In the first part of this commentary, we examined two contrasting views of the market’s direction. The one describes a resilient economy. The other raises concerns about economic fundamentals that cannot justify significant equity exposure. As the commentary explained, those opposing views reminded us of the opposing positions and vision of two great leaders, Julius Caesar and Cato, whose conflict ended the age of the Roman Republic and ushered in the age of the Roman Empire. Our weekly series on Geopolitics and the Day After echoes another watershed moment in our trajectory.

In this second part, our focus will be on a key question at the core of investment committees, asset and wealth managers, as well as individual investors: Given the current metrics, is it justifiable and worthy of the underlying risks to have significant exposure to equity markets?

The death of Johann Sebastian Bach in 1750 manifested the end of the Baroque Period. The music that was created during that period had emotional content bounded by form and logic. It was grand but not pretentious. It reflected the cathedrals of that era that had majesty and were built on solid foundations. Improvisation could not be found neither in the cathedrals nor in the Baroque music of that era. With Bach’s death, a new era unfolded with the likes of Mozart, Haydn, and Beethoven. Bach’s fugues were masterworks of musical architecture that gave voice to those who followed him. He built cathedrals of sound where the mind reels at the composition. What is the “opposite” musical style to Bach’s musical structure? Could it be jazz, or could it be that Bach actually inspired that marvelous musical movement full of innovation that is grounded in the idea of liberation from our fears?

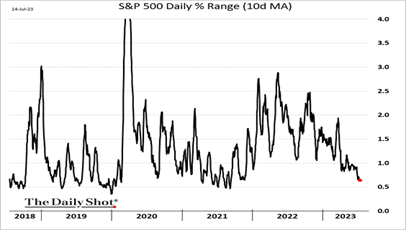

In our commentary last Tuesday, our argument was that because of very loose fiscal and monetary policies in the recent past, there is too much money in the system that sustains both the economy and the markets, while the fear of losing out in market upswings, along with expectations of lower rates in 2024, propels the markets to higher levels, which in turn shepherd an escort called complacency. The latter is partially reflected by low volatility and high rising demand for call options, as shown below.

When we take a look (over the last 50+ years) and compare the S&P 500 Earnings Yield (earnings divided by the stock price, i.e. the inverse of the P/E ratio) to the Treasuries’ yield, we can clearly see – as the figure below shows – that whether we are talking about the mid-1970s, the early 1980s, the early 1990s or 2000s, the historical record signifies that the stock market’s earnings yield – relative to the Treasuries – is pretty low and unattractive nowadays. This is true especially when we take into account the fact that breadth is narrow and valuations are stretched, and despite the fact that the Transportation Index started rising again (implying higher demand and rebuilding of inventories).

The low equity premium (difference between the return on equities and the yield on Treasuries) is an indication of excessive optimism and sentiment which eventually reverses itself.

The Catilinarian conspiracy/coup d’état in 63 BC was another turning point in history that marked the beginning of the animosity between Cicero and Julius Caesar, which eventually led to Caesar’s crossing the Rubicon, abolishing the Republic and ushering in the era of the Empire. When the conspirators of Lucius Catiline were found and brought before the Senate, the Senate’s rising stars took opposing stands. Julius Caesar advocated for a trial before execution, a right of all Roman citizens. It seemed that Caesar’s position would prevail until Cato stood up: “Wake up, before it is too late…We are surrounded on all sides. Catiline and his army press at our throats. There are enemies within the walls and even in the heart of our city…You may prosecute other crimes after they have been committed. But if you do not stop this one from happening, once it does take place, you will appeal to the courts in vain. In a captured city, there is nothing left for the vanquished.” That was it. Dead silence prevailed in the Senate. Cicero stood up and called for a vote to execute the conspirators. Cato and Cicero carried the day. Caesar’s proposal had been crushed and later he was accused of being a conspirator himself, nurturing the ground for the Dreyfus case in 1894.

On numerous occasions, Caesar wrote and sought reconciliation with Cicero, but Cicero never reciprocated. On the contrary, he denounced Caesar as “the prince of scoundrels”, “a wretched madman” who has “never seen the shadow of honor and right.” Caesar was urging Cicero not to take sides between him and Pompey, but Cicero was unmoved. Caesar’s ultimate military battle was with Pompey whom he defeated and in magnanimity pardoned all his supporters. Prior to that Caesar wrote: “I made up my mind to act with the greatest moderation and do my best to bring about a reconciliation with Pompey. Let us see if in this way we can win all hearts and secure a lasting victory. It is a new way of conquering, to use compassion and generosity as our defenses.”

Reflecting on Caesar’s writings and with regards to the opposing views on the market trajectory, could it be wise to reconcile by having some equity exposure but refraining from high stakes given the Treasuries’ yield and the abnormal circumstances?”After all, Bach ushered in the age of jazz as Ward Swingle and his extraordinary French singers have demonstrated over the years by reconciling Bach and swing, demonstrating Bach’s music’s remarkable ability to adapt to all ages and styles of play, and not only survive but also gain in stature.

I hope you can enjoy these videos (recorded in 2009 in All Saints Church in Braunston and in 1969 for Croatian TV) as much as I did.

Les Swingers Singers J S Bach Fugue in D Major 1969 – YouTube