The actual data for 2023 turned out to be better than the projections. If those trends continue in 2024, then optimism should underline the New Year. Despite fighting a pandemic since 2020, significant supply chain turmoil, inflationary pressures, high interest rates, and wars, the international economy has exhibited good strength even though a recession was widely expected in 2023.

The combination of rosy expectations (from lower inflation and interest rates to continuous growth; and from healthy profit margins to high levels of employment), the anticipated productivity jump (for the next few years) from the wider adoption of artificial intelligence (AI), and the positive climate inherited from 2023, has created an optimistic atmosphere despite the fact that major economies such as Germany, China, and the UK are still facing tremors. However, and despite the challenges of those major economies, the star of others is rising, such as those of India, Vietnam, Brazil, Poland, and Mexico.

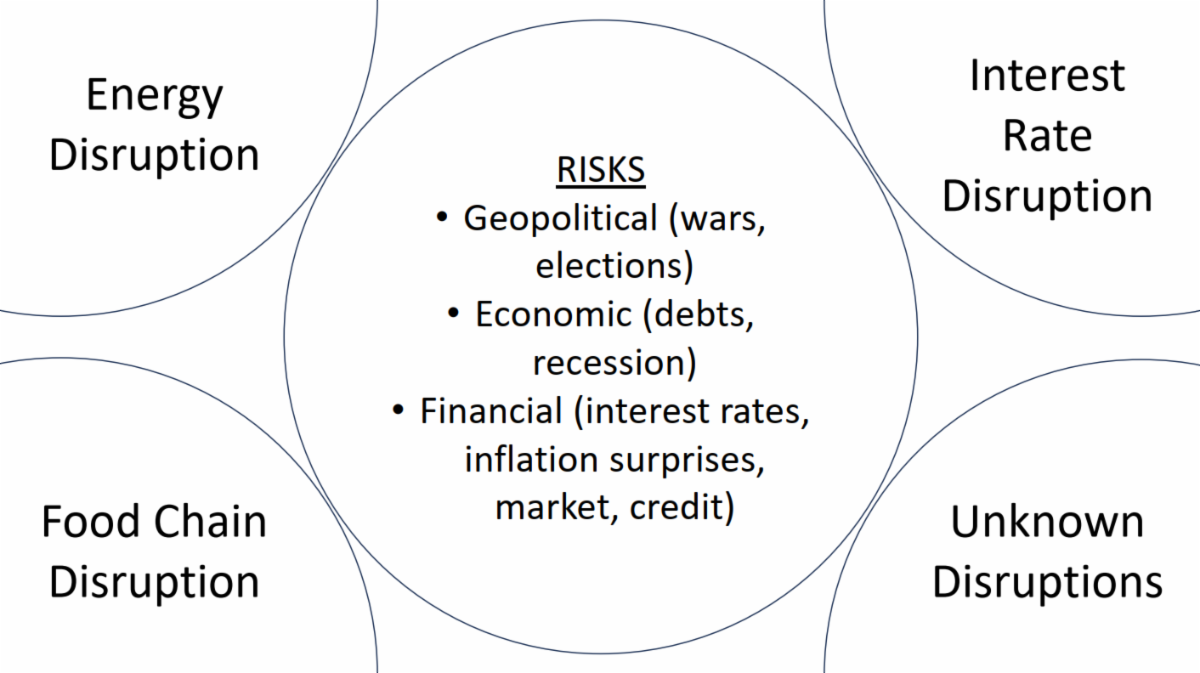

Looking ahead and given the discussion above, we choose to be cautious and assess the economic and financial conditions on an ongoing frequent basis because complacency is always dangerous, given the risks as presented in the schematic below.

Overall, our cautious stance would imply a main focus on income-seeking securities, while having some exposure to technology and to value-oriented securities. The main risks that we see in 2024 are geopolitical, economic, and financial (see schematic above). However, within the framework of risk assessment, we should also consider the four corners of potential choking points that could disrupt economic and financial prospects and derail expectations.

As shown above, energy disruption is a fundamental choking point, because if it were to take place, then economic and financial risks would materialize. Against such a potential choking point, some exposure to energy may be warranted.

The second potential choking point is the overnight/repo market which, in the past, exhibited major volatility at times when debt markets faced challenges. Such a choking point can occur due to a confluence of reasons, such as low levels of reserves, large Treasury issuances, or a major default (something we witnessed last March). When any of the underlying causes takes place, then the overnight repo rate could spike to high levels, as short-term financing becomes scarce. Back in 2019, the repo rate went from less than 2.5% to as high as 10%. Central banks have shown skills in managing such spikes, however if such a spike coincides with the emergence of another major risk (e.g. geopolitical), then the return to stable repo rates might be problematic. Against such a possibility, some exposure to gold may be wise.

The third potential choking point is a major disruption in the food-supply chain. In the back of our minds, there is the real probability of a major food crisis in the next 10 years. However, that does not exclude the possibility that the food-supply chain can exhibit disruptions (as we witnessed in 2022). Against such a possibility, some exposure to grains (or their futures) might not be a bad idea.

Finally, and given the fact that we do not adopt deterministic models of projections, but rather stochastic ones that leave room for error, we should dedicate the lower right corner of our assessment to that unknown choking point that could emerge and disrupt economies and markets. Against such a possibility, we recommend cash (in the form of Treasury Bills). At the same time, it should be noted that the emergence of any of the choking disruption points mentioned above could unravel the realization of risks and turn things quickly upside down while volatility would spike too.

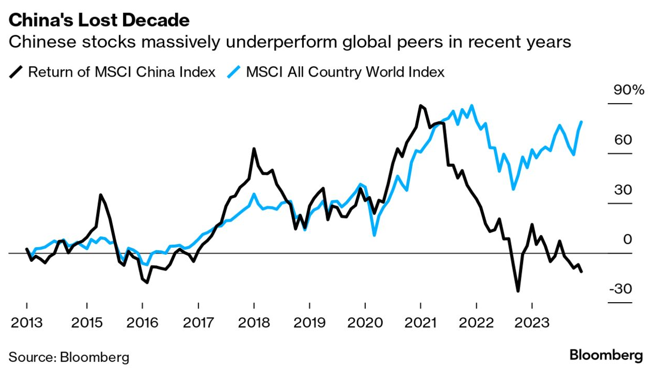

In such an environment, we should pause and reflect on China’s rising star. More than 10 years ago we circulated a post exposing that rise to great amounts of debts that sooner or later could unravel. That Chinese Great Wall of Steroids (debts) could undermine internal cohesion and social stability, while an uncontrolled implosion would have global consequences. After all, if someone had invested in a Chinese ETF 10 years ago, today they would have to show losses for such an investment, as shown below.

Happy New Year!