Market Action

Global equities fell on the week amid a setback in US-China trade talks. The US 10-year Treasury note fell to 2.44% from 2.53% last week, while the price of West Texas Intermediate crude oil remained flat at around $61.90 a barrel. Volatility, as measured by the Chicago Board Options Exchange Volatility Index (VIX), rose to 19.84 from last Friday’s 12.87.

At the eleventh hour, China reportedly backed away from multiple concessions it made earlier in negotiations toward a comprehensive trade agreement with the United States. Chief among the issues is the Chinese government’s unwillingness to write into law many of the commitments it made during the months-long negotiations. The sharp reversal in China’s negotiating posture prompted the administration of US president Donald Trump to increase levies from 10% to 25% on $200 billion of goods imported from China while threatening to impose a 25% tariff on an additional $325 billion in Chinese goods in short order. In reply, China vowed to take “appropriate countermeasures.” On Thursday afternoon Trump, after receiving a letter from Chinese president Xi Jinping, said that a deal is still possible; however, trade broke off on Friday with no agreement announced.

Tensions between the US and Iran intensified this week as the US dispatched an aircraft carrier strike group and a bomber task force to the Middle East amid indications of planned attacks on US interests in the region by Iran or its proxies. Further heightening concerns was news that Iran will end some of its commitments under the 2015 Joint Comprehensive Plan of Action, which was intended to limit the country’s nuclear program. Iran said it will begin stockpiling heavy water and low-enriched uranium, and it threatened to rebuild nuclear facilities and resume enriching uranium unless Europe, China and Russia agree to facilitate Iranian oil sales and banking transactions within 60 days. European leaders were quick to reject the ultimatum.

Fears of increased authoritarianism in Turkey accompanied word that the mayoral election in Istanbul, Turkey, which the ruling party lost in March, will be re-run. The opposition party’s candidate holds a small lead over the candidate from Turkish president Recep Tayyip Erdogan’s PKK party. Finally, multiple short-range missile tests by the North Korean military have raised concerns that ballistic missile tests could be revived, increasing regional tensions. Strains increased further when the US seized a North Korean ship carrying coal in violation of United Nations sanctions.

The US Federal Reserve issued its second financial stability report this week, which showed that the central bank remains concerned by the high levels of nonfinancial corporate debt, particularly with regard to the leveraged loan market. The central bank expressed concerns that a shock to the economy from slowing global growth, trade tensions or a disruptive Brexit could expose vulnerabilities in the US financial system. However, the Fed also pointed out that the financial sector appears resilient, with leverage low and funding risk limited. Asset valuations remain high relative to their historical ranges and risk appetite remains elevated, the report said.

With both Australia and New Zealand experiencing slow growth and below-target inflation, the odds of the Reserve Bank of Australia (RBA) and the Reserve Bank of New Zealand (RBNZ) each cutting interest rates were about 50-50 coming into this week, so it was no surprise that the RBA left rates unchanged while the RBNZ cut its overnight cash rate a quarter of a percent to 1.5%. Forecasters expect the RBA to cut rates before the end of the northern summer.

Click here for this week’s updated market returns table.

What could affect markets in the days ahead?

How talks on Italy’s deficit targets may pan out could become clearer at the May 16 Eurogroup meeting of finance ministers. Signs of compromise will bring relief to Italian bond markets, where yields have seen their biggest weekly jump in three months with a rise of over 10 basis points. Contrast that to Spain and Portugal, often lumped in with Italy as the euro zone “periphery” – 10-year Spanish yields are at 2-1/2 year troughs while Portuguese yields have touched record lows. The latest bond sell-off, which took Italian yields to 2.7%, is small compared to the rout a year ago when yields spiked to 3.4%. But who could be blamed for a sense of deja vu?

Moody’s warned this week that a trade war could tip the US economy into recession next year, and President Trump’s latest decision to hike tariff rates on Chinese goods has possibly brought that risk a bit closer. At least the bond market seems to think so – the yield on three-month U.S. Treasury bills is on the cusp of rising above 10-year yields.

Total social financing, the broadest measure of credit and liquidity in the Chinese economy, grew much slower than expected in April, at half of March’s pace. Many expect the slowdown to prompt China’s central bank to further ease monetary policy, especially as trade tensions with the US grow.

This Week from BlackSummit

An Omen in the Making? The Argentinian and Turkish Developments

John E. Charalambakis

Recommended Reads

The Trump administration’s maximum pressure campaign: A prelude to war with Iran?

China Defaults Hit Record in 2018. 2019 Pace Is Triple That – Bloomberg

5 Takeaways From 10 Years of Trump Tax Figures – The New York Times

Fed Issues More Warnings on Danger of High-Risk Company Debt

There Is No Grand Bargain With China

May Fourth, the Day That Changed China

Video of the Week

https://www.linkedin.com/feed/update/urn:li:activity:6527959746518016000/

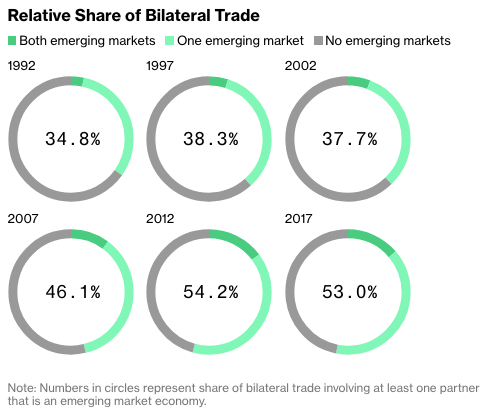

Image of the Week