According to the Fed’s recent announcement, the US central bank will start shrinking its balance sheet shortly, while we are expecting it to raise short-term rates in December. At the same time, we are also expecting the central bank of England to also raise rates in November, while the ECB is expected to reduce its bond purchasing program within the next few months.

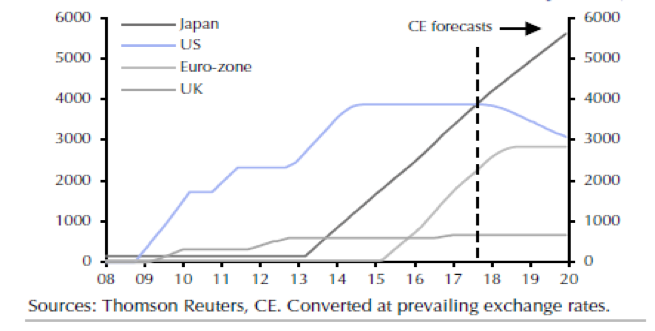

While the above may sound like that we are entering into a contractionary monetary period, the fact is that given the multiple rounds of quantitative easing (QE) around the globe since 2008, monetary policy will remain very accommodative and in an expansionary mode for years to come. The figure below shows that between the four major central banks the debasement of currencies will still be the main game in town well after 2020. On top of this, rates are expected to remain low, and therefore we believe that the planned actions by the central banks will not change the accommodative monetary landscape for years to come.

Moreover, we also need to recall that the central banks’ purchase of bonds soaked up the supply of good collateral in the market; therefore, as some limited normalization starts, the ratio between reserves and tradable stock of good collateral will improve which will also translate to higher liquidity in the market.

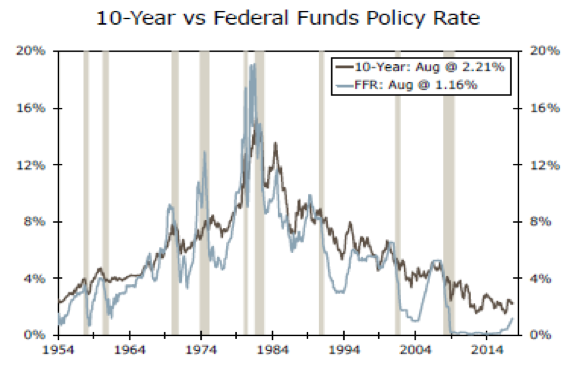

However, what we would like to point out is the following: While the traditional reliable predictor of recessions is the inversion of the yield curve, the fact remains that in the past it has recorded some inaccurate predictions. On the other hand, and as recent research by Wells Fargo indicates, a more reliable predictor for recessions is when the Federal Funds Rate (FFR) crosses the yield on the ten-year Treasuries, as the graph below demonstrates.

Therefore, as the blue line’s trajectory points to a possible crossing of the ten-year Treasury yield, we would caution investors especially as geopolitical developments are unfolding from North Korea, to Kurdistan, to Yemen, to Catalonia while the EU is struggling to find its new identity given Brexit talks and the recent German elections.