John Locke was the first philosopher of the Enlightenment. His works set the stage for classical liberalism which, in turn, was instrumental in the American and French revolutions. The current betrayal of Lockean principles reflects poorly on the judgment of those in charge (whether in business, politics, or social institutions). Moral objective truths, which should ultimately arise from a moral order in “the soil of human nature”, have been contaminated and distorted due to the state of human nature.

The current wars in Ukraine and Israel are nothing but a reflection of such betrayal. How else could we interpret the loss of thousands of lives along with the deprivation of hundreds of thousands for others who have lost their liberty and property? Lockean ideas on the importance of free exchange and limited power would not go well with the power exercised by megacorps, and their influence on politics, social institutions, and overall decision-making.

Our minds are distorted by the power exercised, not by moral forces, but by the powers of the mighty (including social media). However, as it is well-stated, “the might doesn’t make it right”, or as Supreme Court Justice Louis Brandeis called it, the “Curse of Bigness.” As we wrote in a previous commentary:

“When unrestricted growth and concentrated power is amassed at the hands of a few players, then the economy may end up stagnating, inequalities may start exploding, productivity may suffer, democratic institutions could become weaker, paideia may deteriorate, and extremism could start thriving. Could it be that the new road to serfdom is painted with the bright colors of the FAANG? Is it possible to repeat the historical mistakes of the past where uncontrolled business concentration advanced along a fascist path?

Is it proper to be thinking in terms of business concentration (in areas such as tech, media, telecoms, and finance) as a get-out-of-jail card for megacorps to treat their clients with contempt and impunity? If that were to be the case, then could such business concentration undermine the essence of capitalism and free markets, lead us to bubbles, deteriorate the ethics of doing business, while also being a force of radicalizing our politics?”

The power of the megacorps, which serve some of our consumer needs and wants, but which is also shaping our minds and thinking to advance special interests, may end up distorting the marketplace. When someone nowadays looks at the following two figures, they can easily comprehend the nature of such distortion. On an equal weight scale, the S&P 500 Index is flat for the year. The 7.39% YTD return is due to the likes of Amazon, Tesla, Meta, Nvidia, Apple, Microsoft, and Alphabet/Google.

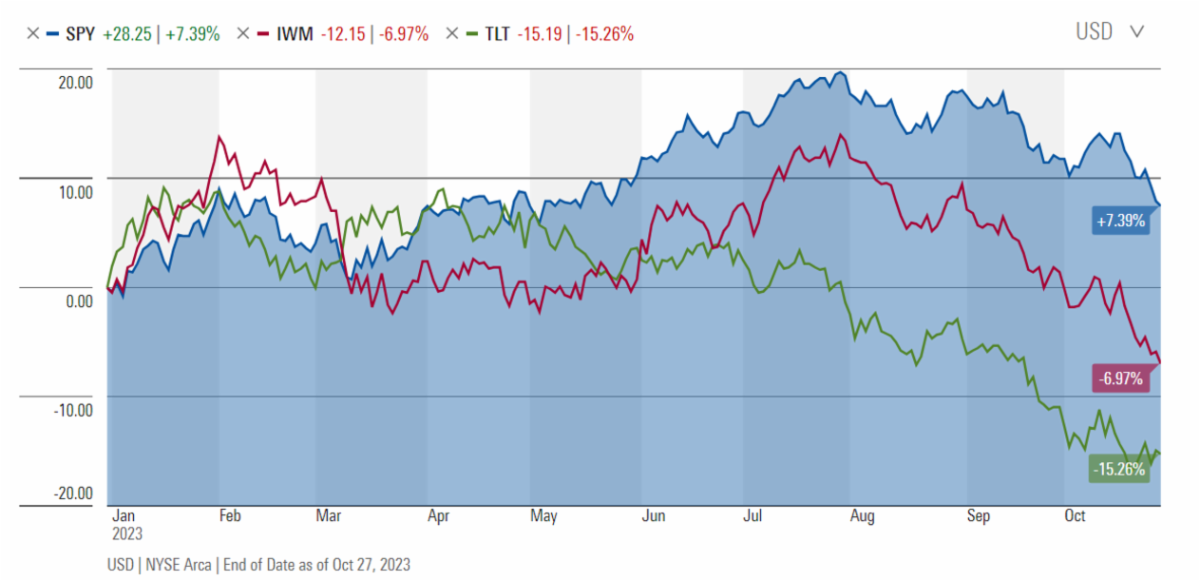

However, following the latest earnings reports, close to $400 billion has been erased from the market value, as shown below. Moreover, when we discuss market returns, we should also consider that in a diversified portfolio some allocation is also made into smaller stocks, as well as into bonds. We simply cannot say that the market enjoys good returns this year when we consider small stocks (down close to 7% YTD) and long-term bonds (down a little more than 15% YTD), as shown below.

Moreover, when we discuss market returns, we should also consider that in a diversified portfolio some allocation is also made into smaller stocks, as well as into bonds. We simply cannot say that the market enjoys good returns this year when we consider small stocks (down close to 7% YTD) and long-term bonds (down a little more than 15% YTD), as shown below.

We wrote lately that a bear steepening of the yield curve (where the yield on the 10-year Treasury rises much faster than the yield on the 2-year Treasury) may be the beginning of a period of forthcoming pain. Concerns about fiscal policy, earnings growth, geopolitical risks, debt refinancing, and constrained spending have started pushing equity markets into correction territory. The result is an abnormal situation that reflects well the current macro and geopolitical environment: the positive co-movement of yields and gold prices, as shown below.

What could we then say regarding market expectations and portfolio composition? We could borrow from Book II of John Locke’s An Essay Concerning Human Understanding, and emphasize that in times like ours, the portfolio should be based on experience (Locke’s empiricism), dualism (where emphasis is placed on good yields and expected returns from safer investments), perceptions of risks, fundamentals, and cash flow (Locke’s subjectivism), and finally power (Locke’s skepticism which in our case may reflect badly on Putin and his demonstration of power, but could also mirror the power that megacorps may have on the market). Speaking of power, what could be more powerful than a 1% drop in long-term rates? The figure below tells the story.