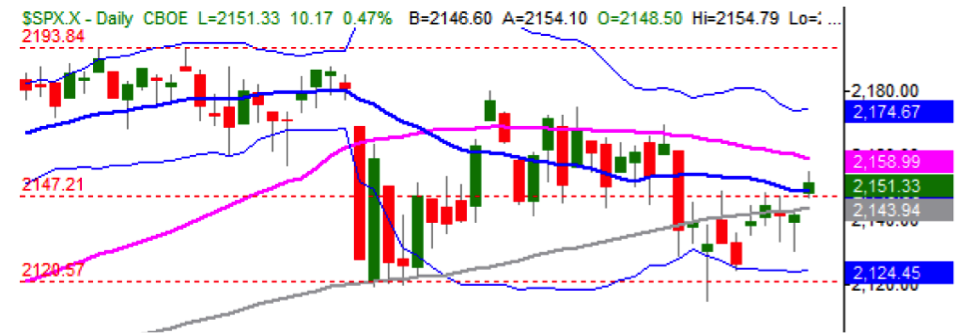

Markets are looking for an opportunity to break free from the noise of going sideways. It could be that the recently announced deals in mergers and acquisitions could become the cornerstone for such a break. On Monday the S&P 500 came close to 2150 and temporarily broke the 20-day as well as the 100-day moving average, both of which are bullish signs. However, the lack of volume was unconvincing and thus the market retreated.

Same thing has happened a few times over the course of the last few months. Unless the market breaks its way above the 50-day moving average line (around 2170), the bullishness wanted may remain wanted. Similarly, unless the floor breaks below 2115, it does not seem that major concerns should occupy the minds of investors. The market seems to be pre-occupied in the trap of noise. The technical graph below demonstrates those facts.

Despite the fact that Goldman Sachs lowered its projected outlook on profits through 2018, the market’s resilience may show the underlying momentum that possibly cannot be ignored. If that is to be the case, then shorts may found themselves trapped and the unloading of those positions could ignite a market rally. The fact is that the market remains stagnant and is looking for an opportunity to break out from such stagnation.

What could be the seed that provides an underlying momentum? Could it be the realization that governments cannot afford higher interest rates? Could it be that while central banks control short term rates, the bond market could discount that control and impose – possibly with the help of new forms of QEs – low long-term rates? Here are some quantified examples of why governments cannot afford higher interest rates.

One of the most powerful institutions in Japan is the Ministry of Finance (MoF). In a recent study they drafted, they estimated that a 1% increase in long term rates in Japan will lower the Japanese GDP by more than 12%, while triggering a huge capital loss on Japanese financial institutions. The same study reports that a 1% increase in US long term rates will lower GDP by more than 4% in the States.

If UK’s long term rates were to increase by 1% then, UK would experience a loss of close to 13% in its GDP. As for Germany, it would experience a loss of 2.5%.

What are the conclusions then from the above discussion? I would say two things:

First, the market may be seeking an opportunity to break out of the current stagnation, and if the S&P 500 breaks above the 2170 level, then we may see another phase of a bullish momentum being built up. Second, duration is extremely important for bond investors. Interest rate increases affect much more longer term maturities, therefore we recommend exposure to short term bonds.