Many commentators have been discussing lately the similarities between the 1970s and the inflationary pressures of today. Others have expanded their analysis by incorporating stagflationary issues into their comments. We certainly can see some similarities to the 1970s, but we humbly believe that a crucial element is missing: Fundamental changes to monetary regimes stimulated by debt accumulation and balance of power dynamics.

A brief historical perspective might be useful:

Stage I: Just before WWII ended, the geopolitical and balance of power dynamics necessitated the establishment of a new international monetary regime. Bretton Woods established the dollar as the international reserve currency. National currencies were tied to the dollar in a fixed exchange rate regime, while the dollar was fixed to gold prices. Therefore, indirectly and via the dollar, foreign exchange rates were linked to a fixed gold price.

Stage II: As the engine of finance (a.k.a. war) was re-engineered in the 1950s, 1960s, and early 1970s (Korean, Vietnam, Cold Wars), the money supply was increasing significantly. More money circulated implied a lower value for the dollar along with higher debts. Moreover, countries like Saudi Arabia were receiving inflated dollars. Welcome to the oil crisis of the early 1970s.

Stage III: The Bretton Woods fixed exchange rate regime could not hold. The dollar was delinked from gold and a new monetary regime was engineered. Mistakes of allowing the Monetary Base (MB= currency + reserves) to leak into actual/circulated Money Supply (MS) continued throughout the 1970s, and, consequently, financial instability along with geopolitical tensions continued rising. Such instability ended with the strong leadership of Volcker whose monetary regime and legacy created the background for the prosperity of the last 40 years.

However, before we endeavor in explaining as briefly as possible the argument for monetary regime change and disintermediation, it might be useful to perform a form of diagnostics on the causes of the market turmoil, especially after yesterday’s debacle that followed a day of strong gains on Tuesday. How does the above relate to the developments we have been experiencing?

- As we have explained before (see indicative commentaries here, here, and here) the root cause of the financial crisis that started in the summer of 2007 was the explosion of the derivatives structure which exceeded $700 trillion by 2007.

- The monetary regime instituted in the early 2000s depended on asset collateralization and rehypothecation (see indicative commentary here) which, in turn, created a chain of credit extensions.

- Credit extensions that increase the Monetary Base (MB) without increasing significantly the Money Supply (MS), do not result in inflationary pressures. That was the experience of Quantitative Easing (QEs) in the 2010s (i.e., the MB increased in an unprecedented way without inflationary pressures).

- When the central banks allow the increases in the MB to leak and become actual increases in MS, as they have been doing since 2020, we cannot expect anything but inflation.

- When inflation materializes (especially after pronouncements of transitory nonsense), valuations decrease which in turn reduces the velocity of the collateralization chain.

- When action is finally taken to combat inflation (policies of raising rates and/or credit tightening), then fears of recession emerge, which, in turn, could expand the credit spreads, raise costs, and produce a hard landing in asset classes and/or the economy itself.

- Market dislocations take place when one or two of the above elements are energized by supply constraints but also by rising geopolitical tensions and/or when parties start questioning the collateral base (or even the actual existence of the collateral itself, see here).

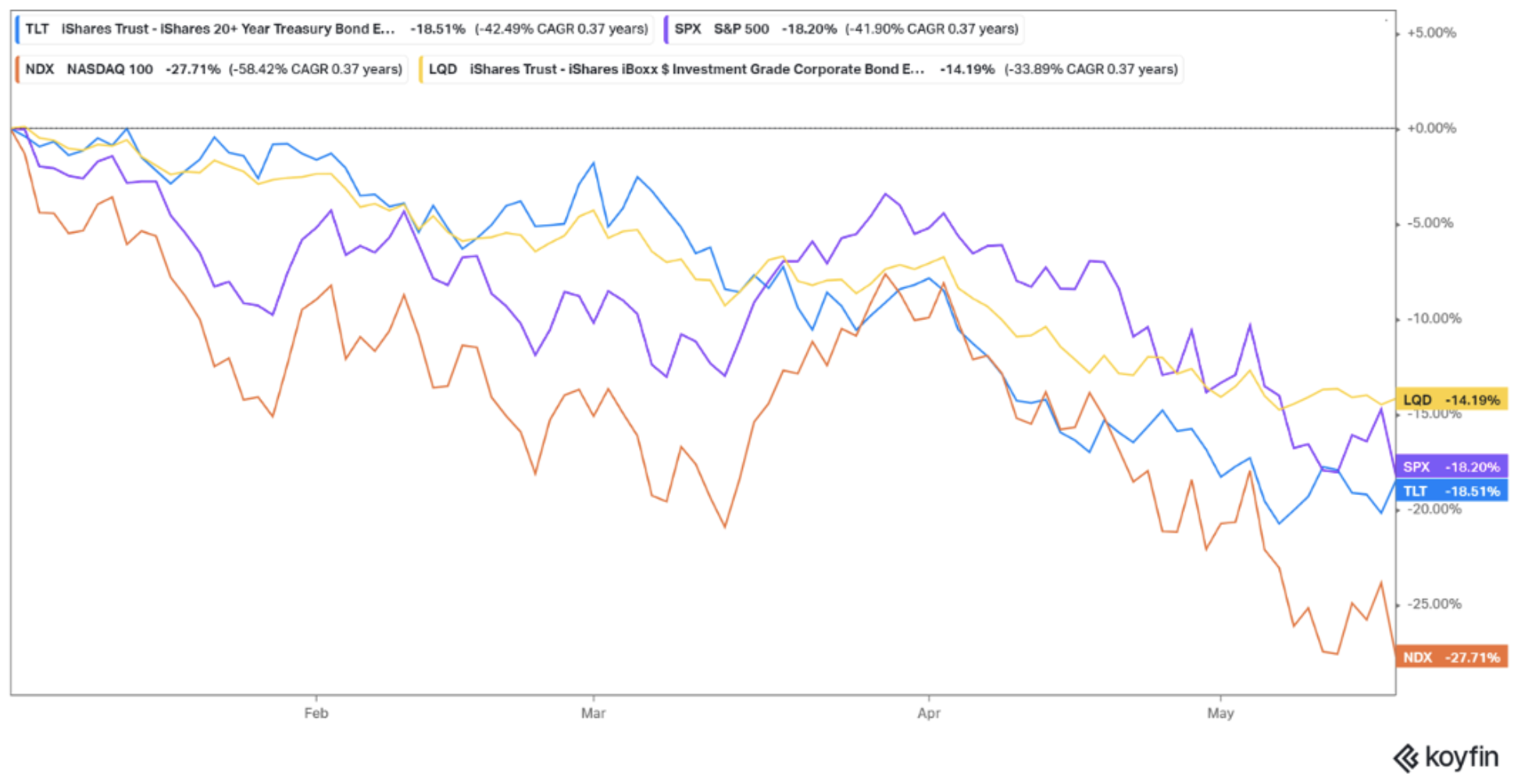

- Market capitulation can occur if perceptions of shocks/crashes register in the behavior of traders or algorithmic programs. As a result, the Nasdaq is past bear territory (having lost almost 28% since the beginning of the year), the S&P 500 is pretty close to bear territory (having lost a bit more than 18%), long-term government bonds are also registering losses of 18%, while investment-grade corporate bonds have lost 14%, as shown below.

So, in a nutshell, a number of factors have joined forces to result in a market downturn. Do we panic? Of course not! Do we jump from the train because it goes through a dark tunnel? Again, the answer is, of course not! As long as the portfolio has solid companies and cash, the opportunities will present themselves to buy more at lower prices. After all, we do not sell our homes because of a bad real estate market. The market will recover as it does all the time, so the focus at this stage is cautious capital management.

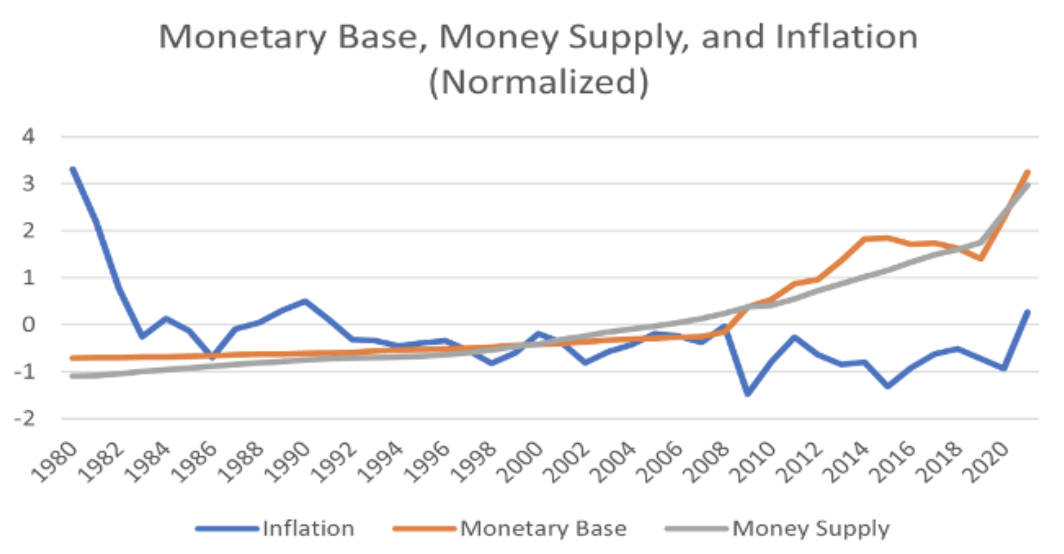

Here is a graph that portrays our argument (the graph has been normalized given that MB and MS are measured in the hundreds of billions while inflation is a single-digit number).

As the graph shows, as long as the increases in the MB are not translated into proportional increases in MS, inflation remains stable. However, the 2020-’21 exponential rise in MS after the QEs and the fiscal stimuli caused a significant rise in the inflation rate.

But let’s now revert to the issue of monetary regime and financial disintermediation. Monetary regimes that do not adhere to actual anchors (or when the anchors are manipulated/cheated like in the case of Britain in the beginning of the 20th century, or in the case of the US in the 1960s) come with an expiration date. Bretton Woods lasted almost 40 years, and since then we are on a fiat monetary regime. The financial crisis of 2007-’09 instigated the need for a new regime. It’s not a coincidence that in the period since then, alternative payment systems have been developed along with alternative/digital currencies. Like in the case of the 1970s, it takes time for the new system to grow, mature, and register in the habits of institutions, consumers, and investors.

The rising inflation in the 1970s pushed a financial innovation which we know by the name of Money Markets Funds (MMFs). The latter started paying interest rates well above what the regulatory environment allowed (due to the fact that money was invested in government bonds whose yield was much higher than the rate paid in savings accounts). Banks, then, started feeling pressures as capital was flying to MMFs, so they got inventive and developed Money Market Deposit Accounts (MMDAs) which paid interest well above the savings accounts. The financial innovation along with the monetary regime change instituted a market that still thrives to this day.

We are marching toward a New Day where alternative payment systems, alternative/digital assets and currencies, new asset classes (think of carbon markets and the tokenization of carbon credits a market which could be over $4 trillion by 2030 and over $20 trillion by 2050), and a new balance of power (with the US in a role of a hyperpower and China in a role of superpower) will institute a new global monetary and geopolitical regime. In that transition period, downturns and even erratic markets will be part of the something we all have experienced before: Growing pains.