It is possible that last year marked a pivot in the markets’ trajectory that is being shaped by too much debt facilitated mainly by central banks, geopolitical risks, the deflating of paper-asset prices, the collapse of cryptocurrencies, the limited rising of opposition against authoritarianism (such as in Iran and China), and the pursuit of new asset classes? How then can we summarize the major investment lessons from 2022, and what could be the initial assessment for 2023?

- Transitory inflation is a myth. Inflation undermines financial stability. Growing money supply chasing a shrinking supply of goods and services always produces inflation, which should be anticipated, and precautionary measures (such as raising rates before the first inflationary signs appear) should be taken, if a soft landing is desirable.

- Corporate pre-emptying should be expected in the form of higher prices, as well as demand for higher wages, both of which, in turn, exacerbate inflationary pressures.

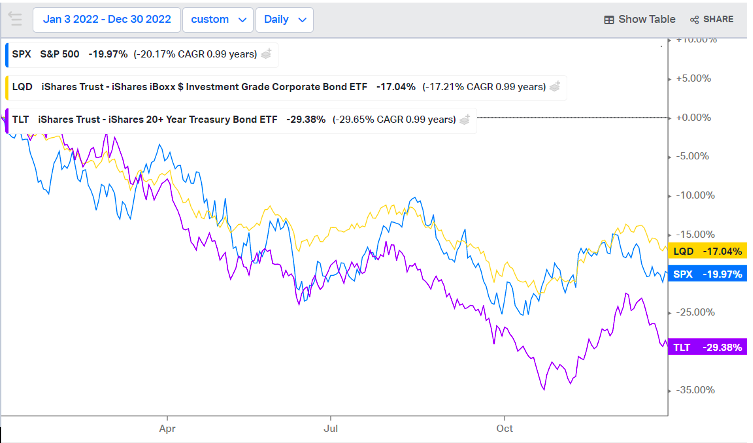

- Holding long-duration bonds in such an environment could be lethal. Fear of lower future profitability (due to rising rates) punishes stocks, and especially tech-related stocks. Government long-term bonds lost close to 30% and investment-grade bonds lost 17% (see graph below), while the S&P 500 lost almost 20% (the Nasdaq lost 33%).

- Geopolitical conflict should be a determinant factor in market assessment and in factoring projected earnings. The war in Ukraine is an excellent example. Sectors that could benefit from geopolitical turmoil should be incorporated into portfolios.

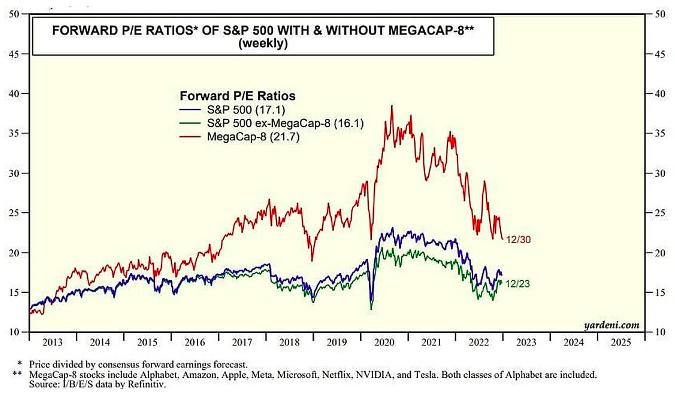

- Exponential gains not grounded on strong fundamentals will lead to significant corrections, whether we are dealing with Tesla, Bitcoin, or Amazon. The fact is that those megacorps/megacaps (Alphabet, Apple, Microsoft, Meta, Netflix, Tesla, and NVIDIA) reached a forward P/E ratio of 38.5 during the pandemic. Such high P/Es (even for well-established companies such as Alphabet and Microsoft) are susceptible to dramatic drops. Indeed, those megacap-8 (as they are known) experienced a capitalization drop by more than 40% in 2022, and investors lost $5 trillion (see graph below).

- And now, as we make our transition from the lessons learned to expectations for 2023, let us state that while some net-zero goals might be unrealistic, the fact is that climate change is taking place, and there is collaboration between governments and the private sector in fighting it. Consequently, a new asset class is under formation (for both official and voluntary carbon markets). Carbon prices are rising, as shown below.

Most certainly we could have discussed additional lessons and it is possible we may have missed significant ones regarding portfolio management. However, having 2022 behind us, we believe that we ought to outline some well-grounded expectations for 2023. Needless to say, such expectations are being shaped by unfolding events and therefore, they are subject to change.

- A recession is anticipated for both the US and the EU, while inflationary pressures should moderate. The EU is in a much worse position than the US which might be able to avoid a hard landing if a number of factors alter the headwinds in front of us. Consequently, sales and profits would decline, unemployment will rise, business and consumer confidence will decline, production and possible capital spending will slow down, and the equity markets may have further to decline.

- Rising geopolitical risks present a significant threat to stability. Therefore, sectors that benefit from such instability should be enhanced in the portfolios.

- Given the above two points and the losses that US Treasuries experienced in 2022, it would be worthwhile exploring adding to the portfolios Treasuries of longer then 12-months maturity, especially when clouds start becoming darker. We remain cautious of high yield due to rising risks and uncertainties that could snowball if a major negative event takes place.

- Some dividend-related funds performed well relative to the S&P 500. That outperformance may continue in 2023.

- Rising instability and volatility could also imply good entry points (on a dollar-cost-average basis) in particular sectors (or in the market as a whole), such as semi-conductors, however it would be wise if the overall stance (for now) is pretty conservative and defensive.

- While the grand majority of analysts expect dollar weakness (something normal after the 2022 gains), there are three factors that make us question the admittedly sound reasoning behind such belief: First, rising economic/financial/geopolitical risks. Second, interest rate differentials in favor of the US. Third, the political understanding that a strong dollar opens us the highways of capital attraction, purchasing power, and geopolitical strength.

- The overall environment seems to be conducive to commodities (oil, grains, precious metals) and structured notes that pay double digit interest (prefer to be tied to indexes – rather than individual names – and have a barrier of at least 30%).

We shall revert to the topic as the weeks are progressing and the markets are looking for direction.

And because we cannot live by bread alone:

“Even in our sleep, pain which cannot forget

Falls drop by drop upon the heart,

Until in our own despair.

Against our will,

Comes wisdom

Through the awful grace of God.”

-In Aeschylus’s play Agamemnon