November 7, 2025 | Volume II, Issue 10 | The FACS Team

Welcome to the November edition of the Carbon Market News Roundup, our monthly briefing on the evolving landscape of global carbon markets and climate-related regulation. Our previous issues, along with the rest of our commentaries, may be read here.

In this month’s issue, we examine the latest regulatory and market developments shaping compliance systems across Europe and beyond. From the EU’s updated CBAM framework and forthcoming ETS2 price stabilization measures, to the collapse of the IMO’s landmark shipping emissions deal, policy momentum continues to define the trajectory of decarbonization across trade and transport. We also explore the rapid rise of new carbon market frameworks in Indonesia, South Africa, and Nigeria, which show how emerging economies are aligning domestic mechanisms with the Paris Agreement’s Article 6.

This edition introduces a new Country-Specific CBAM Exposure section, beginning with an in-depth look at Egypt, the most exposed MENA economy under the EU’s carbon border mechanism. The analysis assesses sectoral vulnerabilities, trade implications, and pathways for transition as CBAM reshapes global industrial competitiveness.

EU ETS – Regulations Updates

Regulation (EU) 2025/2083 of the European Parliament and of the Council

European Parliament

Germany insists on excluding international credits from EU ETS

Carbon Pulse

Germany pushes for delay of free carbon allowance phaseout, extension of EU ETS cap

Carbon Pulse

EU plans support for countries affected by carbon border levy

Kate Abnett, Reuters

EU Floats Measures to Restrict Prices in New Carbon Market

John Aigner and Ewa Krukowska, Bloomberg

EUA prices closed at €81.49 on November 5, down 1.0% on the day but still marking a 3.5% gain over the past month and a 27.8% increase year-on-year. The market began November with renewed strength, breaking above the €80 mark for the first time since January. The rally has been driven by colder weather forecasts triggering additional utility hedging and stronger compliance demand ahead of year-end surrender deadlines. A breakout from the €83.82 level would return EUAs to the late-2023 price range.

Source: Trading Economics

The EU has formally adopted Regulation (EU) 2025/2083, amending the Carbon Border Adjustment Mechanism (CBAM) to simplify and strengthen it ahead of full implementation in 2026, introducing a 50-tonne import threshold exempting small traders while still covering 99% of embedded emissions, shifting the annual declaration deadline to 30 September, enhancing customs enforcement, and linking CBAM certificate prices to the EU ETS from February 2027. Secondary rules on benchmarks and verification remain pending, but the reform signals a move toward proportionality and operational readiness. Meanwhile, Germany has rejected Poland’s call to admit international credits from Article 6 of the Paris Agreement into the ETS and is pushing to delay the phase-out of free allowances beyond 2039 until CBAM proves stable. To mitigate external frictions, the Commission plans to mobilize €200 billion under the Global Europe program (2028–2034) to support developing countries affected by CBAM, while also preparing to tighten price controls in ETS2 for buildings and transport by expanding the reserve and doubling the number of extra permits available if prices exceed €45.

Maritime & Shipping Updates

Landmark global shipping deal abandoned under US threats

Esme Stallard, BBC

Analysis: Shipping climate plan delay could sink clean fuel projects

Angeli Mehta, Reuters

Carbon Pulse

Industry groups urge EU to prioritise zero-carbon ship and plane tech, warn of policy gaps

Carbon Pulse

Hopes for a landmark global shipping emissions deal collapsed in London after the United States and Saudi Arabia led a successful push to suspend International Maritime Organization (IMO) negotiations for another year. The agreement, which would have established binding targets for cleaner fuels and mandatory emissions reductions from 2028, was derailed following U.S. threats of tariffs and sanctions against supporters of the plan. The delay not only disrupts the timeline for a long-awaited global fuel standard but also undermines market confidence in zero-carbon shipping investments. Analysts warn that the one-year adjournment could stall financing for green hydrogen and ammonia projects, weaken incentives for early movers, and increase reliance on regional frameworks such as the EU ETS and FuelEU Maritime Regulation. While the latter imposes stricter carbon intensity limits, it also risks locking in LNG and first-generation biofuels, slowing the transition to true zero-emission fuels. The IMO setback has therefore widened the gap between global ambition and regional implementation, exposing the fragility of consensus in maritime climate governance.

Europe’s regional mechanisms are advancing but face growing challenges. The EU ETS’s first year of coverage for maritime operators revealed an 11% non-compliance rate, which is more than triple that of other regulated sectors, revealing both operational hurdles and enforcement gaps in integrating shipping into the bloc’s carbon market. At the same time, industry associations are urging Brussels to use the forthcoming Sustainable Transport Investment Plan to bridge policy voids and accelerate investment in zero-carbon ship technologies. Without stronger incentives, streamlined compliance, and consistent funding, stakeholders warn that Europe’s decarbonization leadership could falter amid global uncertainty and competitive pressure from regions with looser standards.

Voluntary Market & Emerging Compliance Markets

Indonesia allows resumption of international carbon trade after four years

Reuters

Carbon Pulse

COP30: Tinubu approves national carbon market framework

Vanguard News

EU makes fresh push for global carbon pricing ahead of 2026 levy

Alice Hancock and Simon Mudly, Financial Times

Ten years after it was signed, what has the Paris Agreement on climate change achieved?

Audrey Garric, Le Monde

Momentum in emerging carbon markets accelerated this month as several developing economies moved to formalize trading systems and reopen international participation. Indonesia has lifted its four-year moratorium on cross-border carbon trading through a presidential decree that reauthorizes international transactions under national or UN-certified standards, signaling a return to global markets for one of the world’s largest suppliers of REDD+ credits. The decree establishes a decentralized, real-time registry to prevent double counting and aligns with President Prabowo Subianto’s plan to attract foreign capital through verified rainforest and conservation projects. Indonesia’s exchange, launched in 2023, now offers carbon credits to overseas buyers, while new recognition agreements with certifiers such as Verra and Gold Standard aim to standardize quality. In parallel, South Africa’s National Treasury unveiled a reform blueprint to integrate its carbon tax with a domestic carbon market and align compliance and voluntary mechanisms under a single framework linked to Article 6 of the Paris Agreement.

Nigeria and the European Union are also scaling up efforts to consolidate climate finance and carbon pricing leadership. President Bola Tinubu approved Nigeria’s National Carbon Market Framework and the operationalization of a Climate Change Fund, targeting up to $3 billion annually in carbon finance over the next decade to fund adaptation and low-carbon investments. Meanwhile, the EU is intensifying diplomatic outreach through its international carbon pricing task force, now working with more than 40 countries to expand emissions trading coverage and harmonize carbon accounting standards ahead of the 2026 carbon border levy. Carbon pricing currently covers 28% of global emissions, with 80 national or regional systems in operation. As COP30 opens in Belém, global focus has returned to the broader climate architecture: ten years after the Paris Agreement’s adoption, the treaty has helped shift projected warming from 4°C to roughly 2.8°C by 2100 but remains far from its 1.5°C target, with emissions at record highs. Still, it continues to anchor climate governance and provides the foundation for the new generation of carbon markets taking shape across emerging economies.

Special CBAM Section – Egypt

Among MENA economies, Egypt stands out as the most exposed country to the EU’s CBAM. With the EU accounting for roughly 22% of Egypt’s total trade, equivalent to €12.6 billion in 2024, CBAM presents both a direct competitiveness challenge and an opportunity to modernize industrial and climate policy. Egypt ranks highest in the region on the World Bank’s CBAM Exposure Index, reflecting high carbon intensity combined with deep EU trade integration. While CBAM-covered products represent less than 5% of Egypt’s global exports, they dominate its trade with Europe: roughly 75% of iron and steel, 70% of aluminum, and 50% of fertilizer exports go to the EU. Without a national carbon pricing system or emissions trading scheme in place, Egyptian exporters face rising compliance costs and margin pressure as CBAM phases in by 2026. Some large firms have begun monitoring and verifying emissions, but MRV practices remain inconsistent across sectors. Strengthening these systems while preparing an Article 6-aligned national ETS would reduce exposure and enhance Egypt’s negotiating position under EU climate trade rules.

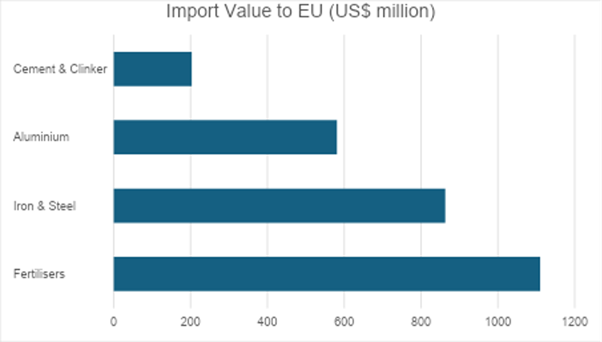

Sectoral data highlight the scale and concentration of Egypt’s exposure. The EU imported approximately US $863 million in iron and steel from Egypt in 2024, US $581 million in aluminum, US $1.11 billion in fertilizers, and US $203 million in cement and clinker which are equivalent to about 1 million tonnes and an 8.9% EU market share. Iron and steel remain the most vulnerable given their high emissions intensity and energy dependence, while fertilizer exports risk losing up to 18% of their EU market share. Aluminum faces electricity-related carbon costs that could erode profitability, whereas cement may retain some competitive advantage if Egyptian plants prove less carbon-intensive than European peers. In the near term, the CBAM transition poses clear macroeconomic risks potentially reducing GDP growth, employment, and export revenues in key industrial sectors.

Recommended Reads

JPMorgan Says US Risks Missing Energy Goals Without Wind, Solar

Alastair Marsh, Will Mathis and Gautam Naik ,Bloomberg

EU to bypass Washington and woo US states on green agenda

Alice Hancock and Henry Foy, Financial Times

LEAK: EU countries circulate draft letter urging Brussels to delay ETS2 until 2030

Carbon Pulse

West Balkan power producers should adopt carbon pricing as EU tax looms, campaigners say

Reuters

UN shipping agency delays decision on carbon price under US pressure

Enes Tunagur and Jonathan Saul, Reuters

To explore insights and tools driving carbon compliance and markets, visit the FACS website here!