Market Action

This week saw only marginal global equity gains as there were mixed third-quarter earnings results and rather dull Brexit news. As measured by the Chicago Board Options Exchange Volatility Index (VIX), Volatility was down by 7% compared to last week. On the other hand, the yield on the 10-year US Treasury note rose to 1.81%. An unexpected drop in inventories cause the price of a barrel of West Texas Intermediate crude oil to rise 5%, to $56.36 a barrel.

On Tuesday, lawmakers in the United Kingdom’s (UK) Parliament voted to reject a limited timeframe for reviewing legislation related to Brexit. This means the UK will most likely not be leaving the European Union (EU) by Prime Minister Boris Johnson’s October 31st deadline. It is likely that the EU will approve a third Brexit extension to prevent a no-deal Brexit from occurring. Prime Minister Johnson announced on Thursday that he will be asking UK lawmakers to approve a general election to be held December 12th which he believes will allow more time for Parliament to ratify his current Brexit plan.

In its World Economic Outlook, The International Monetary Fund (IMF) reduced its projected growth rate for China’s economy next year to 5.8%, which is a reduction from the 6.1% forecast for 2019. Though the IMF projects a slowdown for China’s economy, it forecasts a recovery in the global economy. After an anticipated slowdown to 3% this year, the IMF expects a global economic growth rebound to 3.4% in 2020.

Canadian Prime Minister Justin Trudeau’s and his Liberal party won a second term in the national elections held this week. The Liberal party won the most seats in Parliament but fell short of the majority. While the Liberals have the best chance at forming a government, it will have to rely on opposition parties to pass legislation.

Chile has been experiencing its worst civil unrest in decades. Chile’s central bank cut its interest rates for the third time in five months as the unrest threatens to slow economic growth. The board of the central bank met after nearly five days of protests which have left 18 people dead so far. The protests, along with the weakening Chinese demand for copper has created uncertainty for businesses and consumers and has reduced the outlook for investment.

Mass protests have also erupted in Lebanon. What began as a rebellion against new taxes placed on calls made from the app WhatsApp, protests have quickly grown into something greater. It is clear that anger has long been simmering in Lebanon as its people have finally had enough of the corruption and the inept political class that has ruled the country since the 1980s. In response to the protests, Lebanon’s cabinet signed off on a series of reforms including halving the salaries of certain government officials, implementing new levies on banks, and containing waste and corruption.

In President Mario Draghi’s last monetary policy meeting, the European Central Bank (ECB) decided not to change interest rates. ECB officials suggested rates will stay relatively the same or lower until there is evidence to suggest an acceleration of pick prices. Hungary also left its monetary policy unchanged this week. This coming Thursday, Riksbank (Sweden) and Norges Bank (Norway) will announce no monetary policy changes as well.

What Could Affect the Markets in the Days Ahead

If China signs a partial trade deal with the US in the coming weeks, they are expected to buy at least $20 billion of US agricultural products in a year and will consider boosting purchases in future rounds of talks. Consequently, market uncertainty regarding the trade war will be reduced which may become a force of market stabilization.

According to a poll by Bloomberg, the majority of economists believe the US Federal Reserve will take a break from cutting interest rates after a 25-basis point rate cut again next week. According to the CME’s FedWatch tool, odds of a cut in the fed funds target rate to 1.50-1.75% are at 94%. However, we believe that the rising conflicts (domestically as well as abroad) may start pushing prices higher next year.

Japan will be announcing a policy decision in the next few days. The Bank of Japan is expected to warn markets of slower economic growth and that policy rates may fall deeper into the negatives.

European banks like Deutsche Bank, HSBC, Credit Suisse, ING, BNP Paribas, and Santander will report third-quarter numbers. Analysts have been downgrading earnings estimates for the last 19 months, so there is little anticipation for optimistic results.

This Week From BlackSummit

Recommended Reads

Video of the Week

How coastal erosion destroyed a Ghanaian village

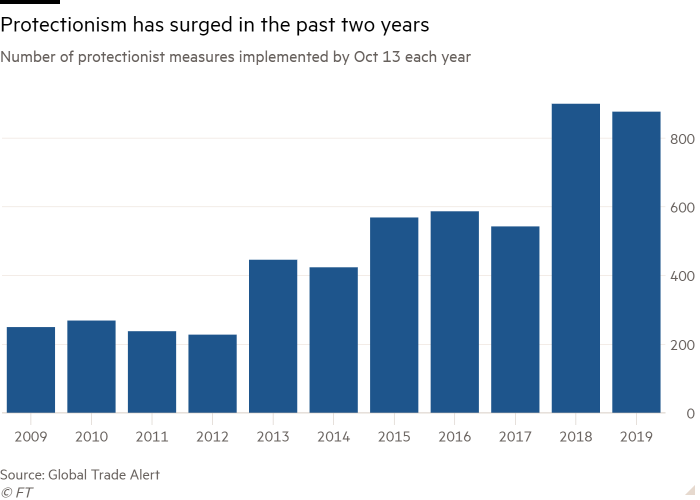

Image of the Week