We’re pleased to announce that the Fundamental Analytics Carbon Services website is now live—explore insights and tools driving carbon compliance and market access here.

The FACS platform, linked to ICE, enables direct EUA trading and streamlined onboarding for CBAM-affected markets.

Welcome to our monthly newsletter, Carbon Market News Roundup, the goal of which is to introduce our audience to a new asset class market in the making: the carbon market. Our previous issues, along with the rest of our commentaries, may be read here.

EU ETS & CBAM

Methodology for the definitive period starting on 1 January 2026

EU Commission

Adjustment of obligation to surrender them to take account of free ETS allowances

carbon price paid in a third country

EU Commission

Carbon price paid in a third country

EU Commission

EU to publish key CBAM rules, methodology clarity in Q4

Carbon Pulse

The European Commission closed August by launching consultations for the definitive CBAM phase (effective January 1, 2026). The package seeks feedback on the methodology to calculate embedded emissions – direct, indirect, and electricity-related – with default values where actuals are unavailable, how to adjust CBAM surrender obligations to mirror the phase-down of free EU ETS allowances, and how to recognize carbon prices paid in third countries and convert them into fewer CBAM certificates. Final measures are signposted for Q4 2025. In parallel, fresh analysis highlighted distributional impacts for developing-country exporters, showing how choices on defaults and recognition rules will shape both trade flows and compliance costs. Step by step, the definitive phase of CBAM is taking shape.

EU carbon allowance prices were steady through the summer: in July, EUAs hovered in the €70s/t, and in August, they held around €72/t, edging higher but still in a tight range. Desks cited muted industrial demand, renewables output, auction supply, and the seasonal power stack as key near-term drivers. With the first maritime ETS surrender due at the end of September, several analysts had anticipated a steeper pre-surrender bid. So far, that additional compliance demand is visible but not yet forceful enough to break the range.

Maritime & Shipping Updates

Expansion of the Emissions Trading Scheme (“UK ETS”) to the maritime sector

Simone Vitzthum, Skuld

First EU ETS shipping payment due 30 Sept

Drewry

US to retaliate against IMO members that back net zero emissions plan

Lisa Baertlein, Valerie Volcovici and Enes Tunagur, Reuters

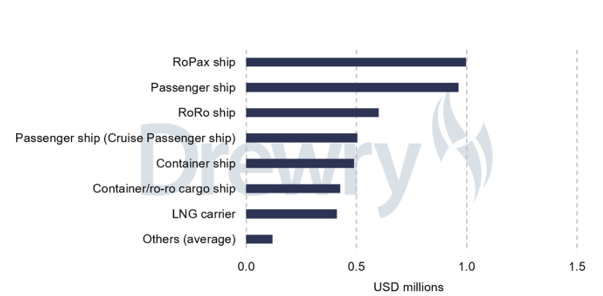

With the first EU maritime ETS surrender due by September 30th, shipping companies accelerated EUA procurement through August—shifting from “test” volumes to more programmatic buying as operators locked coverage and finalized registry logistics. Sector estimates put the 2024 compliance bill near $2.9 billion at ~€70/t, based on ~90 Mt CO₂ reported under EU MRV (a ~14% y/y increase, partly from Suez rerouting via the Cape). On average, RoPax/passenger vessels ~$1 m and container ships ~$0.5 m per vessel for 2024 exposure, with total costs potentially rising toward $7.5 billion once phase-in ends. At the global level, the UN/IMO levy adopted earlier this year continues to shape 2025 planning – expected to sit alongside Europe’s ETS later in the decade – intensifying calls to coordinate regimes and avoid fragmented obligations.

The UK confirmed maritime entry to the UK ETS from July 1, 2026, with scope mirroring EU design in key areas but adding methane and nitrous oxide. MRV will require one emissions monitoring plan per operator, while compliance dates will align with broader UK ETS timelines. In parallel, Brussels moved to link the EU and UK ETS, proposing dynamic alignment on cap/trajectory, sectoral scope, financial-market rules, mutual recognition of allowances, and potential mutual CBAM exemptions. Geopolitically, the U.S. signaled opposition to the IMO’s net-zero framework and warned of possible countermeasures, adding uncertainty just as owners and charterers prepare for overlapping EU, UK, and global carbon obligations.

Voluntary Market & Emerging Compliance Markets

Carbon credit ratings and market news: Price trends and anomalies

Fastmarkets

Are Nature-Based Solutions and Blockchain the Future of Carbon Credits?

Saptakee S, Carbon Credits

Brazil exercising additional year for ETS regulation

Carbon Pulse

In the voluntary market, quality is increasingly priced. Data show roughly ~50% price steps per rating band for REDD+, while project-specific factors still move prices. The first nature-based CCP-certified credits are testing appetite for explicit quality premia around $30/t; even without clear uplifts, more RFPs now require CCP tags or exclude non-certified credits, implying discounts ahead for surplus, non-CCP supply. Looking forward, growth narratives span nature-based solutions and technology removals, with blockchain-enabled tracking gaining ground to improve transparency and prevent double issuance. These are promising tools, but secondary to the immediate tasks of credible MRV, insuranceable risk, and consistent recognition across compliance regimes.

Brazil extended the regulatory phase of its national ETS to December 2026, prioritizing rule-writing and market plumbing over an early launch ahead of COP30. In Europe, Commission-backed analysis revealed the scale of the removals challenge: reaching net zero by 2050 implies an annual removals volume >350x today’s global total—a signal that integrity, accounting, and supply pathways will dominate the next phase of EU climate policy. In aviation, Verra/Gold Standard’s CORSIA insurance criteria landed, a potential unlock for supply. Early forward offtakes at $15–16/t versus $22–23 spot suggest buyers anticipate more eligible credits, even as insurance capacity could become the new bottleneck.

Recommended Reads

EU will not change methane regulation but there is some flexibility, official says

Reuters

Carbon markets updates: sustainable investing, S2 disclosures, soil carbon credits

Sam Carew and Fastmarket team, Fastmarket

DevvStream Bets $10M on Bitcoin and Solana to Reinvent Carbon Credit Markets

Jennifer L, Carbon Credits

3 climate misconceptions that add to noise over energy and net zero

Paul Mottram, SCMP