In the first part of this series, we emphasized China’s ambition to replace (if needed by force) the liberal balance of power with an illiberal autocracy (consequently, limiting the role of the US dollar as the international reserve currency) where useful idiots (willingly or foolishly) sign up for such ambition. In this second part, we will discuss the role that energy plays in the underpinning upheaval that started with the Great Financial Crisis (GFC) fifteen years ago.

On April 6, 2020, we wrote: “So, while in the current stage we may be facing deflationary fears (and hence positive real interest rates which have consequences for fixed income asset classes), the oil sector turmoil along with the higher money supply, monetization of deficits, and the deficit spending itself may turn the tables and bring to the surface stagflation.”

Unfortunately, this assessment came to be true as we have been witnessing the above since the spring of 2022. Our writings three years ago began focusing on the role that geopolitical developments born out of the GFC will play in the current era. The war in Ukraine is a symptom of these developments and the oil market turmoil (which has been contributing to inflationary pressures) is at the crux of those developments. So, where are we headed now regarding energy markets? What is presented below is an overview of underpinning changes that our team put together. We start with an executive summary, then continue with a few vital points, and close with some concluding remarks that could be useful for investors.

Executive Summary: The Global Outlook

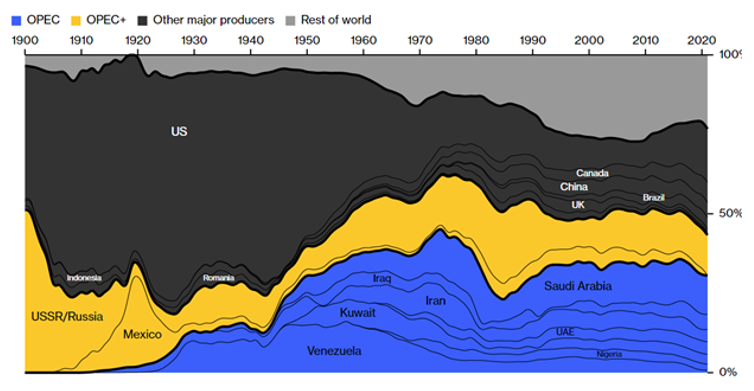

- US oil production is slowing down, which will allow OPEC to supply a larger amount of the world’s oil. OPEC will likely increase in importance due to the world’s short-term need for more oil and gas, despite the international effort to develop green energy sources.

- US green energy initiatives are dependent on transmission lines. Transmission lines have become a top priority for the renewable energy industry, but red tape and NIMBYism (Not In My Back Yard) must be overcome for the US to cut carbon emissions and decrease its dependence on foreign oil.

- Russian weaponization of its hydrocarbon supplies has led the EU to drastically increase its adoption of green energy initiatives. While the US and Europe have markedly moved towards renewables, Moscow is still finding buyers in China, India, and many countries in the developing world. Sanctions have still massively damaged the Russian economy, and Moscow’s bid on the developing world could end up ultimately weakening it for good. Even if its gamble pays off, the decoupling between the East and the West will likely be long-term.

- Miners are seeing a boom on the horizon due to the global green energy transition. Minerals used for electrification projects (windmills, EVs, etc.) like copper, nickel, cobalt, and other commodities will likely see a sharp rise in demand. The mining industry must grow at a near-unprecedented rate to provide for the green energy needed to achieve the 1.5 degrees Celsius climate benchmark.

- LNG capacity, in the short-term, must increase to meet demand in Europe during its readjustment from cutting off Russian energy. US LNG exports are likely to triple at the same time. In the long run, the West is expected to decrease its use of LNG, while South East (SE) Asia & the Pacific are expected to sharply increase their use.

- Europe will likely see tough competition for LNG supplies with Asia. Investors are wary to fund projects that would increase LNG imports as they believe hydrocarbons may become obsolete in the next 30 years. When renewable projects finally come online on a large scale, global energy prices may finally stabilize.

- US oil from Texas may flood the market if it becomes included on the Dated benchmark. This would alleviate the higher prices, especially in Europe.

A Few Vital Details: What is the essence then of the above developments?

The oil production boom that made the US the world’s largest producer is slowing.

- Frackers are hitting fewer large wells in the Permian Basin, which is a sign they’ve drained all the good ones. Shale companies’ best wells are producing less oil too.

- The average well in 2022 produced 6% less than the average in 2021.

- Domestic oil output in 2022 grew at a third of the average annual pace it did in 2017-2019 and has not yet returned to pre-pandemic levels. This slowdown was caused by investor pressure to generate higher returns, in addition to the decreasing output of well production.

- US output grew half as fast as forecasters expected last year, and it will increase similarly this year.

The decreasing production will have geopolitical ramifications.

- Oil executives say the stagnation in shale production is a precursor to more dependence on foreign energy sources, à la the ‘70s & ‘80s. They also claim that OPEC will supply a larger share of the world’s oil.

- The global market could previously count on US oil production to alleviate the effects of supply disruptions and rising demand, but if current trends continue, companies will be forced to tap less productive wells. These less productive wells would require higher oil prices to attract investment.

Oil companies’ decision making has been affected.

- The worsening productivity of wells has caused concern about the industry’s path to growth and has even led some companies to consider mergers.

- Chevron has been forced to shift some drilling into New Mexico due to missing its oil production target.

- Devon has seen its average well production fall almost 50% from 2020 to 2021.

- Some executives aren’t alarmed by the decrease in productivity, instead seeing the trend as a sign US oil production is maturing as ‘gushers’ are tapped. They posit that tighter crude supplies will push oil prices higher, making exploration of less productive wells economically viable.

- Companies in the oil fields of Texas, New Mexico, and North Dakota have tapped many of their best wells.

- If the largest drillers kept their output flat, as they did during the pandemic, they would continue drilling profitable wells for a decade or two. If they boosted production by 30% a year – the pre-pandemic growth rate of the Permian Basin – they would run out of good wells in a few years.

- Big shale companies have to drill hundreds of wells each year just to keep production flat. The world will need more oil and gas in the short term, despite international consensus on developing green energy.

- The geopolitical & market realignments stemming from the Russian invasion of Ukraine have spurred the industry to re-evaluate how the energy transition will work.

Electricity, Mining, and Energy Transition During a Remarkable Year

“There is no transition without transmission” says Rob Gramlich, founder of Grid Strategies LLC

- The fact is that the biggest impediment to general clean energy use and availability is power transmission. Power-line projects have struggled to advance and have been halted by bureaucracy, NIMBYism, or general industry stasis.

- That being said, some projects are moving forward, such as SunZia (the Southwest), TransWest Express (Mountain West), Grain Belt Express(Midwest), and Champlain Hudson Power Express (NYC), totaling $13 billion. SunZia and Champlain Hudson Power Express are expected to begin construction this year, with both ordering advanced equipment. SunZiais expected to produce 3 gigawatts of energy from New Mexico to Arizona, the equivalent of 3 nuclear reactors, where it can then flow to the West Coast. Champlain Hudson Power Express ($6b) will bring Canadian hydropower to NYC.

- While transmission development has been and continues to be slow (with all projects subject to the same risks and price tag listed above), it has become a top priority for the US renewable energy industry, assisted by the Biden administration and the IRA (Inflation Reduction Act).

- The fact that the negative impacts of climate change are coming sooner than expected is increasing the impetus for a clean energy shift, while the IRA points towards a Congress that is open to subsidize clean energy initiatives, even for the sake of geopolitics.

- In the US, there exists a separate problem pertaining to federalism vs. interstate development of infrastructure. Some infrastructure may be able to be done federally similar to the highway system; however, much of it will be done at the state level and may therefore require subsidies, etc. as the only levers available to the federal government to push states in the right direction. Not all conservative states are hostile to renewable energy, as demonstrated by the success of the wind industry in Texas.

- Russia’s invasion of Ukraine and its subsequent impact on the global energy market is hastening its transformation in a way not seen since (and which may eclipse) the 1973 oil shock and therein lies risk for the prosperity of the Russian state.

- Russian weaponization of its hydrocarbons in response to European sanctions has triggered the European Union to drastically increase support for its green energy transition, with renewable output increasing by 9%. The IRA in the US and the EU’s RepowerEU will further catalyze such shifts. For Russia, the impact of sanctions and loss of the European market has reduced oil and gas revenue by as much as 46% from last year and the impact is being felt, as Russia ‘s January budget deficit is close to half of the amount projected for the year. Nonetheless, Russia has proven more resilient than initially expected, in large measure due to its reorientation towards hydrocarbon-hungry emerging economies in India and China, who have been happy to gobble up cheap Russian fuel.

- The developing world, which has generally not signed on to Western sanctions, represents two-thirds of greenhouse emissions, affording Russia a continued market for the foreseeable future. Still, the pitfalls for the country are real and time will tell whether Russia’s emerging market bet will pay off in the long run.

- It may be necessary for the US to play a Machiavellian act; lift all sanctions in Venezuela, and while bringing online the largest oil reserves in the world, also assist and embrace development in Latin America.

- While the EU has engaged green energy policies for a number of years, energy needs threatened by geopolitical risk have increased the impetus towards a green energy transition. There exist opportunities through broad European cooperation to achieve such a transition in due course and European governments are stepping up to the plate; however, in the short-medium term, natural gas will still prove a valuable resource until that transition can be achieved. Russia will play an increasingly diminished role in providing its energy commodities to European states in the interim.

- Miners are spending billions and raising budgets for new projects, bidding on the global energy transition. Mining companies are holding more cash on their balance sheet for projects, marking a significant shift from recent years where they focused on increasing their dividends or buying back stock.

- The mining industry isn’t currently producing enough copper, nickel, and other commodities vital to the energy transition. This recent pivot reflects their attention to the issue. Analysts claim that the industry will have to grow in production at a rate achieved only at the end of the China-led commodities boom if the world is to meet the 1.5 degrees Celsius goal.

- An estimated $23bn of annual investment will be needed over the next 30 years, 64% higher than the average annual spending during the past three decades.

- Miners believe the IRA will increase metals demand due to support for clean energy projects, most of which use more metals like copper than traditional energy production facilities. Consequently, mining companies are expanding their spending on projects and exploration. Hopefully, the industry has learned its lessons and will avoid a repeat of mistakes made a decade ago when miners invested billions in new mines and ambitious deals without solid foundations. The expansions flooded the market with supply and crashed prices.

- US LNG exports are likely to triple over the next decade with the IRA designed to support local energy over imports – boosting demand for LNG. The US LNG market is set to support 29 billion ft3/d of production into 2023.

- Qatar & Oman have been working throughout 2022 and into 2023 on major LNG export contracts to Asian markets with countries including China, Japan, and Korea. Japan is looking to restart seven nuclear reactors by late 2023 to reduce its imported LNG dependence. China will likely take similar action towards renewable energy.

- Europe is expected to decrease its use of LNG beyond 2028, while SE Asia & the Pacific are expected to increase their use more than 40%.

- US domestic gas production capacity is expected to decrease in growth through 2023 as new facilities are developed. Prices at Henry Hub are expected to average $5.47/MMBtu across 2023 after reaching a high of $6.65/MMBtu during 2022. Beyond 2023, production capacity will again increase as new facilities like the Golden Pass facility in Texas go live.

- Demand in China is expected to rise in 2023 due to the easing of Covid-19 restrictions.

- Europe has a competitive advantage in LNG import capacity over any other region, but the rapid growth in demand from Asia is a serious threat for securing LNG cargo in the coming years.

- Qatar is considered among the world’s biggest LNG exporters – its majority of cargoes are going to Asia where buyers are paying a premium to attract shipments.

- The long-term target of creating net zero economies in the UK and Europe has also sapped investors’ willingness to fund the development of a fossil fuel they believe could be obsolete in 30 years.

- Europe’s attempts to be a global leader on climate change have arguably fed into the wider changes in the market.

- LNG supplies should increase in the coming years as more projects come online, but in the short term, consumers need to brace for a period of higher energy costs.

- Gazprom is preparing Power of Siberia 2, a pipeline that would connect the fields in western Siberia to China by 2030.

- International Gas Union advocates that governments ought to reconsider strict environmental policies – from drilling restrictions in the US to licensing delays in the UK – that they believe have damaged the industry’s ability to keep the world well supplied.

- If we look at history, during the 1970s Arab oil embargoes, a spike in energy prices induced an energy efficiency drive. The development of resources in regions like the North Sea and Alaska ushered in two decades of cheaper oil.

- Whether renewable developments will have the same capacity to stabilize global energy prices if gas supplies stay tight, still remains untested.

- The world’s most important oil price is about to be changed. Crude supplies from west Texas will help determine the price of millions of barrels of petroleum transactions.

- The shift in price is due to Dated Brent (the existing benchmark) running out of tradable oil to remain reliable. Its publisher (S&P Global Commodity Insights – AKA “Platts”) has been forced to make the shift.

- Starting in June, West Texas Intermediate Midland will become one of a few grades that set the Dated benchmark.

- The Dated benchmark helps set the price of two-thirds of the world’s oil and even defines the price of some gas deals. The benchmark is at the center of a web of derivatives, shaping Brent oil futures that get traded on exchanges.

- Now, traders will be able to offer West Texas Intermediate Midland (WTI Midland) to be evaluated by Platts to see if it’s the most competitive price on offer – if it is, then it could set the benchmark.

- To evaluate WTI Midland against the existing Dated grades, Platts uses a ‘freight adjustment factor’, deducting the estimated cost of transport of WTI Midland and comparing that to existing grades. The process places an emphasis on tanker costs.

- Real cargoes of crude from the US will be allowed for inclusion by July(possibly sooner). The inclusion of WTI Midland, if it comes to fruition, could increase the flood of US crude to Europe by one-fifth once traders adjust to the change.

- Platts will also have to evaluate how WTI Midland compares in quality to other grades. US terminal operators claim that WTI Midland is of consistently high quality, and some even claim that it’s superior to other crudes.

Concluding Remarks

- A New Day is dawning in the energy markets marked by transition (new benchmark, LNG, renewables, shifting demand due to geopolitics) and transmission.

- Investors could explore some allocation via holdings and exposure in LNG, carbon instruments and futures, metals mining companies, but also traditional oil companies.