In the final act of Mozart’s opera Don Giovanni, the statue of Commendatore – whom Don Giovanni had killed – appears at the dinner. After all, Don Giovanni in his hubristic attitude and spirit had ordered his servant (Leporello) to invite the statue of Commendatore to the dinner party. For Don Giovanni, it was a party that ended all of his parties.

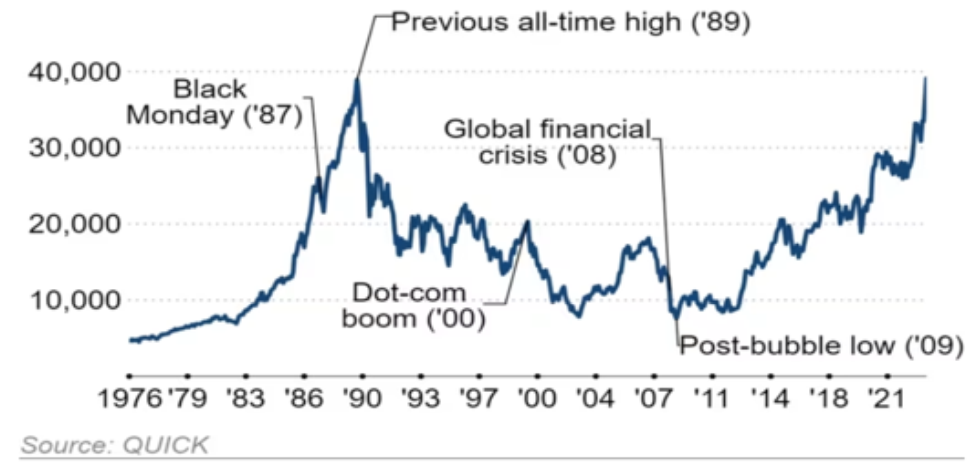

After 34 years, the Japanese Nikkei Index finally surpassed the record it set back in December 1989. The graph below shows the exponential growth of Japanese stocks in the 1980s, their crash (due to unsustainable debts) that lasted close to 25 years, and their ascendance which took almost 10 years before reaching the level that the index had achieved back in 1989. The 1980s was the Japanese version of a Don Giovanni party marked by hubris.

The Japanese market is the best-performing market so far this year. It is up more than 17%, and as we explained to our clients a few months ago, the prospects were good and remain promising. What are the factors that led to such great performance for the Japanese market? First of all, strong earnings; second, valuations were attractive; third, upbeat expectations; fourth, a resurgence of manufacturing; fifth, significant improvements in corporate governance along with institutional reforms and practices (such as

implementing better capital efficiency metrics); and finally, a rotation out of Chinese stocks and into Japanese equities.

The overtures in Don Giovanni remind us of those in Figaro as the stage in both opens with a servant in a predicament. However, in Figaro an amiable guile moves the opera, while in Don Giovanni it is a sinister guile that drives the action: two dramatically different spirits. Even though Leporello tells Don Giovanni that he is leading a rotten life, he never can act decisively and leave his master, accommodating his demands. Don Giovanni is nothing less than the unrepressed id of a particular segment in society siphoned through self-centeredness and deception.

Truth fails to define the relationship between Don Giovanni and Leparello. This unfortunate fact is where Mozart’s opera meets the markets. The truth of a forming bubble could not sway the Japanese market in the 1980s, the American market in mid 2000s, or the Chinese market in the 2010s. Prosperity and market upswings built on credit cannot be reflections of fundamental wealth creation.

Now when we look at China’s large-cap index (represented by the ticker FXI, see graph below) for the last two decades, we observe that all the gains made in the last 15 years have been erased, especially since 2021. The Chinese boom was financed by debt (a cynic would say that any resemblance to the Japanese case is coincidental). The great wall of debt steroids (from real estate to infrastructure spending, and from municipal operations to special investment products) financed an extraordinary growth which collapsed in the last couple of years and is now seeking rescue from a Japanese-like stagnation.

However, as we wrote a couple of weeks ago, Chinese assets have started exhibiting signs of renewed strength, while confidence seems to be rising. A number of measures taken has been fueling an upturn in Chinese stocks, and we would not be surprised if that trend continues. Clear signs (besides the measures taken and the rising confidence) include the narrowing of spreads, rising liquidity, and currency stability, at a time when valuations are low and attractive. Such signs will become more attractive when the Fed starts lowering rates. The recovery can be seen in the Hang Seng China Enterprise Index, as shown below.

Mozart’s Don Giovanni points to relationships and reflects the three forms of Aristotelian friendship. The first one is utilitarian where people use each other without real regard for mutuality. This is the relationship between Don Giovanni and his servant Leporello. There is also, as Aristotle taught us, a second kind of philia (friendship) which can be described as a pleasurable amity reflecting ephemeral feelings. That’s the relationship that Don Giovanni seeks with all the women he pursues while chasing momentary gratification. However, there is that third type of philia which Aristotle calls primary and pure because it comes from arete (virtue).

Market valuations can also take the form of these three types of relationships: Utilitarian valuations reflect a trading strategy without consideration of a disciplined investment strategy. Ephemeral valuations based on sentimental feelings and a momentum/bandwagon/minion-mentality advancing bubbles, which always burst. Pure valuations reflect an investment strategy mostly dependent on fundamentals.

At the conclusion of Don Givanni, there is relief but no reconciliation. Don Giovanni is sent to hell. Now that he has gone to hell, the core element which brought together everyone else (Donna Elvira, Zerlina and Masetto, Don Ottavio and Donna Anna, and of course Leporello), i.e. their desire to punish Don Giovanni, has disappeared so they go their separate ways. All of them have a certain but limited goodness about them, but that never translates into something more that can carry the value forward.

As we look at formulating an allocation strategy, the anti-Don Giovanni elements should guide our choices: True and solid fundamentals, anchored faith in a competent executive leadership, and a strong or strongly recovering business environment. Otherwise, we better be careful whom we invite to dinner, even if in our hubris we think they would never come!