Market Action

Global equities increased slightly on the week. The US 10-year Treasury note rose to 2.56% from 2.50% last week, while the price of West Texas Intermediate crude oil declined slightly to $63.60 a barrel. Volatility, as measured by the Chicago Board Options Exchange Volatility Index (VIX), declined to 12.62 from last Friday’s 13.21.

According to a copy of the special counsel’s report released Thursday, Robert Mueller found extensive interference in the US 2016 election by the Russia government and an affiliated company, though he didn’t conclude that there was collusion with the Trump campaign and decided not to provide judgment on obstruction of justice by President Trump but rather left the decision to the Congress.

China recorded a 6.4% economic growth rate in Q1, surpassing the expectations of many economists. Growth was supported by strong industrial production, which surged 8.5%, and consumer spending, which grew by 8.7%. In recent months, the government issued new measures – such as tax cuts, infrastructure spending and looser monetary policy – to help stabilize business activity and stimulate the economy. In addition, the recent ease in trade tensions between the US and China helped lift business confidence. Nonetheless, China’s growth still is the slowest in decades, and economists and the government expect the economy to continue to slow. Currently, the government’s growth target is at 6.0%-6.5% for 2019.

The US and Turkey have failed to break their impasse over Turkey’s plan to deploy a Russian air defense system the Pentagon says could jeopardize US fighter aircraft including Lockheed Martin’s F-35, which Turkish manufacturers helped build. Turkish officials repeated that the deal with Russia has been signed and is final, while the US has threatened to impose sanctions under legislation that allows the punishment of entities doing business with Russia, and to expel Turkey from the F-35 program. The first batch of Russian S-400 missiles may be delivered as early as June, leaving little time for the dispute to be resolved.

China produced a record 231 million tons of steel in Q1 spurred by consumption in the infrastructure sector due to government stimulus. The Q1 figure is up almost 10% from a year earlier, with production in March rising 10% to 80.3 million tons. There are caveats on the steel numbers. Analysts noted that steel purchasing is peaking earlier than normal, and is probably lower than last year, due to an earlier Spring Festival. The country’s steel use will expand 1% over 2019, compared with an earlier estimate of flat growth, before declining next year, the World Steel Association said in its twice-yearly outlook on Tuesday.

The US and China appear to be nearing an end to trade talks, and announced plans for two more rounds of face-to-face meetings followed by a signing ceremony tentatively anticipated in late May or June. European negotiators received the green light to start trade negotiations with the US after threatening each other with billions of dollars in new tariffs over an aviation dispute. The EU is trying to do its own limited deal with President Trump to address tariffs on industrial goods, in part to avoid levies he has threatened on foreign automobiles and car parts. Japan this week also stepped into bilateral US trade talks as Shinzo Abe aims to avoid tariffs or quotas on auto exports and Trump attempts to crack open Japan’s agricultural market and reduce a $60 bn trade deficit.

Click here for this week’s updated market returns table.

What could affect markets in the days ahead?

The idea of a second Brexit referendum is “very likely” to be put before Britain’s parliament again although the government remains opposed to any new plebiscite, according to Chancellor of the Exchequer Phillip Hammond. While the government was opposed to a new public vote, many Labour lawmakers are pressing their leader Jeremy Corbyn to demand a new referendum in talks with the government. Theresa May has so far failed to get her own Conservative Party behind her Brexit divorce deal and has reached out to the opposition.

With roughly 15% of the constituents of the S&P 500 Index having reported, first-quarter earnings are expected to decline approximately 3.8% year-over-year, according to FactSet Research. Meanwhile, revenues are expected to expand 5.2%.

Unofficial preliminary election results showed Indonesians re-electing President Joko Widodo for a second five-year term, but his nationalist opponent has questioned the count, setting up political uncertainty in the world’s third-largest democracy. The preliminary election results are based on the tabulation of ballots by government-approved private pollsters at a sampling of voting stations across the country. Such tallying, known locally as quick counts, has proven accurate in past elections.

This Week from BlackSummit

Echoes from the Riviera of Purgatory: Investing for the Future

John E. Charalambakis

Recommended Reads

Futures Guru Targets Libor Replacement

Tense Border Standoff Threatens East African Stability

What America Can Achieve After Trump

China in the Balkans – The Globalist

Video of the Week

Attorney General Barr Summarizes Findings of the Mueller Report

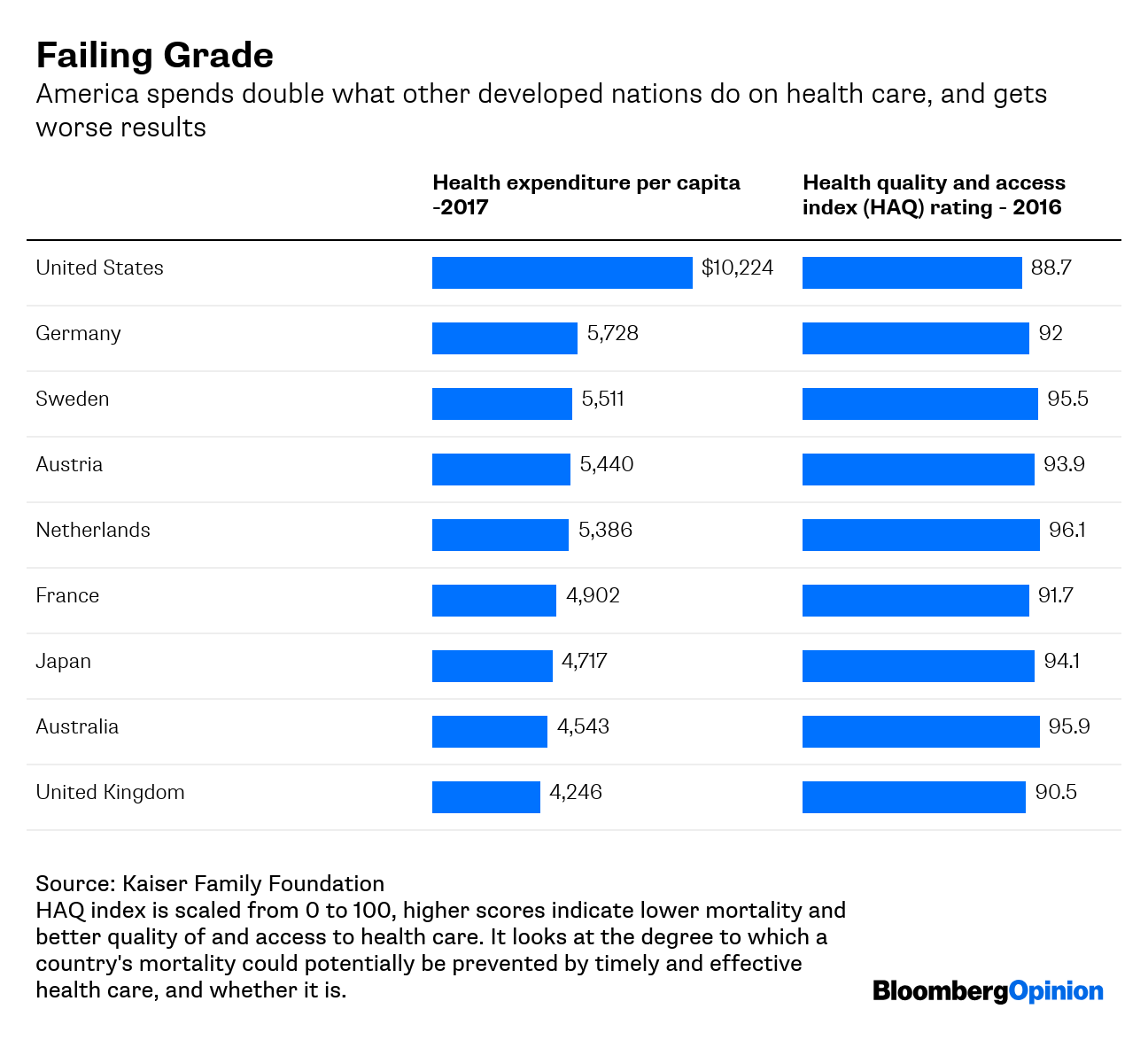

Image of the Week