The international financial system is based on credit. At the heart of that system is the bond market whose global size exceeds $100 trillion. Just in the US, the bond market is above $40 trillion, and the US Treasuries play a central role in that given that they are over $15 trillion. The undercurrent fiscal policy will lead to significant increases in the US deficits. As that takes place, the US should simply increase the issuance of more Treasuries at a time when global demand for those declines. Both of those forces (higher supply and lower demand) lead to lower bond prices and higher yields, something that does not sound promising for Treasuries and the greenback.

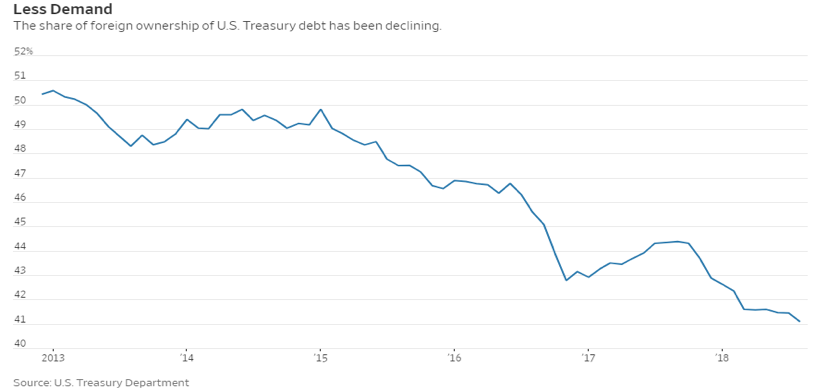

As the graph below clearly shows, the foreign demand for US Treasuries has declined significantly since 2013 and has taken a hit in the last year dropping to 41%.

While the interest rates differentials are abnormally biased in favor of the US dollar, the relative strength of the latter is particularly weak, especially if we take into account the slowing foreign demand for US Treasuries. The less-than-prudent fiscal policy in the US at a time of power rebalancing could unsettle financial markets and the greenback’s trajectory. Standing up to China might be necessary; however, trade policy cannot jeopardize relationships with traditional allies and certainly cannot be uninformed let alone naïve.

Given the above, we suspect that the higher Treasury yields may reflect higher risk premiums in the face of slowing growth and especially of deficits that could reach as high as 8% of GDP in the next ten years. At the same time, the greenback’s share of international reserves (held by central banks around the world) has fallen to 61%.

When the ten-year Treasury pays 3.20% while the ten-year Bund barely pays 0.5%, one would believe that it is a no-brainer to buy US Treasuries and thus such capital shift should keep the dollar in an upward trajectory. However, the cost of hedging the greenback exceeds 2.5% nowadays, and thus the benefits of holding dollars disappear.

In addition, tariffs and trade policies, in general, reduce demand for commodities which adds additional downward pressure to the dollar at a time when the commercial participation in gold futures turned net positive after a long time.

So, at a time when the interest rates differentials favor the greenback, profit repatriation should be boosting the US dollar, the emerging markets are under significant turmoil, the US growth far surpasses other developed countries’ growth rate, and the Fed has been taking a hawkish stand, we observe that the relative strength of the dollar is weak.

At the same time, analysts report a significant squeeze on the Eurodollar market (dollars circulated outside the US). That implies that demand for dollars exceeds their supply which could also be another cause for the October stock market turmoil. As we can understand, if the Eurodollar market experiences a significant turmoil (like it did in 2007-08), then the implications could be disproportionally big for the markets, especially if the Italian banking tremors intensify.

Based on the above, we believe that with or without the assistance of the Fed (e.g. supplying more dollars in the international markets), the dollar is susceptible to a downward trend. The benefits of such loose policy (above and beyond the fundamental reasons explained above), i.e. allowing the dollar to lose ground, could be summarized as follows:

– It attracts capital (e.g. Europeans with a stronger euro can buy US assets – including bonds – cheaper)

– It promotes US exports, possibly reducing the trade deficit, and adds to growth prospects

– Addresses the Eurodollar squeeze

– Allows easier financing of US deficits

– It counters Chinese yuan depreciation

– It also relieves higher interest rate pressures

– It builds a precautionary wall in case of an EU banking turmoil

– It advances earnings growth and the bottom line as US companies repatriate profits

– It allows greater volume in commodities trading and thus promotes the greenback’s supremacy

In closing, and based on the facts as they are being shaped by the forces above, we would say that the greenback may be facing some heavy headwinds in the months ahead.