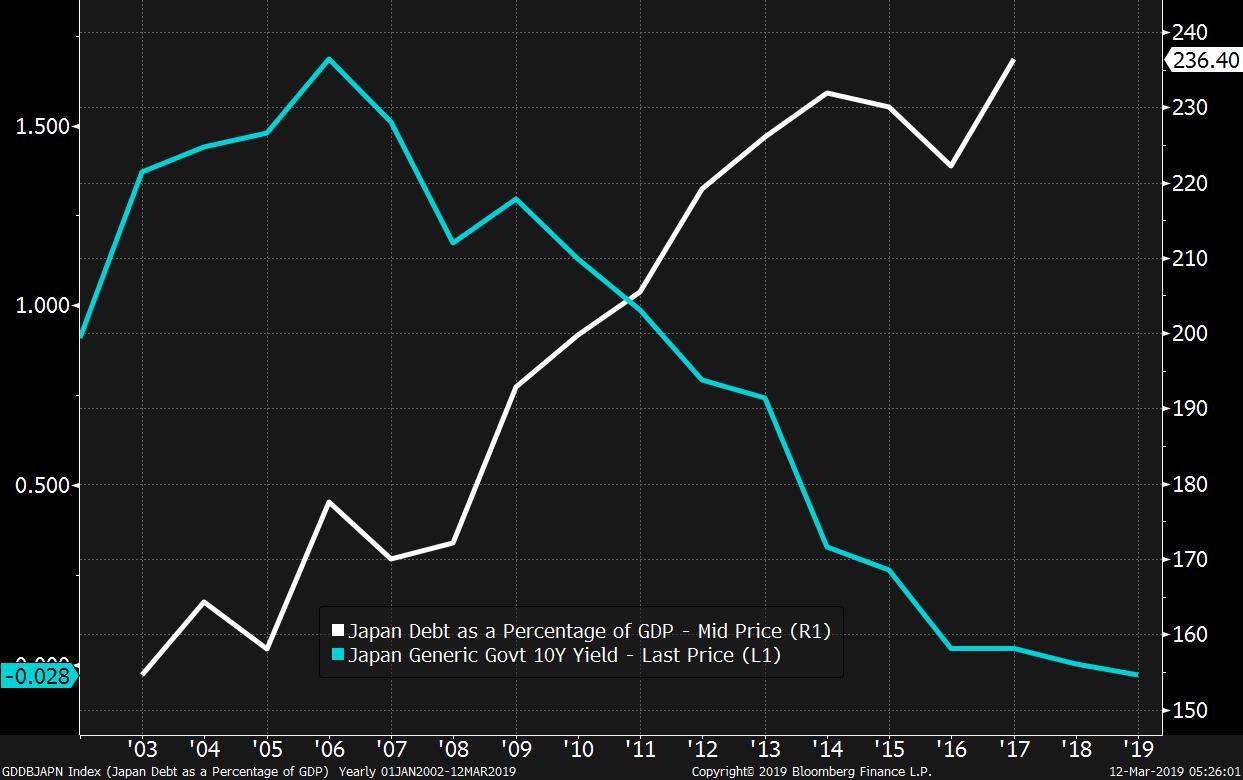

Image of the Week