When we compare equity and oil markets over the course of the last four years it is easy to see that markets in the US are reaching record highs while oil prices are reaching record lows. Obviously, the Fed’s intervention has been a catalyst for the markets’ performance and the accompanying financial repression with zero-bound interest rates. We anticipate that the swing from quantitative easing to reverse repos in US monetary policy – at a time when the EU and Japan follow a path of quantitative easing – will result in waves of instability characterized by short periods of credit and liquidity freezes. This in turn will be followed by market upswings until a plateau is reached due to the fact that the marginal efficiency of central authorities intervention reached a level of entropy. Therefore, if there were to be a conclusion out of this commentary it would be that markets swings are expected that would resemble the game of musical chairs, until the music ceases for good.

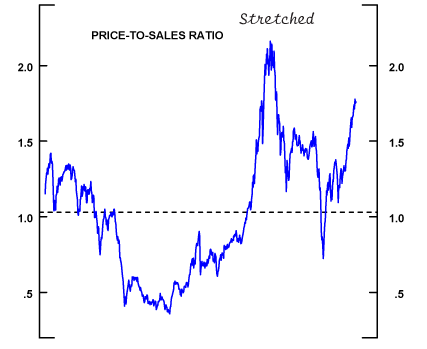

In this environment the combination of fundamental and technical analysis will prove to be pivotal for the realization of profits. We would not be surprised – given the recent narrow trading range – if the markets go into reverse for a short period of time, demonstrating once again that liquidity is the key. In this environment, if we look at the price-to-sales ratio, we will observe that it has started reaching stretched levels, i.e. searching for a resting period.

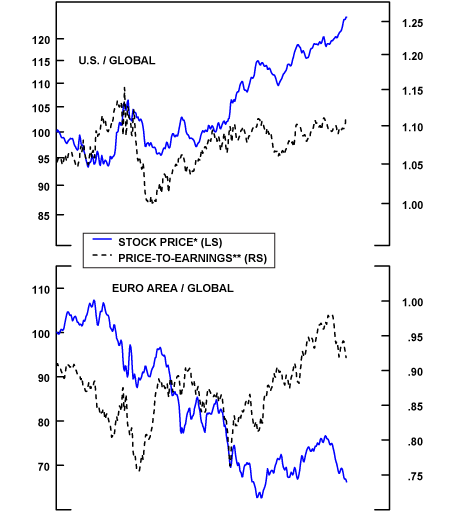

At the same time, the discrepancy/divergence that has developed in the last year between the US and EU markets calls for some convergence. As the graph below shows, the US vs. the global markets has followed an upward trend, while the EU has followed exactly the opposite.

We are of the opinion that in 2015 some convergence will take place between US and EU equity markets’ performance, mainly due to the ECB’s measures of “asset” buying that will weaken the Euro against the dollar. At the same time Chinese markets –due also to some liquidity infusions as well as some institutional changes – and possibly the Japanese markets too will perform relatively well, adding to the atmosphere of optimism that celebrates prosperity bought on credit.

In the midst of these expected developments – waves of volatility, credit freezes, liquidity constraints, and market upswings – when someone asks where the engine of growth (productivity) can be found, he is told in government spending and the central banks’ balance sheets!

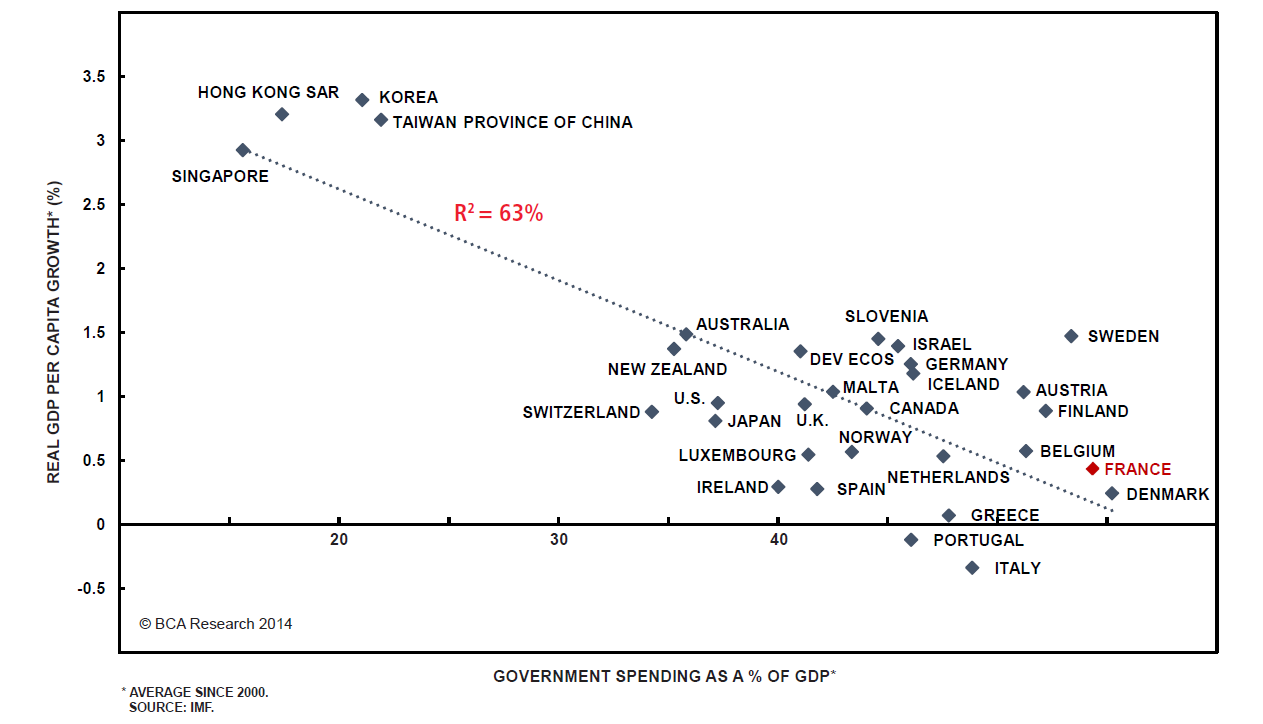

With all due respect to this idiotic rationale, we offer some facts as concluding comments: Productivity growth rate on an annualized basis is pretty dismal at 0.9%. Unless productivity growth rate picks up, growth will decline while debts are rising. Now, as for growth and government spending, the following graph is self-explanatory.

Welcome to the era of delusional rationale where placebo treatments are reserved for those that believe that the long-term prosperity of a nation depends on its ability to enlarge the government and to print more money.