The Rolling Pyramid of Historical Financial Crises and the Moral Economic Imperatives: Distinguishing Causes from Symptoms

We have noted in past commentaries that our global financial system moves from crisis to crisis due to the lack of an anchor. In the previous commentary (http://stage.blacksummitfg.com/3225) we noted that the unfortunate outcome of such an arrangement is the poor choice between an unstable equilibrium and a stable disequilibrium. The latter is what has prevailed in the last ten years.

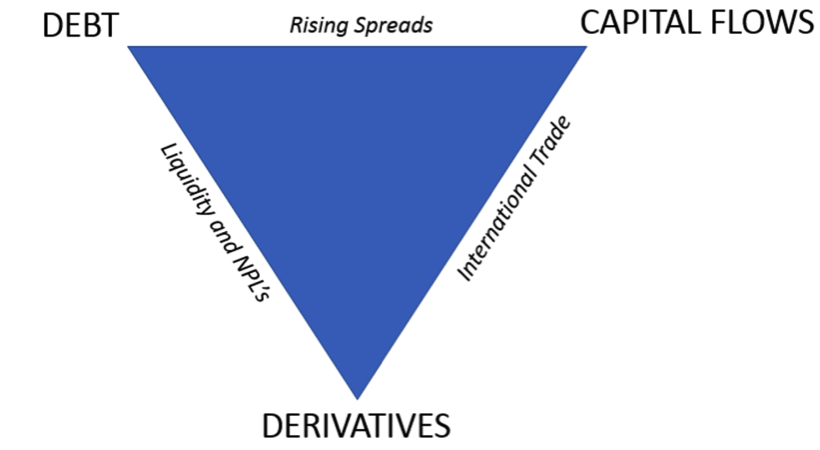

In this week’s commentary we chose to let two schematics tell the story of the rolling inverted pyramid that encompasses a myriad of complex issues, as shown in the second diagram. It is our opinion that this inverted pyramid rolls on a thin line and represents the causes of the multiple symptoms that surface in the markets and create turbulences and uncertainties.

We choose to represent the inverted pyramid with the derivatives at the bottom (whose notional amount exceeds $700 trillion), since we consider them to be the main cause of not just the financial crisis but also of the convoluted scheme of paper-collateralization and credit overextension that has dominated the markets in the last fifteen years. However, we could have chosen the debt creation (public and private, financial and non-financial) or the capital flows as the bottom, and the result would have been the same in terms of disequilibrium, turbulence, and uncertainty.

It’s a rolling pyramid, which as it rolls on a thin line, creates liquidity issues (such as the ones observed in the bond markets these days), non-performing loan issues (which the IMF issued a report/warning for the EU banks just a couple of weeks ago), while other times it creates rising spreads (e.g. between investment grade and non-investment grade bonds), and some other times capital flow issues (such as the capital outflows from emerging markets nowadays), or disturbs international trade (the growth of international trade has been slowing significantly over the last year).

Our difference from the mainstream analysis is that rising spreads, or the rising NPLs, or the bond liquidity issues, or even the decline in international trade as the cause of the market turmoil, are symptoms of the greater cause called a convoluted global financial scheme that lacks an anchor and a direction.

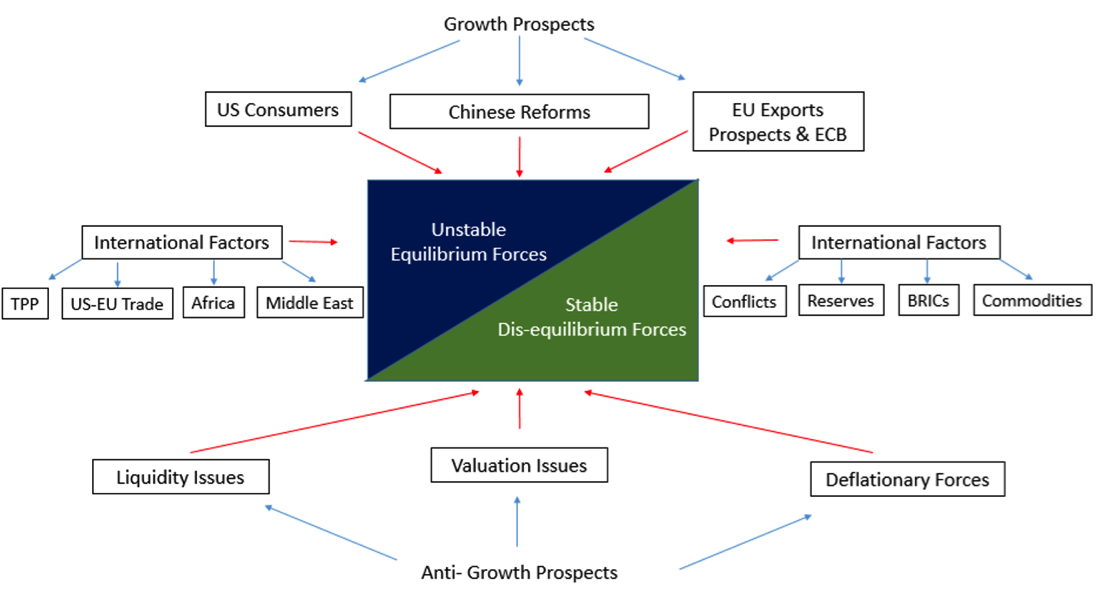

Now, if we wanted to expand the schematic above in terms of the factors and forces that shape it up and lead it to create a stable disequilibrium or an unstable equilibrium, we could offer the following schematic.

In either case (unstable equilibrium or stable disequilibrium) there are growth and international considerations. In the anti-growth camp the bond market liquidity, the deflationary forces and possibly market valuation issues are the ones that appear (or will appear) in the headlines and are blamed for market turbulence. In that same camp, international geopolitical conflicts (such as the Syrian one), declining foreign reserves (e.g. in China, Russia, S. Arabia, etc.), the turbulence in the BRIC countries, and the declining value of commodities, create an environment of uncertainty that lead analysts to conclude that a recession is coming or a bear market and correction may be imminent.

In the growth camp, we see a resilient US consumer, some Chinese reforms, and a determined ECB to cheapen the Euro and infuse quantitative easing measures in the EU as factors that can sustain growth prospects beyond current expectations. In that same camp, international trade agreements (Trans-Pacific which was reached last night, US-EU), as well as the positive prospects of Africa mitigate the Middle East concerns (even for the latter there is hope with a possible agreement similar to the Cambodia one, as we explained last week).

Overall, we tend to believe that for the foreseeable future the growth camp will prevail and a turnaround will take place from a situation of stable disequilibrium to a state of unstable equilibrium, which could not be but good news until the next crisis hits.

Let’s hope that if indeed this turnaround takes place, the moral imperative that calls for an anchor will also occupy the minds and plans of those who shape up the system.