The Wooden Nickel is a collection of roughly a handful of recent topics that have caught our attention. Here you’ll find current, open-ended thoughts. We wish to use this piece as a way to think out loud in public rather than make formal proclamations or projections.

1. Scarcity, Signals, and Share Count

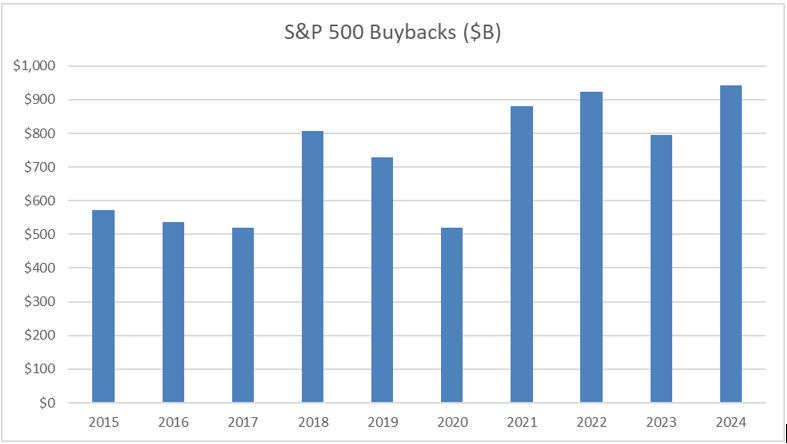

A lot of ink has been spilled over the years on the “virtue” of buybacks as a weapon in a firm’s capital allocation policy. Regardless of one’s view, the sheer force of share repurchases and their frequency cannot be denied. The first quarter of 2025 set a new quarterly record with share buybacks totaling $294B, according to S&P Global, for the S&P 500 Index. On a market capitalization of roughly $50T, that repurchase amount works out to be between a 2% and 2.5% “yield”, roughly double the dividend yield. Between the record cash generation level of firms these days and the era of ZIRP (zero interest rate policy), investors have come to expect buybacks as a regularity. Firms have obliged.

Figure 1: S&P 500 Buybacks, Source: S&P Global

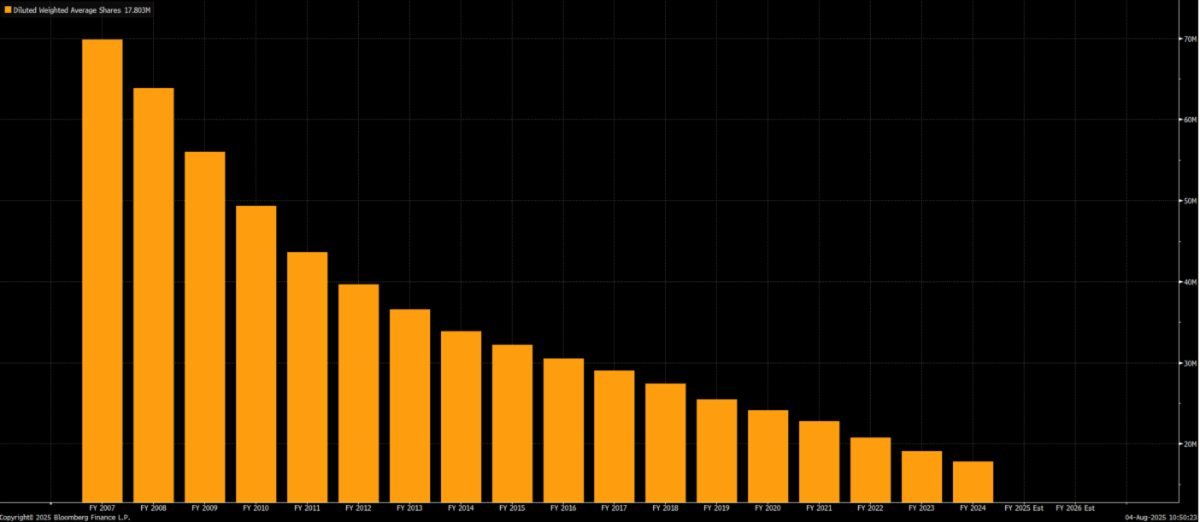

Share repurchases, at their best, are corporate alchemy; buying a dollar for 95 cents or better. When shares are retired below intrinsic value, every remaining piece of equity inherits a fatter slice of the same cash-flow pie. And unlike a dividend that must be repeated, a buyback is a one-time strike with an instant, measurable payoff. For firms that are cash flow machines, regular buybacks add to their compounding nature. Autozone has reduced its share count by approximately 2% per year for the last +15 years, generating an astounding IRR on that use of capital.

Figure 2: Autozone’s Buyback Machine

But too many companies operate like an Autozone when their underlying business isn’t that strong or durable. Most firms, alas, blunt the blade, dripping cash into the market each quarter regardless of price, turning investor capital into a dollar-cost-averaging exercise.

Sometimes it’s far more illuminating to point out when firms don’t buy back shares. Jamie Dimon, on this quarter’s earnings call, stated, “I don’t like buying back the stock at almost 3x tangible book. No one’s going to convince me that’s a brilliant thing to do.” JPM trades at 2.8 tangible book value today. It’s probably not what the market likes to hear, but it’s better for the long-term health of the franchise because if nothing else, it gives you optionality for an M&A or buying back when the market gives you chances.

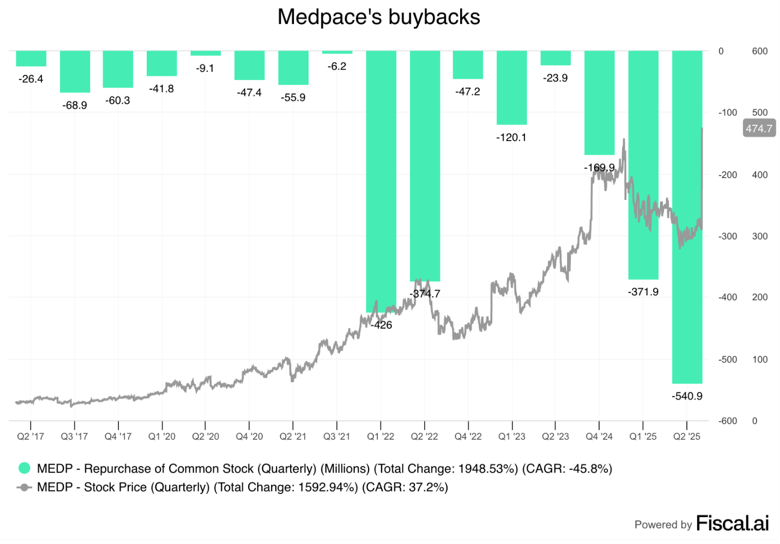

Just look at Medpace, an R&D outsourcing partner for biotech and drug companies. The history of its buyback activity is pretty muted. But when they step in, they step in big.

Figure 3: Medpace’s Opportunistic Approach to Buybacks

Notice the timing of the repurchases in the chart: a bear market for stocks in 2022 amidst fears of recession and interest rate hikes, and the market correction and tariff tantrum of this year. The firm spent $500M alone on buybacks as the share price traded around $300. Today it trades at $430. The best managers know that repurchases—like the punch of a boxer —land hardest when the timing and force are perfectly placed.

2. A Macro Rorschach Test

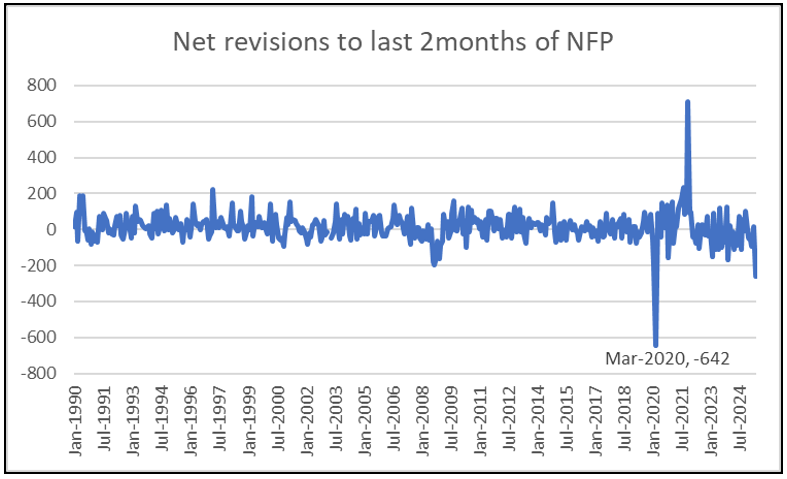

The macroeconomic landscape can at best be described as foggy at the current juncture. Tariff noise has distorted data that has already come in, while their on-again, off-again nature in the first half of the year has some looking past much of the data altogether. Which is probably why last Friday’s jobs report was met with accelerated selling throughout the day in the risk markets. It’s one thing if calamitous tariffs are postponed or canceled and push out a probable recession; it’s quite another if we were in a recession already. The report, and its historic revisions (Figure 4), even had CNBC hosts calling for an emergency Fed cut two days after the most recent meeting.

Figure 4: July’s Revisions to Prior Jobs Reports Are Historically Weak

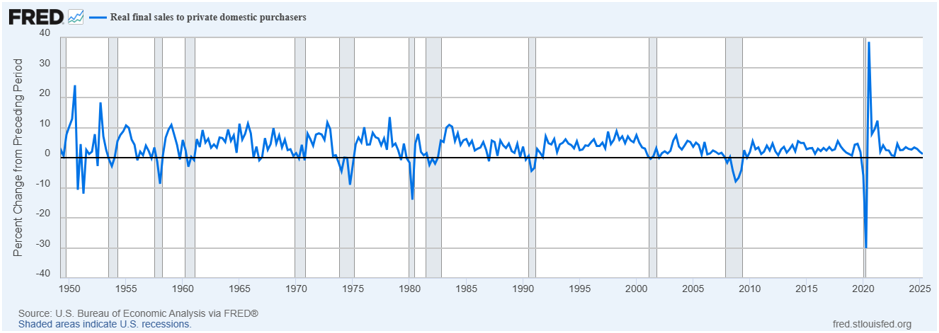

If you strip out the noise from trade and exclude the public sector, and instead focus solely on domestic investment and consumption, the slowdown is indeed clear. Final sales (adjusted for inflation) to the domestic economy have hit their slowest pace since 2022. The decline since Q3 of 2024 has been rapid, from 3.4% to 1.2%.

Figure 5: Domestic Consumption and Investment is at a 3 Year Low

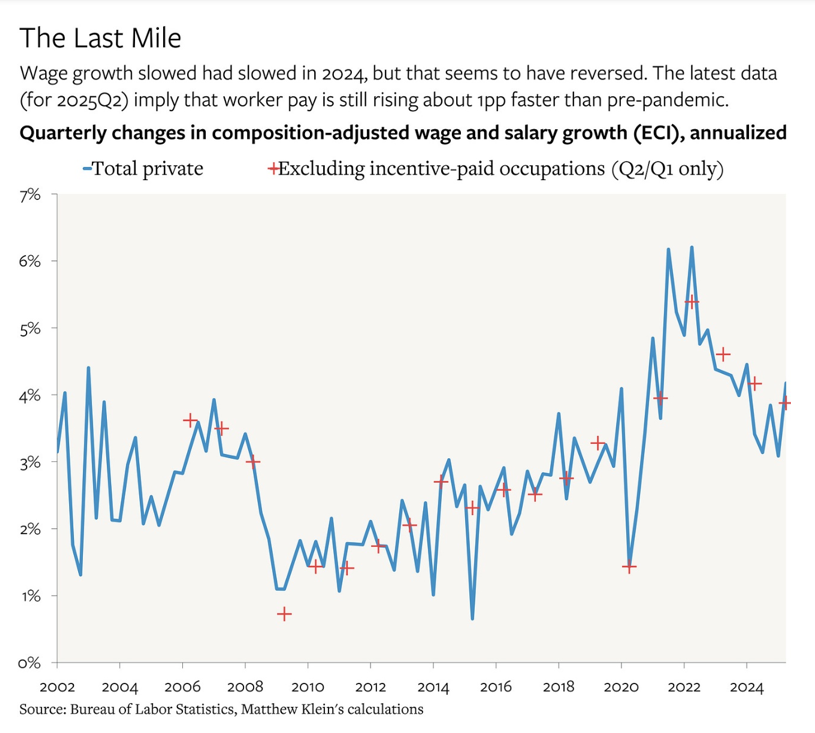

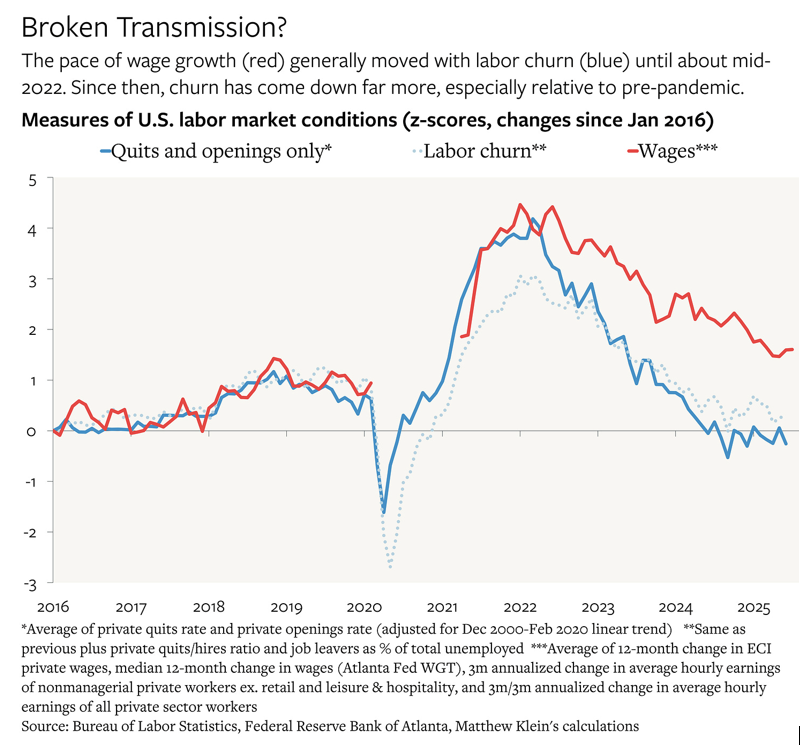

Yet amidst this weakness, wages and overall compensation have settled in at much higher levels of growth, even compared to prior late-stage cycles in the economy. Other measures of the labor market, such as labor churn, have returned to pre-Covid levels of normalcy, but wages have remained stubbornly high.

Figure 6: Wages and Compensation Have Settled Above Pre-Pandemic Levels While Overall Labor Markets Have Normalized, Source: Matthew Klein

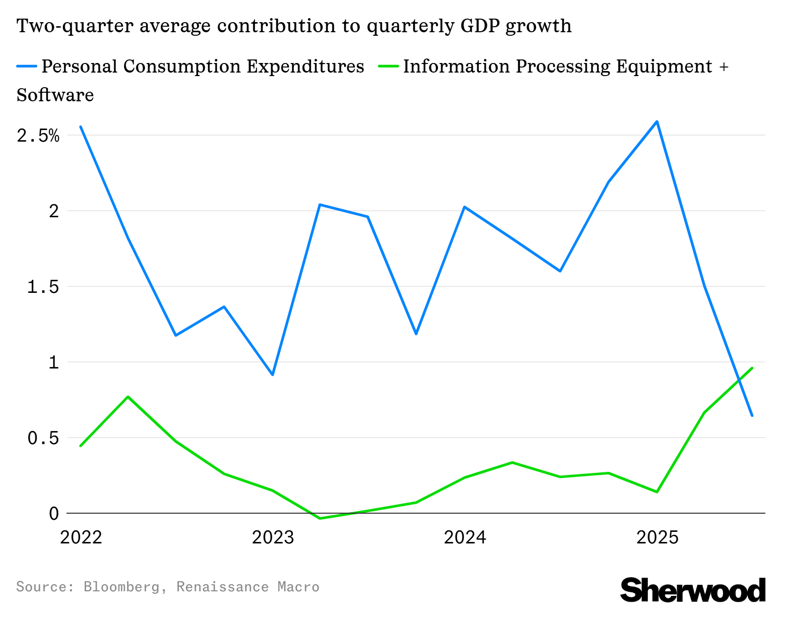

Yet despite the wage strength, domestic consumption has also taken a step back. So far in 2025, investments in data centers, AI, and computer equipment have contributed more to GDP than personal consumption, despite the latter making up more than 70% of the U.S. economy.

Figure 7: AI Spending Has Outstripped Consumption in Impacting GDP, Source: Sherwood

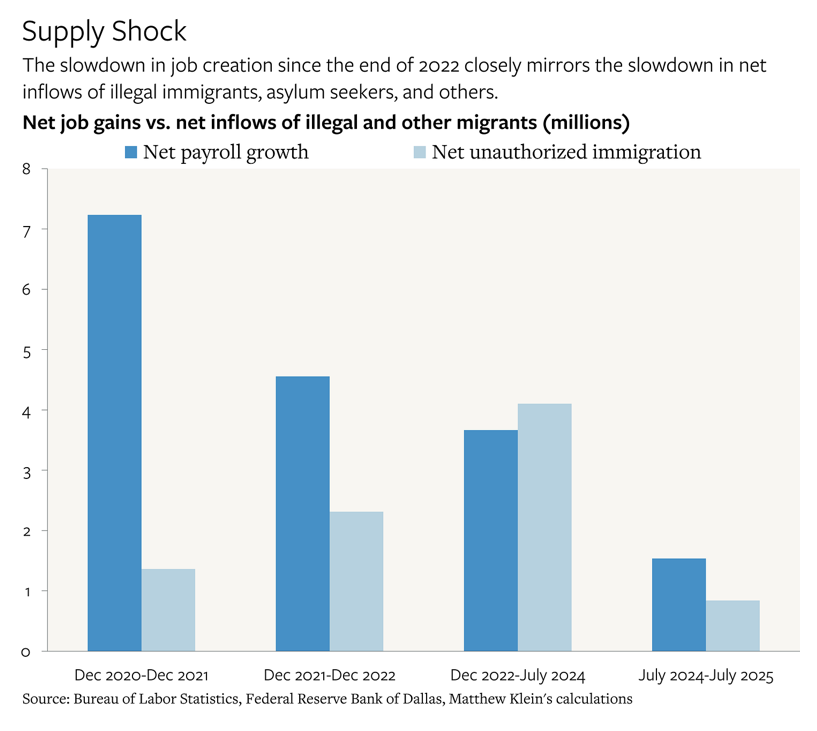

The most likely explanation for the slowdown in the past year is a rather simple one: the potential of the economy has been capped and/or diminished. It’s hard for any entity to outgrow its potential. And with the pool of potential workers capped, thanks to immigration tightening over the past 15+ months, the ability for the economy to grow at average to above-average rates has been severely hampered.

Just consider that from December 2022 through July 2024, the underemployment rate rose despite an average of 200,000+ jobs being added to the economy. Yet since then, the underemployment rate has stayed flat while average employment growth is closer to 120,000 jobs per month.

Figure 8: The Jobs Slowdown Coincides with Labor Supply Shortages, Source: Matthew Klein

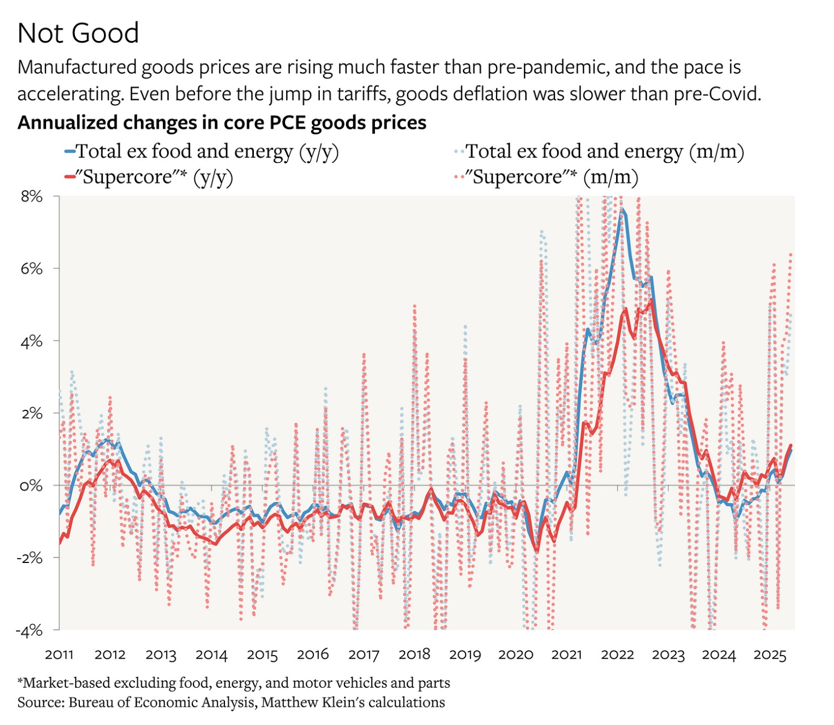

Thus, we perhaps shouldn’t be so reactive to meager employment reports or to future negative revisions in the months and quarters to come. The larger concern is probably that while much of the economy has reverted to pre-pandemic trends, prices have not and seem to be ready to head in the opposite direction, even before tariffs make their mark.

Figure 9: Prices Seem Poised to Resume an Upswing, Source: Matthew Klein

3. Recommended Reads and Listens