A few days ago the IMF published its annual forecasts for developed and emerging economies. Five things are worth pointing out:

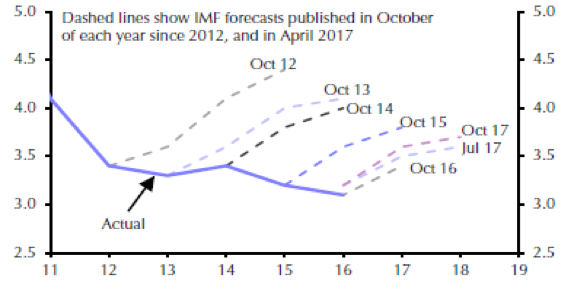

- First, when we review forecasts made for previous years it becomes obvious that the IMF is overestimating growth potential.

- Second, regarding China we believe that the IMF’s forecast underestimates the great wall of steroids (a.k.a. huge debt and NPLs) and the possible effects on global growth for developed and emerging economies if the debt bubble in China starts to burst.

- Third, the Brexit impact and the lack of coherent leadership in the United Kingdom will start having a significant effect on the UK economy in 2018.

- Fourth, a possible messy Brexit in association with political turmoil in the EU (Catalonia, Italy) and Russian mingling/claims from the Black Sea to Syria (always with the purpose of getting access to the warm waters of the Mediterranean) could elevate risk levels and reduce capital investment spending.

- Fifth, potential incomprehensible policies by the US could generate waves of uncertainty which in relation to the overvalued markets could unleash fear and profit-taking, which in turn could undermine growth.

The graph below shows the IMF’s forecasts (the dotted lines) in previous years and the actual growth rate for developed economies. The discrepancies are obvious.

Source: Capital Economics

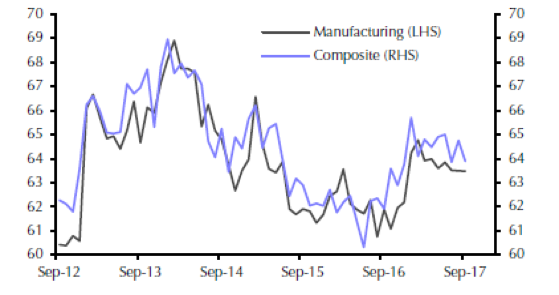

In addition, when we take into account the global PMI (Purchasing Managers Index) projections –as shown below – we could say that while growth may be stabilizing, the purchasing managers are cautious regarding their expectations.

Source: Markit, Thomson Reuters

Therefore, as we enter the last quarter of 2017 and begin thinking of 2018, it might be wise to take a more conservative approach to asset classes and portfolio holdings, while also deploying some hedging tools that could protect the downside of the portfolio.