Ideological sclerotic politics can lead to tyranny. Adopting inflexible stands in an ever-changing market can lead to portfolio fragility. Ignoring the principle of prudence can inflict instability on both our portfolios and our politics. Edmund Burke could be considered an excellent example of one who excelled in the fields of politics and philosophy. Burke’s foresight regarding the just cause of the American Revolution, the fights he gave for the imperial abuses committed in India, his opposition against the oppression of Irish Catholics, and his deep understanding of the forthcoming terror following the French Revolution, are cornerstones of inspiration.

The current economic environment is marked by a few changing winds that can potentially create conditions where the ground resembles the picture of sinking sand. Specifically, in the West, we are facing a situation where rates can stay high for longer than expected, while inflation can turn out to be sticky. The combination of the two can squeeze spending and liquidity and, consequently, earnings. Moreover, and staying within the geographical perimeter of the West, while growth in the States is projected to be reasonably healthy given the current circumstances, the European economic picture is foggy with Germany facing significant headwinds.

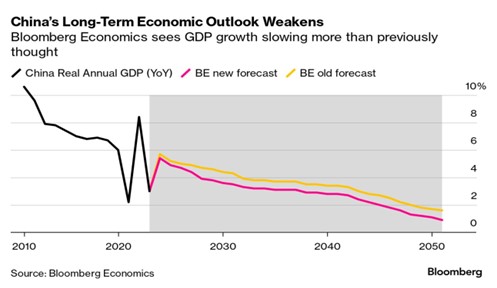

And while the European picture is challenging, the one in China keeps getting worse every week. Growth is slowing down, companies are defaulting on the debts and bond payments, major debt restructurings are underway, the real estate sector (which contributes close to 30% of Chinese growth) is shaky, youth unemployment is through the roof, and spending is declining as consumers are trying to build up their savings, while measures taken are half-baked and insufficient to revive growth. Analysts have started discussing the case of Chinese Japanification where for decades growth could remain stagnant.

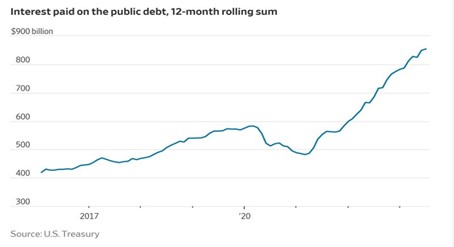

However, as previously discussed, the accumulated deficits make debt more expensive, especially at a time when rates are pretty high. Hence, as the graph below shows, paying close to $1 trillion for interest on debt necessarily becomes an impediment to growth and a disincentive to investors. High debt levels in the West, China, and Japan can derail growth and undermine earnings.

To the issues discussed above, we should add supply constraints and cost-push/energy pressures which, in turn, can serve the inflation cause and become a symptom of fragility that undermines investments.

When we read Edmund Burke’s writings, we are moved by his classical liberalism that espouses a moral, ordered, and regulated liberty that doesn’t deny the rights of anyone, but rather seeks to reconcile and preserve liberty with the primordial social contract, which, in turn, connects the living with the dead and with those who are following us and yet unborn. This is a virtuous partnership that upholds stability, avoids extremism, honors the past, and embraces change. Unfortunately, our politics have undermined that vision and, consequently, the headwinds we are describing, along with a gloomy and fragile economic picture, present a major challenge to the markets, despite the promises of rising stars such as India, along with good prospects in economies such as Brazil and Poland.

The latter three economies could be seriously considered in a portfolio that seeks to be reformed while adopting technological innovators without jumping on bandwagons that resemble ephemeral bubbles of innovators without substance and strong balance sheets. In that spirit then of Burke’s conservation while pursuing reform, portfolios could seek the safety of Treasuries that yield 4-5%, and experiment with rising economic stars as discussed above, while holding well-known names/anchors that are characterized by high margins, low debt, market leadership, solid sales growth, an abundance of cash, and consistently high returns on their invested capital.