“There’s a retired businessman named Red

Cast down from heaven and he’s out of his head

He feeds off of everyone that he can touch

He said he only deals in cash or sells tickets to a plane crash

He’s not somebody that you play around with much”

(From Bob Dylan’s “Song Foot of Pride”)

We need anchors. Whether in personal, family, corporate/institutional, national & international aspects of our lives, we need anchors. It is the argument of this commentary that the anchor of portfolios and markets can be found in the process of forming, enhancing, and sustaining a consciousness. The abandonment of such a process negates normalcy and sows seeds of turmoil and trouble.

There is a modern opera called Death and the Powers where the main character (Simon Powers) transfers his consciousness to a computer system. Such hypothetical brain emulation brings us dilemmas, generates questions, and opens a field of wonders given the developments in Artificial Intelligence (AI). Descartes proclaimed “Cogito, ergo sum” (I think, therefore I am), while Hegel by his statement “The Truth is the spirit that knows itself”, taught us that the intrinsic value in the development of the human spirit is in realizing that the cornerstone of consciousness is represented by devotion to the truth. When you remove objective truth from any relationship, that relationship collapses.

Here are the conclusions we can draw from Descartes and Hegel and their writings on consciousness as the latter relates to contemporary markets:

- Ignoring self-evident truths is detrimental.

- Any reaction to circumstances needs a healthy dose of skepticism.

- Awareness of current facts needs to be tied not just to historical incidents but most importantly to the causes that brought up current circumstances.

- When normality reverses (e.g., inversion of an upward-sloping yield curve), repeat the process of the first three steps. History may not be replicated as facts may have changed.

- When a reversal of the abnormality starts taking place (e.g., correction of yield curve inversion) it doesn’t necessarily mean that normalcy is returning. On the contrary, problems may start materializing.

- Attempting to transfer such an anchoring process destabilizes us and the system in which we operate.

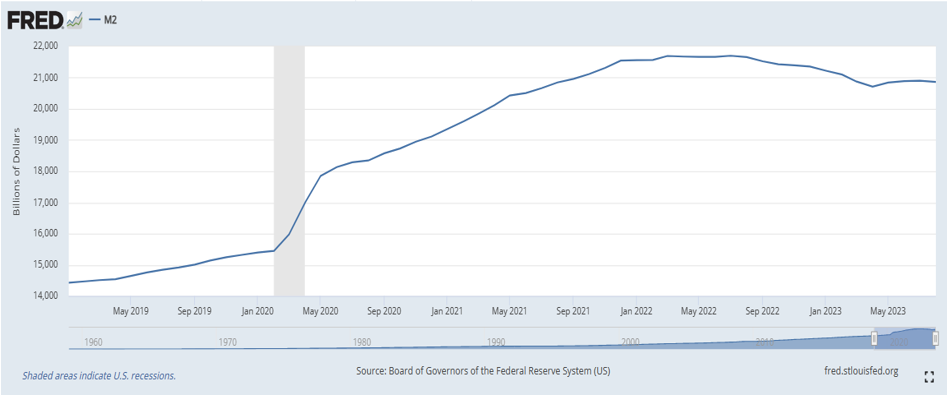

The current market turmoil, for which we have devoted a number of recent commentaries since the early days of summer, has an underlying fundamental, objective cause (self-standing truth in Descartes’ system): the desire to emulate fantasies (such as transitory inflation which by default failed Descartes’ principle of skepticism and doubt) coupled with illusions that the nature of things has changed, the infamous “this time is different”. Such emulation of fantasies made the Fed lose control of the money supply, believing that inflation wouldn’t pick up pace. Most certainly, interest rates (which have been at the epicenter of the turmoil since early 2022) wouldn’t have had to be raised so dramatically, and in such a short period of time, if the Fed had not lost control of the money supply.

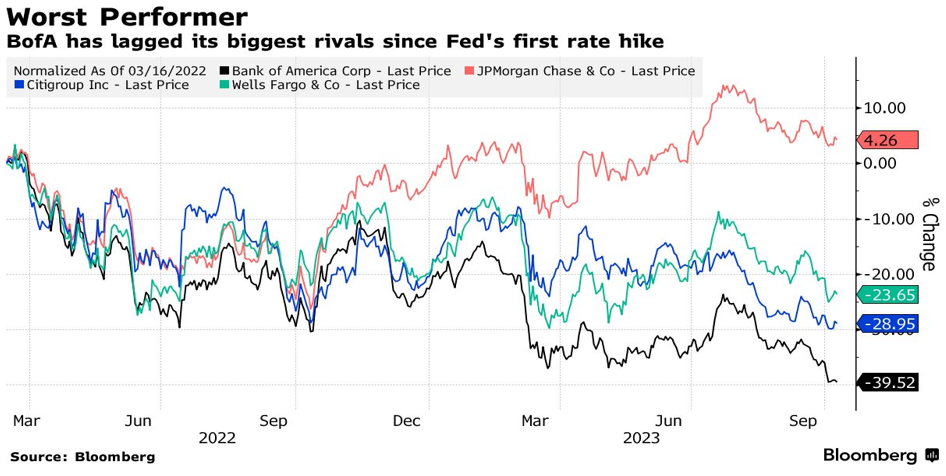

Losing perspective of self-evident truths tempted well-known banks to buy Treasuries when they were paying peanuts in terms of yield. Consequently, these banks’ portfolios recorded huge paper losses (a few of them failed last March), and as a result, their stock prices have been suffering, as shown below, with stock price losses as high as almost 40%.

Understanding today’s complex reality (geopolitically and geoeconomically) – from the war in Ukraine to today’s bloody situation in the Middle East, and from European dysfunctions to Chinese tremors, amid US political polarization, coups in Africa, and while Latin America is seeking an alternative route to prosperity – may require what Hegel called a process of contradictions and reconciliations (see closing comments regarding the bond yields). For both Descartes and Hegel, self-awareness is the starting point, however stopping there without recognition of the contemporary (not just historical) context could lead to deception, misjudgment, and ultimately to wrong conclusions and practices (hence the bank losses mentioned above).

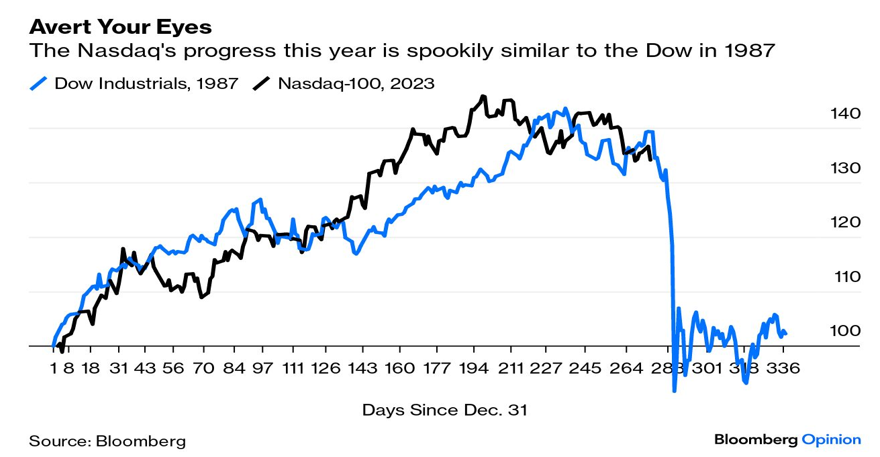

As the following figure from Bloomberg demonstrates, being aware of the similarities between the performance of the Dow Jones Industrial Average (DJIA) in 1987 (the year of the biggest crash in US markets) and the Nasdaq’s performance this year can truly spook investors into believing that a Nasdaq crash is imminent.

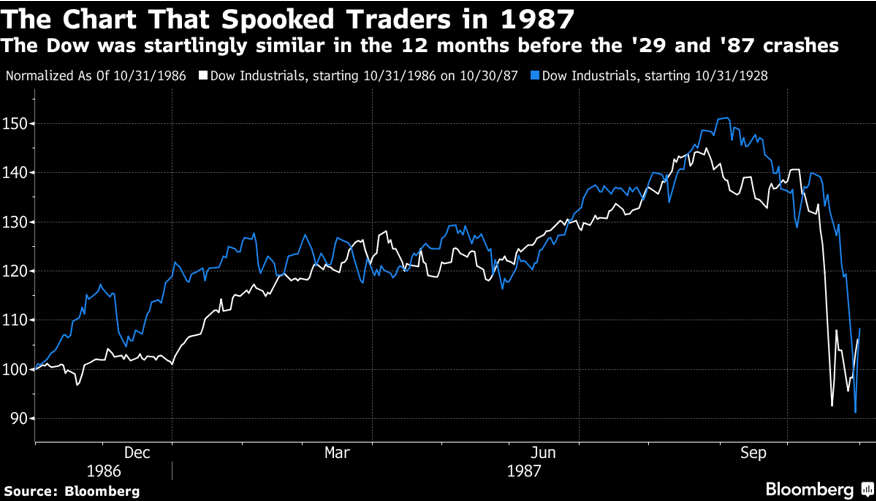

Similarly, the investors in 1987 were shocked to discover the similarities between the performance of the DJIA between October 1928 and September 1929 (before the crash that shook the markets and unleashed the Great Depression) and the DJIA’s path in 1987, as shown below.

Looking at both of the graphs above out-of-context could be misleading and make us believe of a forthcoming market crash simply based on historical patterns. Without dismissing such probability, our argument is that by removing the facts from contemporary context we may fail miserably, because as Hegel taught us, we should intimately connect our awareness of current conditions to current reality in order to unify subject and object and dissolve the distinction between knower and known.

In the most recent past, the yield curve inversion (where short-term Treasuries pay more than longer-term Treasuries) would have implied, with very high probability, a forthcoming recession. However, the latter has not materialized yet. Recently, such inversion has started reversing itself (the 10-year Treasury yield is rising faster than short-term Treasury yields). This has resulted in theshrinking of the spread (between the 2-Year Treasury and the 10-year Treasury) from 1.10% to less than 0.3% nowadays. However, such observation (awareness) when not linked to current developments, could make us believe that the economy is out of the woods and recession has been avoided.

Guess what? It might mean exactly the opposite, given that it is not the fall of the 2-year Treasury yield but rather the increase in the yield of the 10-year Treasury that has caused the shrinking of the spread between the two (a.k.a. bear steepener). If indeed the shrinking spread turns out to be a bear steepener, then corporate profits may be squeezed, a recession could come, and valuations may drop. Furthermore, bear steepening of the curve is expected to take place before a new growth cycle starts. However, the current environment is not exactly pointing to a new growth cycle, which might be interpreted as exactly the opposite, i.e., a recession within the next 6 months which would force some market pain and cause the Fed to reverse its higher-for-longer stand and cut rates, making winners out of investments in 10-year Treasuries.

Consciousness separated from truth is inconceivable. It appears we are spectators in a play where the market participants’ consciousness is attempting to be transferred into a system that we do not understand, where …

“They don’t believe in mercy

Judgment on them is something that you’ll never see

They can exalt you up or bring you down main route

Turn you into anything that they want you to be.”