Let’s start where we left the discussion in the last commentary. Rising Japanese yields are sending a warning signal, especially when we consider the statements of the Japanese central bank regarding forthcoming interest rate increases. The rate differential in favor of US Treasuries is disappearing, particularly when we consider the downward trajectory of the dollar (chances are that this downward trajectory will continue in 2026). As Japanese bonds become more attractive (largely for Japanese investors), US authorities will be facing a dilemma between:

- Higher long-term rates and/or

- Pressuring the Fed to buy more Treasuries (aka monetization of debt which could add to the existing inflationary pressures). The Treasury in the last two weeks has been buying back its own debt to slow down the long-term rates and their upward pressures.

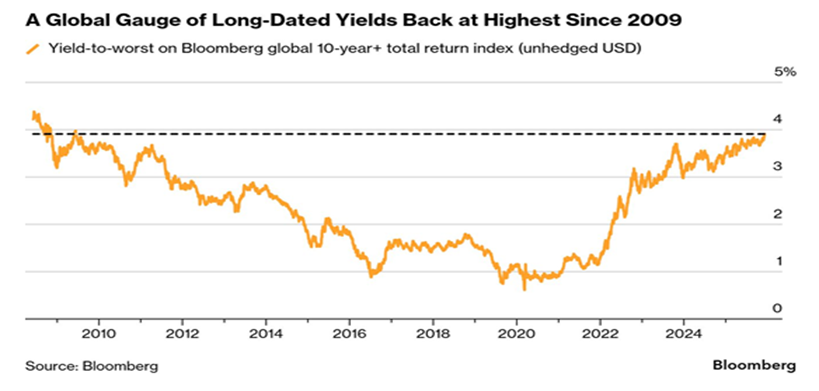

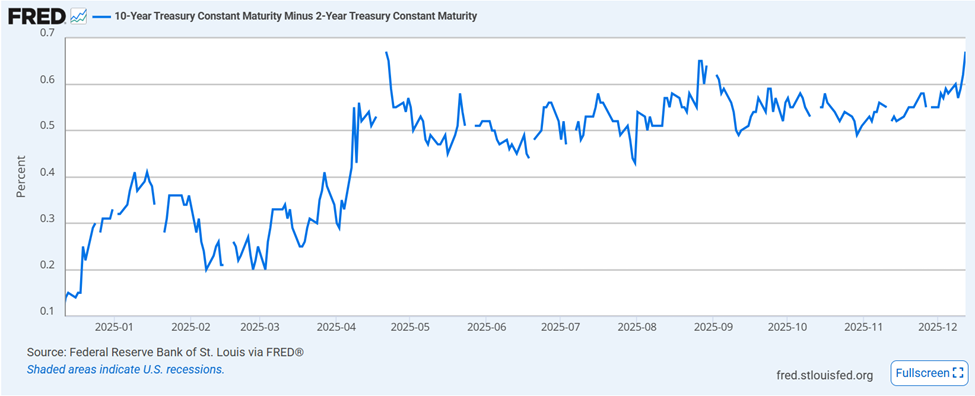

Global markets already have been facing the reality of rising long-term rates, as is shown in the first graph below. Moreover, despite three consecutive decreases by the Fed, long term rates are higher today than three months ago (see second graph below).

The upward pressure on long-term rates is happening amid a rising deficit and an exploding debt. The Japanese probably will have an easier job to overcome the pressures from higher interest payments on their debt, as supply-side measures appear to be better positioned than equivalent measures in the US. This mandates that the US needs to start creating primary budget surpluses immediately (budget balance without considering the interest on the debt), if it desires to keep the attractiveness of its Treasuries/bonds going forward. If that doesn’t happen, then the recession we are predicting to hit the US by late summer 2026, will make the affordability mess even worse. We expect the rising 10 and 2 year spread (see graph below) to decline if a recession hits, however a recession will create a myriad of other problems, and if price pressures exacerbate by then due to a dovish Fed, then we may be welcoming stagflationary forces!

In this environment and as we are facing the dawn of 2026, we still are still questioning the sustainability – let alone the rates of return – of the AI spending, as well as the high-flying market valuations. Hence, the question naturally emerges in our minds: Where then should we invest? Here is a list of potential suspects:

- Heath care sector

- Industrials

- Financials

- Energy

Regarding the energy sector, we are primarily considering well-known oil majors with solid financials and good management as well as solid dividend policy. Oil prices are down significantly, so a two-year investment plan into the sector, worths our consideration. Here are some additional facts about such argument:

- The usual suspects related to oil prices’ trajectories, range from demand (upswing business cycle) and supply (think of shale oil to OPEC+ decisions) factors, to the price of dollar (usually inverse relationship), and from financial conditions to interest rates (to name just a few factors).

- Over time, analysts have tried to identify a guiding relationship between gold and oil prices (how many barrels of oil a troy-ounce buys). Traditionally, the ratio hovered around 15-18. During Covid we saw it as high as 90 (oil demand collapsed). Nowadays it hovers above 66, as gold has skyrocketed and oil prices have dropped significantly. Quite abnormal, but these are not normal times.

- We retain some reservations if supply suffices for the existing and forthcoming demand.

- We are skeptical of any analysis proclaiming a semi-permanent state of low oil prices. We saw that scenario before in the late 1990s, only to witness a few years later record-level oil prices.

- Given the undercurrents, chances are that precious metals will stay high and possibly go higher. However, a decline in the gold/oil ratio is expected too over the next 12-24 months, therefore, considering oil majors might be a worthy consideration.

As the “ghosts of Christmas Eve” are approaching, we are always in awe of the reversal that Bethlehem set upon us. Awe is the word that comes to our minds when we consider Christ being born into poverty, spending his infancy as a refugee, experiencing the crux of minorities living in a foreign country, while dying as a criminal unjustly accused. Obviously, Bethlehem shatters the long-standing categories of weak victims and strong heroes, for there the victim emerged as the hero. Merry Christmas!