Are we experiencing a tragic market filled with pathos and crowned by ironies? Are there objective patterns in the flow of history (and for that matter of market cycles/waves) related to the unraveling of contemporary events? Isn’t it the purpose of theorizing to find solutions about the end of cycles (and/or of history), and to prepare for the next cycle/chapter? The answer is maybe, if in the process of discovery, we are not willing to accept the distortions of facts, be willingly deceived by spurious correlations, and ignore fundamentals about human nature. Moreover, and according to Reinhold Niebuhr, any framework of interpreting historical facts should incorporate three broad categories, namely: tragedy, pathos, and irony.

In the first part of this series, we wrote: “ Herodotus’ message was clear: When a democratic republic seeks the fruits of an empire while drinking from the glass of hubris, power becomes elusive and blinds the vision of leaders. Skotomorphogensis is at work, and etiolation prevails. Herodotus’ warning was overlooked by the Athenians. The Peloponnesian War would end up devastating them.”

In an era during which a new cold war is emerging, it may be necessary to heed Niebuhr’s warnings in his book titled The Irony of American History, especially when we take into account that he wrote about them in 1952 in the midst of that cold war. After all, Niebuhr was a major influence on George Kennan and his containment doctrine which turned out to be one of the most important statecraft strategies ever implemented. Niebuhr’s message of pragmatism in the face of evil, unrealistic idealism, and historical waves that we may not understand (including the reaction of actors involved) should echo today for both statecraft and portfolio composition.

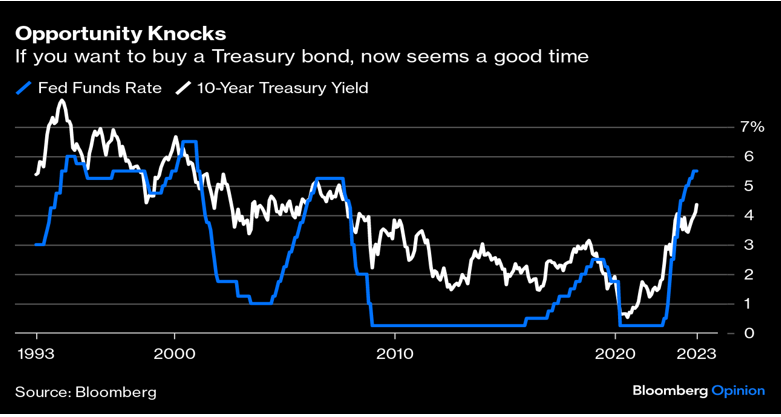

We live in a market that we can barely understand. Experts were expecting a bad equities market earlier this year, and now are reversing their calls, advocating for a soft landing. Imagine the reversal of fortunes if recession hits us in a few months. Long-term government bonds keep losing value. They have lost close to 40% since the beginning of 2022 (see figure below), due to their duration/interest rate risk.

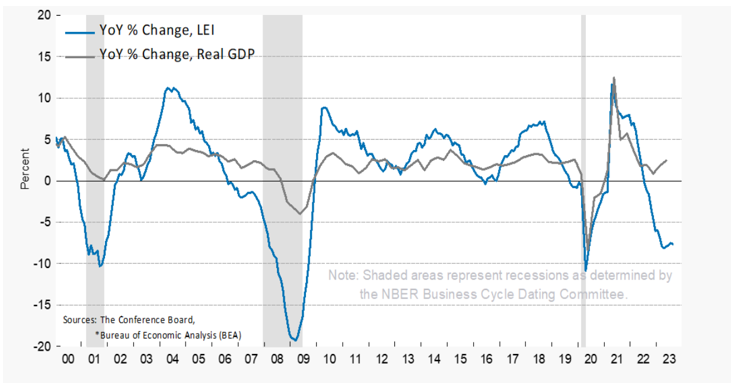

Are we then in a market filled with pathos in Niebuhrian terms? Pathos, according to Niebuhr, is constituted of capricious confusions/interactions between fortune and painful frustrations. There is no nobility in that market. However, Niebuhr can envision a case where a situation filled with pathos can form an element of beauty if resilience prevails over a downward spiral, especially when leading economic indicators point to a recession, as shown below. No wonder, then, that an internet search about current market resilience reveals thousands of related links.

If the contemporary market affirms an element of pathos, where is the tragic Niebuhrian element? When a universally accepted bad choice (keep raising rates) is consciously made for a greater good cause, this represents a tragic choice for the preservation of a higher purpose (offset inflationary pressures, finance higher deficit, dollar statecraft, to name a few of the higher purposes). Hence, the need to keep interest rate high for a longer period than originally anticipated. Tragic choices are made knowingly, and could subvert the aimed for higher purposes (growth, employment), hence the additional tragic element in those choices (like in the case of being forced to use nuclear weapons despite the fact that they may have been originally developed for the purpose of avoiding a mutual destruction). Adopting a tragic choice does not dissolve its tragic elements, it can rather multiply them as, quite often, they are inescapable, and the recognition of that can force actors to act imprudently.

If, then, we can accept that we could be in a tragic market filled with pathos, where does the ironic element fit? Niebuhr defines irony as: “Apparently fortuitous incongruities in life which are discovered, upon closer examination, to be not merely fortuitous. Incongruity as such is merely comic. It elicits laughter. This element of comedy is never completely eliminated from irony. But irony is something more than comedy. A comic situation is proved to be an ironic one if a hidden relation is discovered in the incongruity. If virtue becomes vice through some hidden defect in virtue; if strength becomes weakness because of the vanity to which strength may prompt the mighty man or nation; if security is transmuted into insecurity because too much reliance is placed upon it; if wisdom becomes folly because it does not know its own limits—in all such cases the situation is ironic.”

The hubristic geopolitical situation today is pathetically tragic, twisted by ironies. When market bubbles are created, the situation reflects nothing but irony formed and destined to have pathetically tragic consequences. If ironic situations are not recognized and dissolved quickly, then real tragedy could follow. That’s why it is important to recognize and dissolve bubbles and equally – if not more importantly – to contain ironic characters/leaders whose ironic actions, if not addressed and dissolved, could generate evil in the world.

We live in an era of identity crisis when faux redemptive narratives dominate debates. These faux redemptive narratives do not limit their appeal in the political, social, and geopolitical arenas. They extend to the market narratives.

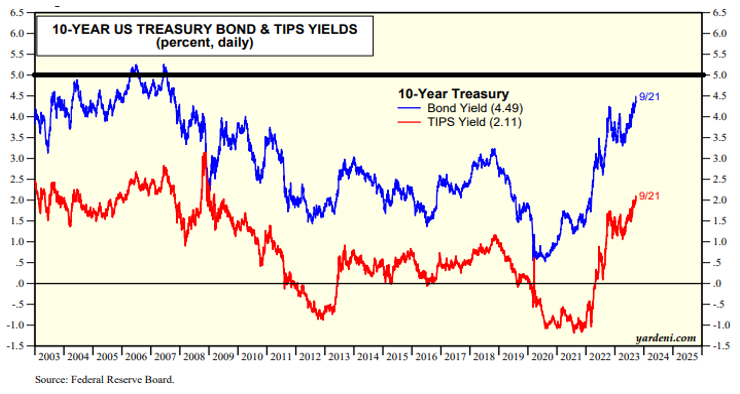

In the past few months, we have argued that the risk premium along with the yield on Treasuries are such that they make Treasuries attractive. The Fed leads the rate dance. The chances of another 25-bps hike in November are not low. Even the possibility for that keeps yields on an upward trajectory. We are of the opinion (expressed several months ago) that rates should/will remain high in 2024 and we also believe that any meaningful reduction may take place after May of 2024, unless clear signs of an economic slowdown materialize. The above constitutes one of the main reasons that we advocate for considering investments in 10-year Treasuries. The duration upside is attractive which could translate into good capital gains. Those who bought Treasuries when yields peaked prior to the financial crisis and held them until the end of 2008/early 2009 made a total return close to 60%. Of course, such investments should be made in stages.

Regarding the possibility of a recession in 2024, we give it a chance north of 35-40% as excess consumer savings becomes smaller, as corporate spending declines due to high rates, as debt consideration push yields higher, and as the latter take a significant bite out of discretionary spending. Of course, if recessionary risks rise, the possibility of lower rates becomes even higher which, in turn, translates into capital gains for 10-year Treasuries in a sooner time frame.

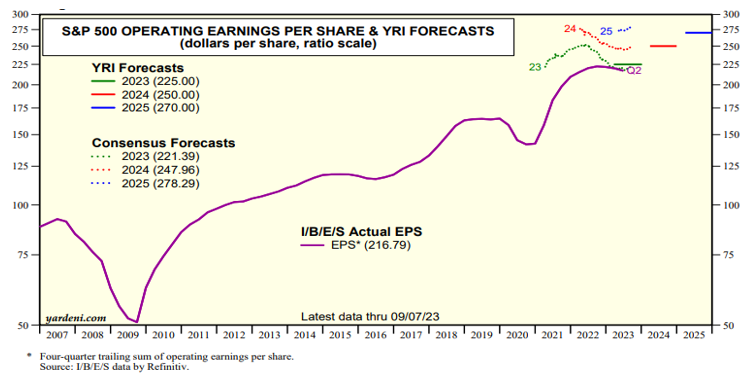

Since the end of July, a number of sectors have lost between 8-10% (materials, information technology, industrials, real estate). Could that continue? We may have a few more weeks of market turmoil, but the disinversion of the yield curve is good news that the market situation is improving, in the sense that the 10-year Treasury may be reverting back to levels seen in the pre-financial crisis of 2007-’09, while there is also an upward trend in the forward earnings for the rest of 2023, 2024, and for 2025, as shown below.

How certain can we be of market normalization as we assess the outlook? The only certainty might be the reality of human nature that requires redemption, as Niebuhr constantly keeps reminding us.