James Cain’s book The Postman Always Rings Twice is an allegory of greed, passion, judgment, and even divine intervention. Frank (the novel’s main character) got away with murder the first time. However, the second time around he was wrongly convicted for murder.

Here are the facts of the global market nowadays: First, the emerging markets are expanding, especially the ones outside of the BRIC (Brazil, Russia, India, China) block. Indonesia’s and Turkey’s capital markets have experienced significant returns in the first seven months of this year. Second, yields on developing countries bonds are dropping as are their credit default swaps, signifying lower default risks and higher risk appetite. Third, Chinese growth is slowing down, while bubble indicators are picking up steam. Fourth, EU countries seem to be recovering without addressing their fundamental problems of overcollateralization. Fifth, The US economy is facing an “unusually uncertain” economic future. Sixth, markets and investors are looking for direction while corporate bond issuance reaches record highs of the last three years in the midst of declining risk premiums and corporate bond yields, making refinancing easier. Seventh, the Fed decided to keep the size of its balance sheet intact, suggesting that its financial stimulus will remain steady, while contemplating further expansion. Eighth, wheat and other agricultural commodities keep rising. Ninth, currencies and paper money of emerging economies are rising, showing potential and promises of growth and better returns. Tenth, hard assets in the form of precious metals are holding well despite fears of deflation.

Given that the Fed is the conductor in the current symphony, we are focusing this commentary to its latest announcement which we believe it resembles the postman who is preparing to ring the bell again.

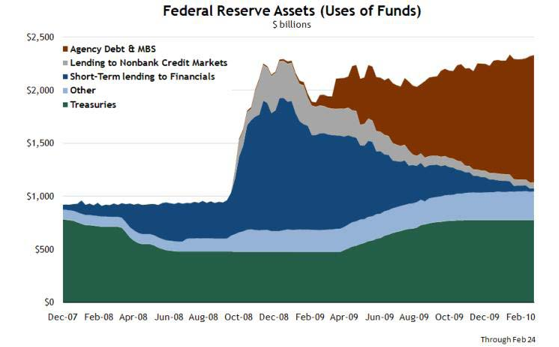

It was August 2007 when the Fed started its unprecedented actions of expanding its balance sheet from around $700 billion to over $2.3 trillion nowadays (see figure below, where the numbers have not changed since the February data shown below). Those moves may have spared the US and the global economy from a second depression – at least thus far – but have brought with them significant risks. The expectation was that the Fed’s programs would stimulate the economy. They did, but only temporarily. They put the economy on life support treating the symptoms while leaving the causes unaddressed. As we had predicted in our writings (see our newsletters since last September), the economy started showing signs of weakness this past spring, and since then the talk in town is about a double dip and deflation. At the same time, stimulus programs in the US, China, the EU and in other countries uplifted hopes for growth, for a V-type of economic recovery, making people believe that financial stimulation and credit extension would solve the problem. We are of the opinion that those programs are covering up the causes and postpone the needed surgery.

The Fed was expecting that as the paper assets that it had purchased matured, it would withdraw the electronic credits from the banking system and thus start shrinking its balance sheet. The Fed’s announcement however, this past Tuesday paints a different picture. It shows that it will keep recycling funds from matured paper and will be involved in further purchases of paper assets. The postman is preparing to ring the bell again, but we do not know yet if the second ringing will be for redemption or condemnation. It seems to us that the effort tries to add credibility to an irrational policy of credit extension without addressing collateral issues and foundations of this credit extension exercise.

We are of the opinion that markets can hold well for a few more months given these intentions and programs in what we believe is an exercise in futility. Emerging markets may continue performing better in that period too. They have done well primarily due to their exports; however, as hope is replaced by despair again down the road, especially when the Chinese situation starts sinking in. Investors will start looking for the exits again, contributing to declining exports and growth prospects. Thus, while emerging markets hold much hope, the uncertainty of the bell’s ringing may unleash a possible wrath on those who were warned that unless the boat has an anchor, it better not sail out in the open waters.

Ode to anchors!