Given the fundamental trends, we expect global growth to remain healthy in 2018, and therefore we also expect that the credit risk appetite will also remain healthy in 2018. Having said that, we should also state that we expect some tightening in the spreads between investment grade (IG) securities and high yield (HY) securities. In the overall framework, we should take into account the high valuations and the accompanying fatigue; however, the undergoing trends are such that should limit the effects of widening spreads.

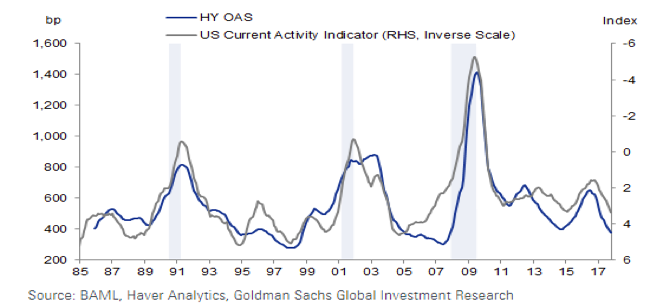

If we add three Fed hikes into the picture, we could say that our initial preference for 2018 would be to overweight IG vs. HY and furthermore to overweight Emerging markets (EM) dollar credit over US HY. As the following graph shows, the high correlation and co-movement between improved economic conditions (right inverted scale) and the narrowing of spreads (left axis) is indicative of efforts and trends to normalize financial and economic conditions. As the Fed embarks on shrinking its balance sheet and raising rates, we expect the effects on financial markets not to be significant.

On the other hand, we expect the ECB to keep buying bonds in the EU (at a slower pace) and to continue doing so throughout 2018 and the first half of 2019. That should tighten the EU spreads and possibly become a motive for EM dollar credit. When we take into account the maturing IG and HY bonds in both the US and EU markets, then we could also say those maturities and an improving EM outlook may increase demand for EM dollar fixed income securities.

With the above analysis we should add that the upswing in commodity prices and the positive outlook for metals is also encouraging for EM dollar bonds and provides support for a smooth credit outlook in 2018.

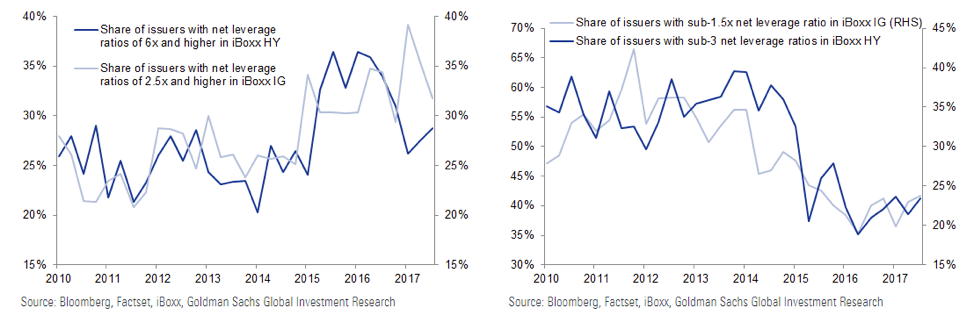

However, there is one area that could be concerning, and that is the rising trend in leveraged issuers and the corresponding decline in the percentage of non-leveraged issuers, as shown below.

The increased leverage makes HY securities vulnerable to exogenous shocks. Moreover, if inflation starts picking up steam in the second half of 2018 the HY issues may suffer.

As a concluding note, it is our opinion that IG and EM dollar securities should be preferred in 2018.