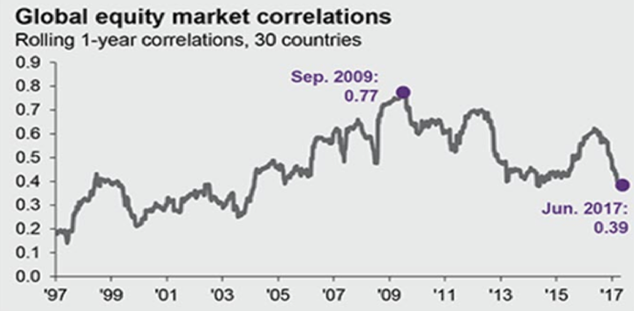

As many analysts have pointed out lately, the equity markets at the current levels are stretched, but probably not over-stretched. Global equity correlations have been falling this year (from their high of 77% in 2009 to around 39% in 2017), providing some opportunities for diversification and possible gains. Earnings are projected to be healthy, interest rates are expected to stay low, production is picking up steam, and sentiment remains strong. All these are signals that a bear market is not in the works, without of course excluding a correction if a shock disturbs the picture.

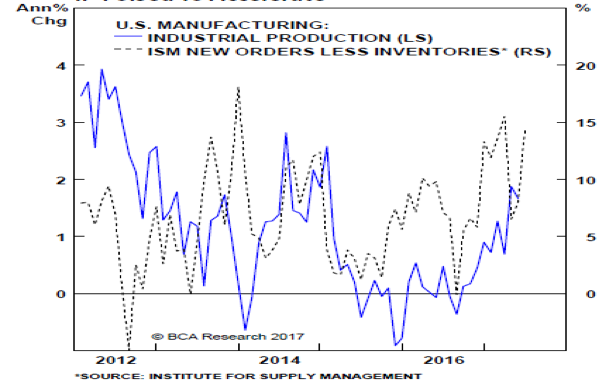

Based upon future orders and data from the ISM, industrial production in the US as shown below (including exports) is poised to increase in the foreseeable future which should give a boost to earnings, spending, and profits.

Among the major signals for a recession and a bear market would have been an inverted yield curve (where short term bonds would yield more than longer term ones), and a real short term interest rate above 2%. We have a flat yield curve but certainly not an inverted one. At the same time the Fed’s actions imply that real monetary growth (growth of money supply minus GDP growth rate) remains well above zero, suggesting expansionary policy that accommodates asset price upward trajectory.

Given the above, we could say that we would rather opt for a little bit greater exposure in high yield bonds, but avoid MBS (mortgage-backed securities).

The additional fact that global equity correlations are falling – as shown below – under current global macroeconomic conditions make us a little bit more comfortable for emerging markets allocation.

The selloff in the global bond market and the central banks’ quasi-action and talk has reduced the spread between the ten-year Treasury and the German ten-year bonds. Such reduction could be perceived temporarily as bearish for the US dollar, and if the Fed tightens soon or starts contracting its balance sheet, then we would not be surprised if credit spreads widen temporarily. However, we expect such Fed action to be short-lived and hence a widening in the credit spread in the next 3-6 months could be perceived as a buying opportunity for the particular asset class.

Allow us to close this commentary with some thoughts on US bank debt. What we have been observing is that bank debt exhibits a zero growth, while their assets/loan portfolio and the net interest margins are rising. Looking at bank bonds and adjusting for credit quality and duration, we observe that bank spreads look attractive. Therefore, it may worthwhile for investors to look into both senior and subordinated bank debt.