Market Action

Global equities rose last week on hopes that looser monetary policy will keep the global economic expansion intact and on news that US – China trade talks will resume at next week’s G20 meeting. Yields on the US 10-year Treasury note fell below 2% late in the week but trade near 2.06%. The price of a barrel of West Texas Intermediate crude oil rose $5 on the week to $57.50 on increasing tension between the US and Iran. Volatility, as measured by the Chicago Board Options Exchange Volatility Index (VIX), fell to 14.7 from 16 last Friday.

Hong Kong officially halted work on bill that would allow extraditions from the territory to mainland China for certain crimes. The moves came after millions took to the streets in protest. Protesters also demonstrated at the police headquarters regarding the cases of 24 protesters who were arrested during the largely peaceful demonstrations; protesters demanded the government drop the cases and stop referring to the protests as a riot, which could lead to heavier jail terms.

US President Donald Trump ordered airstrikes against Iranian targets on Thursday in response to a series of provocative Iranian actions near the Strait of Hormuz in recent weeks. At the last minute, after the planes were in the air and the ships in position, the operation was called off.

There was a confluence of central bank meetings last week:

The Fed set the stage for a rate cut at its late-July meeting, and markets priced in a significant chance of a 50 basis point cut at that gathering.

At the annual European Central Bank forum in Sintra, Portugal, outgoing ECB President Mario Draghi laid the ground work for additional easing through rate cuts, additional quantitative easing and forward guidance.

The Bank of England nominally retained its modest bias to hike rates if Brexit proceeds smoothly, though at the same time acknowledged increasing risks from Brexit and slowing global growth.

The Bank of Japan kept policy unchanged but suggested it may allow 10-year Japanese government bonds yields to fall below the -0.2% threshold it had previously targeted.

Also this week, the minutes of the recent Reserve Bank of Australia meeting noted that further easing is more likely than not.

The lone hawkish outlier was Norway’s Norges Bank, which raised policy rates to 1.25% from 1% and signaled continued gradual, cautious tightening. Norwegian inflation is running at 2.4% a year, above the central bank’s 2% target.

Japan’s exports fell for the sixth straight month, down 7.8% year over year in May. Capital goods, auto parts and steel were the main drivers of the decline.

Mexico became the first country to ratify the US-Canada-Mexico agreement, the North American Free Trade Agreement replacement. Canada and the US have yet to ratify the deal.

The race to replace Theresa May as leader of the Conservative Party has reached its final stage with Boris Johnson and Jeremy Hunt chosen as the two candidates to contest the leadership. It is now up to a vote by the Conservative Party’s 160,000 members, the results of which will be announced July 22nd.

What Could Affect the Markets in the Days Ahead

A summit of 28 European Union leaders failed to reach agreement on who should take on the bloc’s top jobs. The talks, held in Brussels, continued until the early hours of Friday morning without candidates being finalized. The group made plans to reconvene on June 30th to try again. The leaders are under pressure to reach agreement on a package of top positions before the new European Parliament holds its first session on July 2nd and elects a president.

Prospects for a US Federal Reserve rate cut at its July meeting and hopes that the US and China will reengage in trade talks at next week’s G20 summit, forestalling additional tariffs, helped drive the S&P 500 to a record high close on Thursday. The rally came despite clear signs from global government bond markets that growth is slowing and central banks are at risk of losing their inflation anchors to the downside. Equity markets are betting that the Fed, which strongly hinted at a cut at its next meeting, and other central banks will be able to provide enough stimulus to keep the global economic expansion intact, while record-low bond yields in Europe and near-record low yields in Japan suggest fixed income markets are skeptical of that narrative. This year’s breathtaking bond rally has pushed the tally of negative-yielding global debt to over $12.5 trillion.

Washington and Beijing have confirmed a meeting between President Trump and President Xi Jinping at next week’s G-20 summit in Osaka. While no breakthrough on trade is expected given the wide differences in negotiating positions, markets are hopeful that are that talks will be productive enough to keep the US from imposing tariffs on the remaining $300 billion in Chinese exports to the US.

This Week from BlackSummit

Weaponizing Foolhardiness in the Midst of Rising Geopolitical and Geoeconomic Risks

John E. Charalambakis

Recommended Reads

Alexander Hamilton Would Not Approve of Today’s Federal Reserve

Facebook co-founder: Libra coin would shift power into the wrong hands | Financial Times

Here’s why Jeffrey Gundlach thinks Trump might drop out of 2020 presidential race – MarketWatch

Europe must find its will to power | Financial Times

Is Africa Experiencing a Democratic Moment?

Video of the Week

Protesters Return to Hong Kong Streets as Struggle Broadens | Time

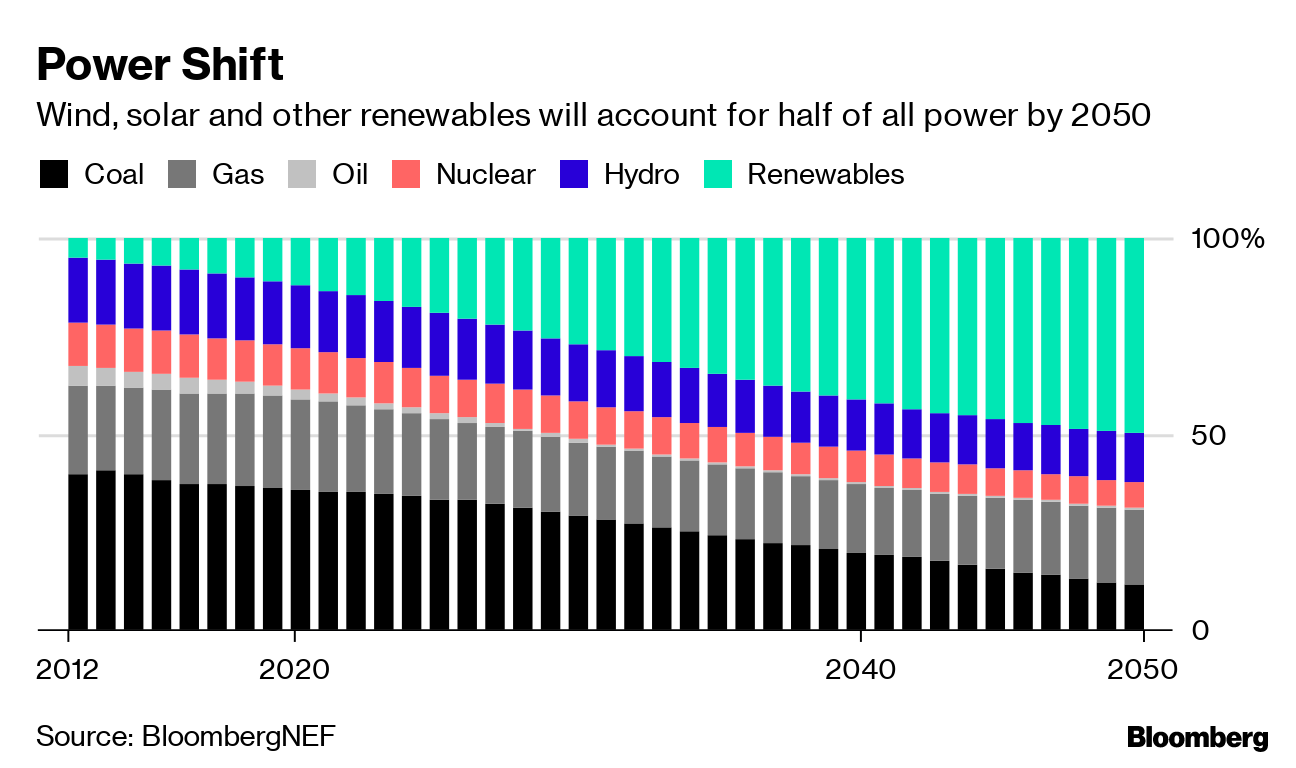

Image of the Week